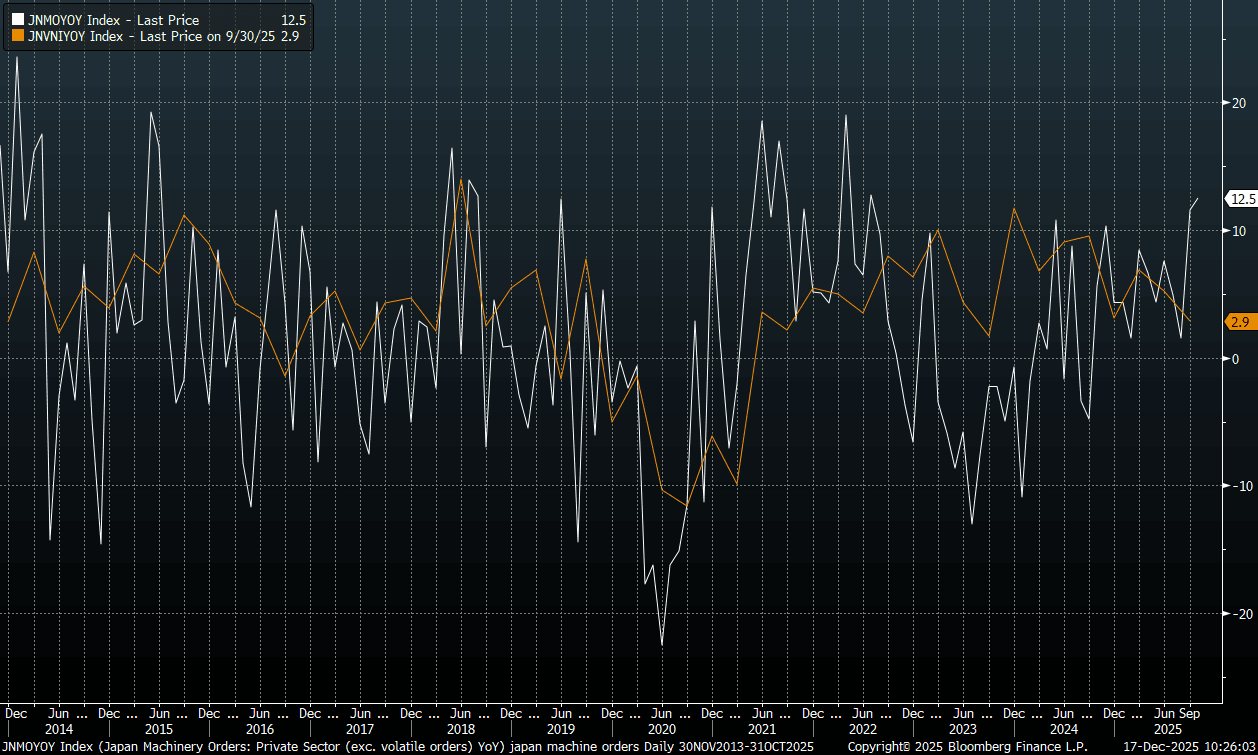

JAPAN DATA: Machine Orders Well Above Forecasts, Bodes Well For Capex Spend

Japan core machine orders for Oct were notably above forecasts. In m/m terms we rose 7.0%, against a -1.8% forecast, while y/y we rose 12.5%, versus a 3.6% forecast. This leaves the y/y pace at fresh highs back to 2022. The chart below plots the machine order print against capex y/y (ex software). The positive trend for machine orders bodes well for the capex outlook. Business/capex spending has been an important source of growth for Japan, although we saw a dip in Q3.

