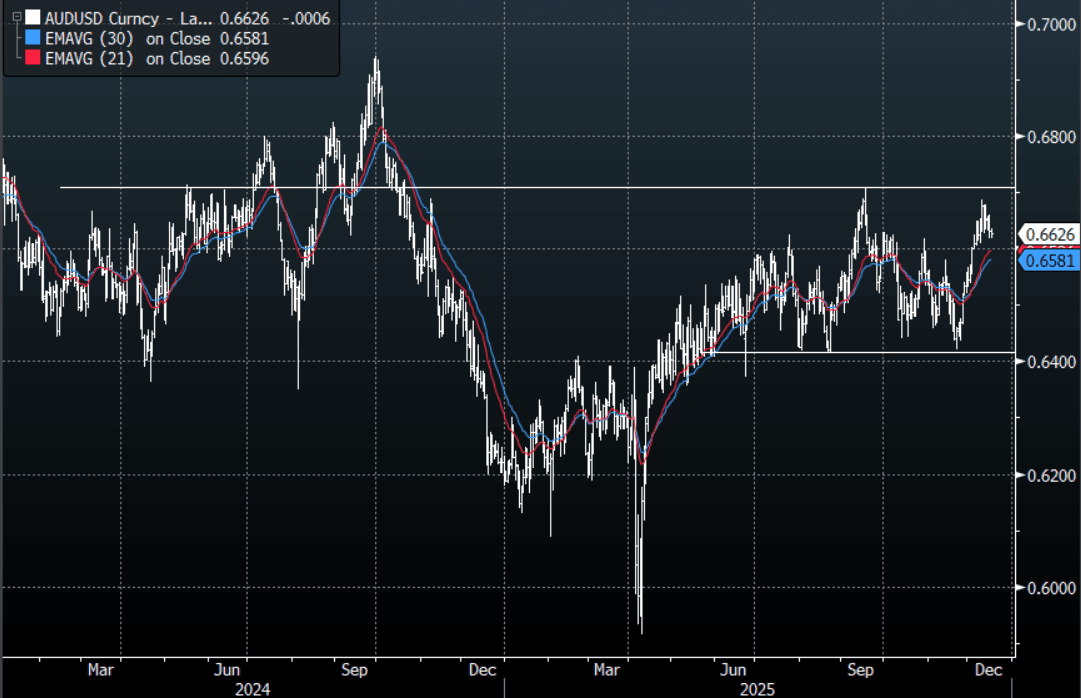

AUD: AUD/USD - Consolidating Above 0.6600-0.6630

The AUD/USD has had a range today of 0.6619 - 0.6635 in the Asia- Pac session, it is currently trading around {AUDUSD Curncy}. The AUD slipped lower as risk took a turn for the worst in Asia on the US blockade of Venezuela, risk has since pared back those losses but the USD has remained bid for now. The AUD price action remains constructive and while the AUD remains above 0.6500-0.6550 I suspect dips could continue to be supported. On the day, while the 0.6600-0.6630 area continues to provide support I would probably be skewed long looking for a move back toward the 0.6660-80 resistance. If this support area does not hold it could signal a deeper pullback toward the 0.6550 area.

- "AUSTRALIA NOV. WESTPAC LEADING INDEX FALLS 0.04% M/M" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6590(AUD680m), 0.6700(AUD655m). Upcoming Close Strikes : 0.6550(AUD1.07b Dec 18 ), 0.6675(AUD1.1b Dec 19), 0.6700(AUD1.57b Dec 19) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Modestly Cheaper Ahead Of Tomorrow's RBA Minutes & Wed's WPI

ACGBs (YM -2.5 & XM -4.0) are weaker on a data-light session.

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at +33bps.

- The bills strip is -2 to -3 across contracts.

