MNI EUROPEAN MARKETS ANALYSIS: Japan Exports Remain Weak

- The RBNZ cut rates 25bp to 3% bringing total easing to 250bp, as was widely expected. It revised down its OCR path with Q1 2026 now at 2.56% (May 2.85%). The prospect of more easing saw NZD drop over 1%, while RBNZ dated OIS pricing closed 14-23bps softer for meetings beyond August.

- In Japan, export growth remained negative, falling for the third straight month. Core machine orders were better than forecast though, suggesting a resilient capex outlook.

- Tech sensitive equity plays continue to lose ground. This has weighed on KRW & TWD, but JPY has outperformed in a more risk-off environment.

- Later the Fed’s Waller and Bostic appear and the July FOMC meeting minutes are published. Friday’s Chair Powell speech is likely the key event remaining this week. UK July CPI & PPI, euro area July CPI and German July PPI print. ECB President Lagarde appears on a panel.

MARKETS

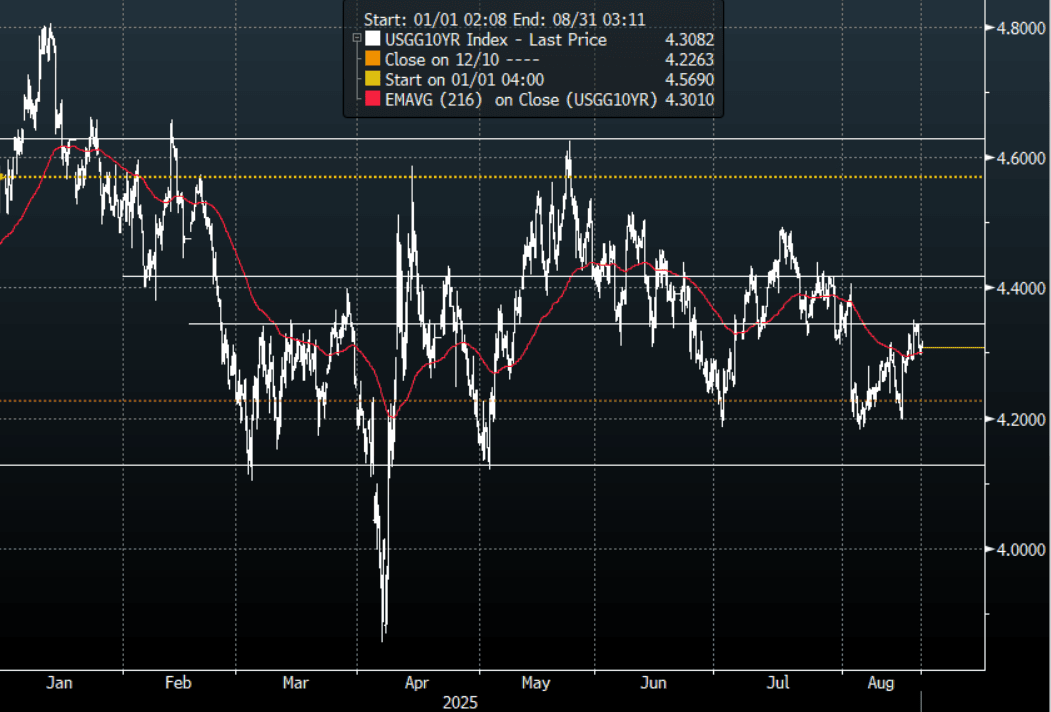

US TSYS: Asia Wrap - Yields Edge A Little Higher In The Front-End

The TYU5 range has been 111-21 to 111-26 during the Asia-Pacific session. It last changed hands at 111-23+, down 0-01 from the previous close.

- The US 2-year yield has edged higher trading around 3.752%, up 0.01 from its close.

- The US 10-year yield has edged higher trading around 4.308%.

- Yields are still firmly within its wider 4.10%-4.65% range. The 4.35% pivot area in 10-Year yields found solid demand overnight helped by the S&P rating, the market will now be waiting for any clues from Powell's upcoming Jackson Hole speech.

- “TRUMP: EVERY SIGN IS POINTING TO A MAJOR RATE CUT" - BBG

- "Could somebody please inform Jerome “Too Late” Powell that he is hurting the Housing Industry, very badly? People can’t get a mortgage because of him. There is no Inflation, and every sign is pointing to a major Rate Cut. “Too Late” is a disaster!" - (Trump Truth Social Post)

- (Bloomberg) - It’s not the first time that when monetary policy is tweaked in New Zealand, there’s a read across for G-10 peers, especially Treasuries. The RBNZ lowered interest rates as expected, but surprised traders by implying deeper cuts into next year. The resulting yield curve steepening is likely to be replicated by fixed income peers where central banks have an easing bias.