Fig 1: Japan Core Machine Orders & Capex Y/Y (Ex Software)

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

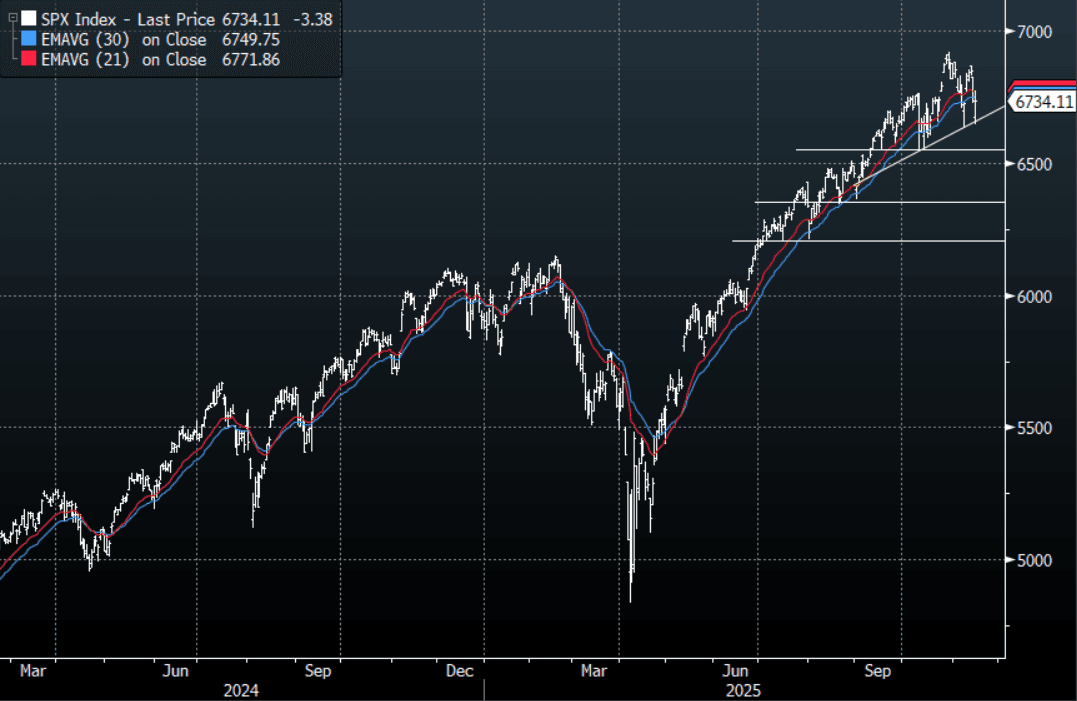

US STOCKS: S&P(ESZ5) - Bounces Off Support, Keeping Bullish Trend Intact

The S&P(ESZ5) overnight range was 6670.50 - 6795.50, SPX closed -0.05%, Asia is currently trading around 6760.00. The S&P looked to be rolling over again on Friday night down almost 1.5% before it found solid demand during the N/Y session and pared back all the day's losses. The market will be looking toward the release of some US data this week to get a gauge on things and also heavily focused on the upcoming Nvidia results which will heavily impact the direction of markets this week. The Crypto space which has been a leading indicator for risk has fallen to a low around $93 000 this morning and is technically starting to look vulnerable to a deeper correction. This morning stocks opened a little higher, E-minis(S&P) +0.05%, NQZ5 +0.10%. Technically the S&P has put in a lower high on the Daily chart and this could be signaling a deeper potential pullback, but a break below the support between 6550-6600 will be needed first to confirm a break of the bullish trend.