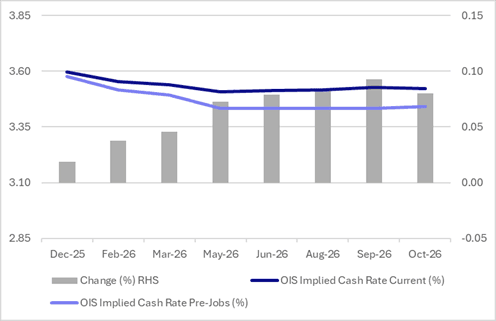

- Interest rate expectations in Australia out to mid-2026 have firmed just shy of 10bps over the past week. The key driver of this move was October’s employment data. The labour market normalised, with unemployment returning to 4.3% after September’s 4.5% spike. OIS pricing implies just a 1% probability of a 25bp December cut (9% pre-data), with cumulative easing of 9bps priced by mid-2026 (down from 17bps pre-data). (see chart)

- Even still, as previously noted, markets may still be overestimating the likelihood of further cuts, given that rising annual inflation has historically ended RBA easing cycles.

- Tomorrow, the local calendar will see RBA Minutes of the Nov. Policy Meeting ahead of the Wage Price Index on Wednesday.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$1000mn of the 2.75% 21 June 2035 bond on Wednesday and A$700mn of the 1.25% 21 May 2032 bond on Friday.