Fig 1: S&P 500 Index Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

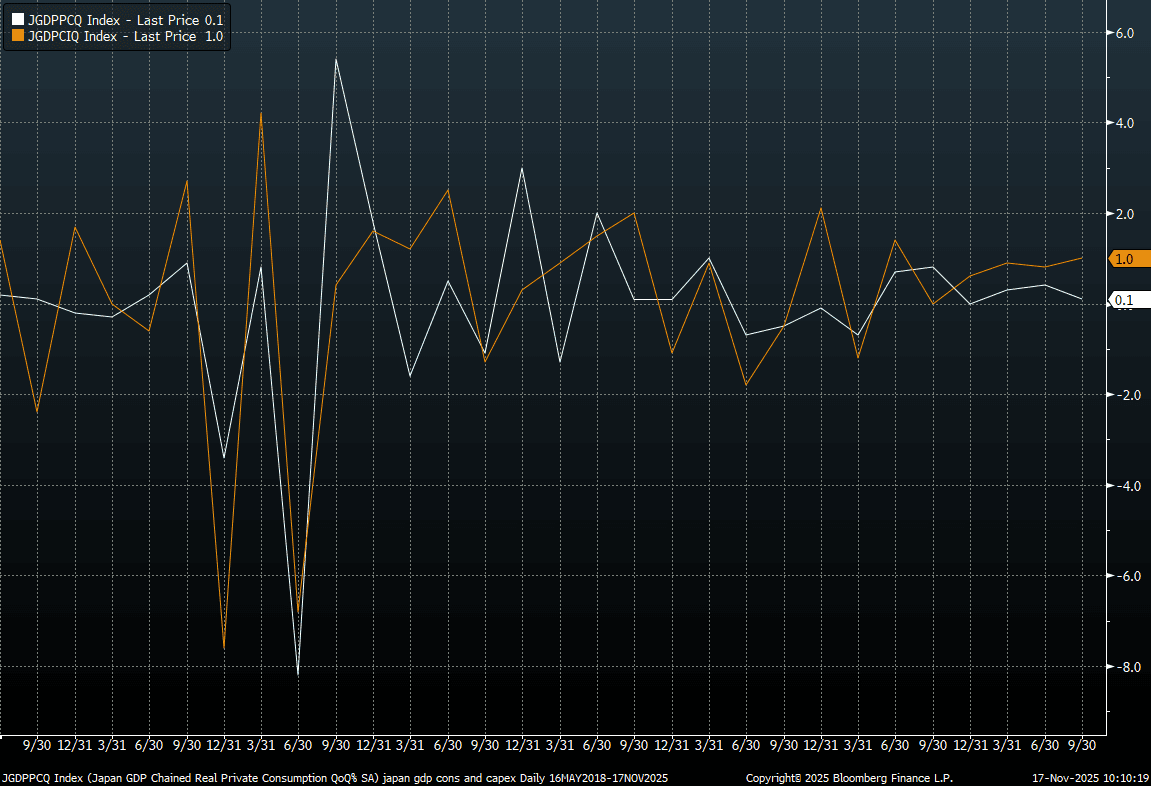

JAPAN DATA: Q3 GDP Contracts, But Resilient Detail, Particularly Business Spend

Q3 GDP (preliminary) in Japan was negative q/q, but not as much as the market forecast, thanks to upbeat business spending (+1.0%q/q versus -0.1% forecast). This was the first GDP decline since Q1 2024, but the detail paints a resilient underlying economic backdrop and comes ahead of fresh fiscal stimulus from the new Takaichi government. Today's GDP data should add some confidence, at the margins, the BOJ has in the GDP backdrop (particularly in terms of the drivers). We await Ueda's early Dec speech for details around hike timing.

- The q/q outcome for GDP was -0.4% against a -0.6% forecast. Note Q2 growth was revised to +0.6% from 0.5% originally reported. In annualized terms, growth -1.8%q/q, versus -2.4% forecast and a revised 2.3% gain in Q2. Note business s[ending was also revised up in Q2 to 0.8% from 0.6%q/q. Other components of GDP were close to forecasts, consumption up 0.1%q/q, while inventories were a -0.2ppt drag and net exports also trimmed -0.2ppt off growth.

- Whilst this is just a preliminary GDP print, the detail should be welcomed by the authorities. The q/q trends for private consumption (the white line) and business spending are plotted in the chart below.

- The resilience to strength in business spending, in particular, will be welcome. Via our Tokyo policy team: Private consumption and capital investment, the major components of the economy, are likely to firm in or after the fourth quarter, the official said. Private consumption, particularly non-durable goods, was hit by high prices and scorching weather in Q3, but is undergoing a moderate recovery supported by improving consumer sentiment, the official added.