Figure 1: RBA-Dated OIS – Current Vs. Pre-Jobs

Source: Bloomberg Finance LP / MNI

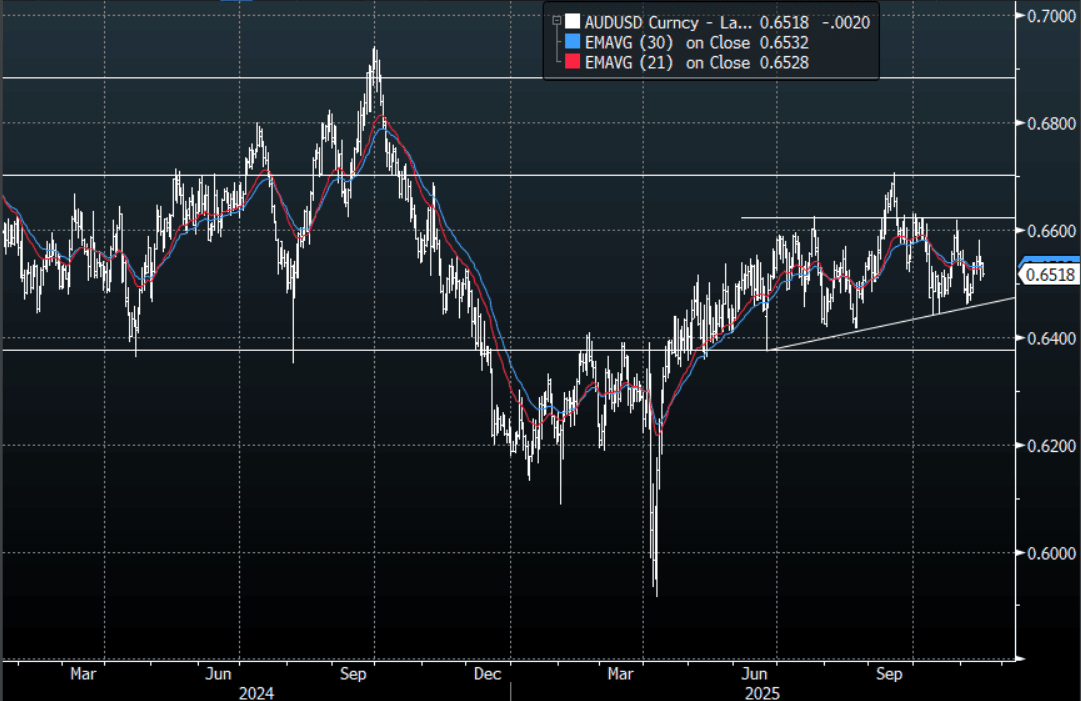

AUD: Asia-Pac: AUD/USD Drifts Lower As USD/ASIA Extends Higher

The AUD/USD has had a range today of 0.6512 - 0.6537 in the Asia- Pac session, it is currently trading around 0.6520, -0.30%. The AUD/USD has drifted lower in our session being led by the move higher in USD/Asia. The AUD/USD tested the 0.6500 area on Friday but bounced into the weekend with US stocks. The AUD/USD looks a little lost and is chopping around in a clearly defined range. Bitcoin gapped lower on the open but has since recouped all its losses moving back above $95k, the moves in crypto have recently been leading the market but for this to get legs it would need to break below the pivotal $90k area to add to the current market malaise. The AUD/USD has basically traded 0.6350-0.6650 since April this year and we will need a catalyst for this to break, otherwise it looks like more of the same unfortunately.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6525(AUD394m). Upcoming Close Strikes : 0.6400(AUD913m Nov 18), 0.6550(AUD674m Nov 20), 0.6600 (AUD679m Nov 18) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 39 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Cheaper But Best In $-Bloc, Nov Cut Hopes Stable

NZGBs closed showing a modest bear-steepener, with benchmark yields 1-2bps higher.

- Today’s move leaves the 2/10 yield curve around cycle highs, the highest since 2021.

- NZGBs outperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 1-2bps tighter.

- “On average, respondents believed there was a 38% chance of finding a new job, down from 41.2% in 3q and the lowest since the survey began in 1q 2022.” - RBNZ via BBG

- “October selected prices update presents no obstacles to another rate cut from the RBNZ at next week's policy meeting, said Westpac in a report on Monday. Westpac has revised its forecast for December quarter inflation to +0.3% and +2.8% for the year to December, both down 0.1 percentage points from the bank's earlier forecast.” - BBG

- Swap rates closed 2-3bps higher.

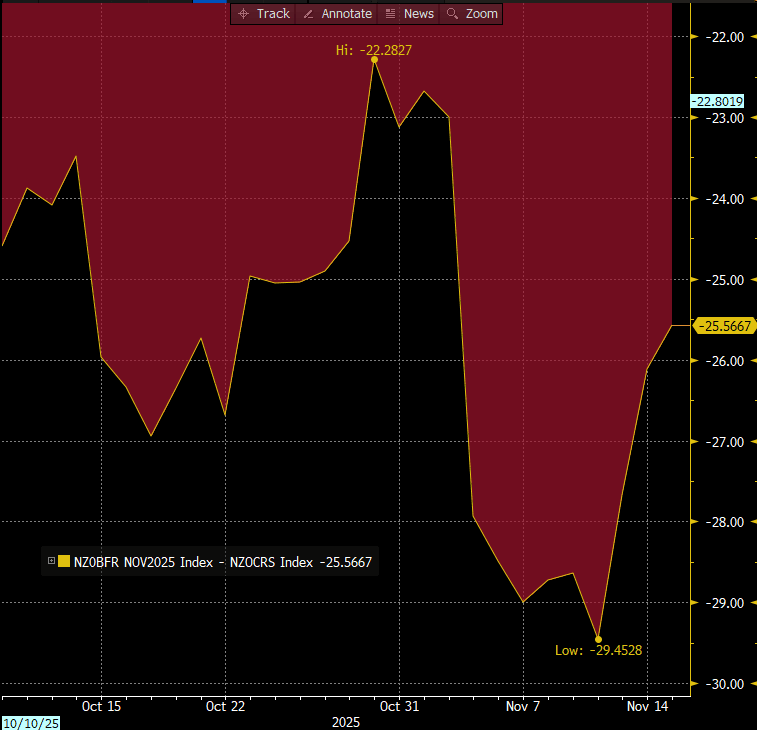

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for November, with a cumulative 34bps by February 2026. Pricing has been relatively stable over the past month. (see chart)

- Tomorrow, the local calendar will see Non-Resident Bond Holdings.

Bloomberg Finance LP