- This also comes ahead of fresh fiscal stimulus, via BBG: "The Finance Ministry plans an economic package worth about ¥17 trillion ($110 billion), the Nikkei reported on Saturday, without identifying its sources. The supplementary budget to fund the spending is expected to reach about ¥14 trillion, exceeding last year’s ¥13.9 trillion compiled under former Prime Minister Shigeru Ishiba, the report said." - BBG

Fig 1: Japan GDP Components, Q/Q (Consumption (White Line) & Business Spending (Orange Line)

Source: Bloomberg Finance L.P./MNI

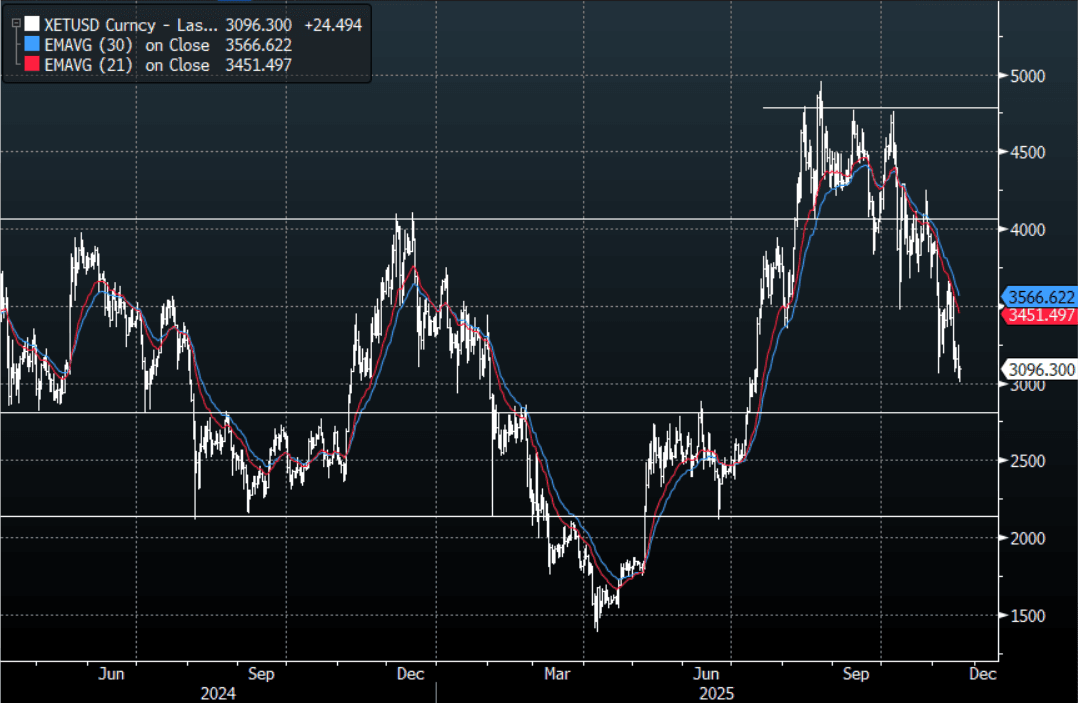

CRYPTO: Ethereum - Support Toward $2700 Approaches, Fade Bounces Toward $4000

Ethereum had a range over the weekend of $3025.15 - $3247.15, Asia is trading around $3100, +1.00%. Ethereum has traded under pressure over the weekend, it gapped lower on the Asian open testing the $3000 area before finding some demand. There are lots of commentators saying this will be the low, but in my experience when you have a leveraged asset class it tends to squeeze out weaker hands and inflict maximum pain before it finds a base again. Technically it now looks to be in a short-term bear market and I think rallies could potentially now be faded, the perfect sell-zone is toward the $3800-$4100 area, where I suspect sellers will return if given the chance. Ethereum has had a deep pullback almost 40% off its highs seen August, so at some point I think it should again offer value, technically the support comes in initially around $2600-$2800, then more big support toward the $2000-$2200 area.

Fig 1: Ethereum spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P