- Data/Events: MBA Mortgage Applications, FOMC Meeting Minutes

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Mostly Cheaper With A Steeper Curve

JGB futures are little changed, -3 compared to settlement levels.

- Japan Export Growth Negative, Lagging Other Parts Of Asia : Japan July export and import outcomes were fairly close to market expectations, but the trade balances were slightly weaker. Exports fell -2.6%y/y (-2.1% forecast and -0.5% prior), while imports were -7.5%y/y, (-10.0% forecast and 0.3% prior). The trade deficit was -117.5bn, against a 198.5bn forecast.

- Japan Core Machine Orders Above Forecasts, Suggesting Resilient Capex : Japan June core machine orders were better than forecast. We rose 3.0%m/m, versus -0.5% forecast and -0.6% prior. The y/y print was 7.6%, against a 4.7% forecast and 4.4% prior. Today's machine orders print continues to paint a resilient capex picture for Japan's economy.

- US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are slightly mixed across benchmarks, with yields 0.5bp lower (7-year) to 3bps higher (40-year). The benchmark 10-year yield is 0.4bp higher at 1.606% versus the cycle high of 1.616%.

- Swap rates are flat to 1-2bps higher, with a steepening bias.

- Tomorrow, the local calendar will see Weekly International Investment Flows, S&P Global PMIs (P) and Machine Tool Orders alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

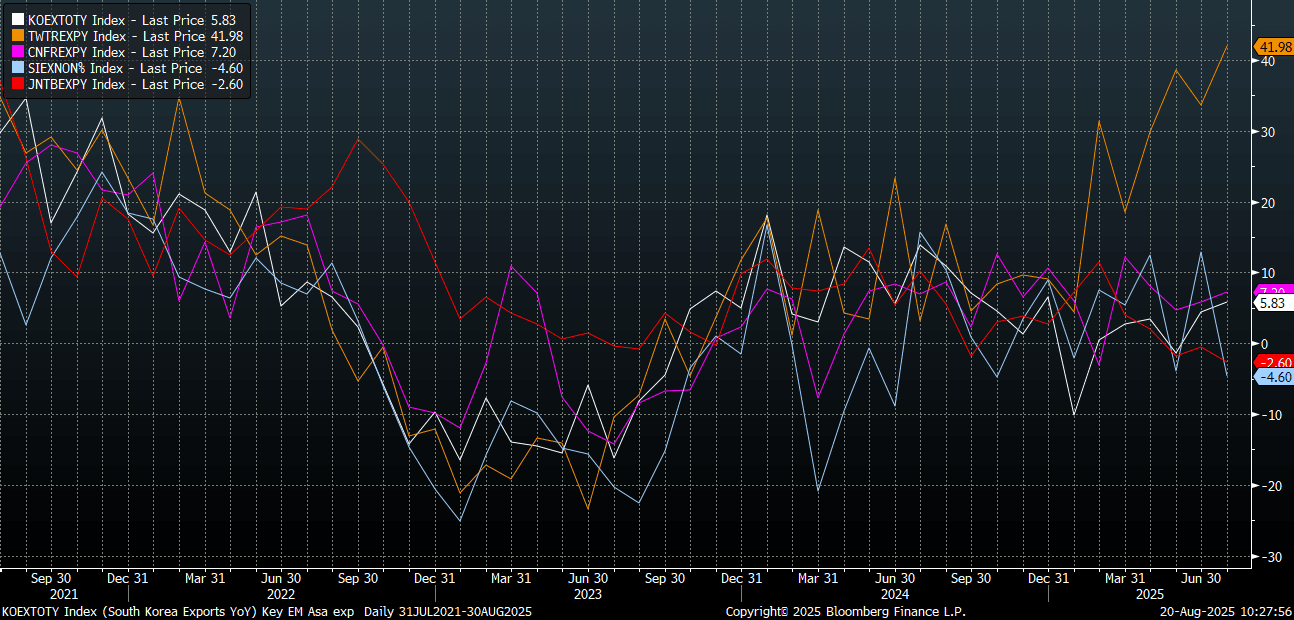

JAPAN DATA: Export Growth Negative, Lagging Other Parts Of Asia

Japan July export and import outcomes were fairly close to market expectations, but the trade balances were slightly weaker. Exports fell -2.6%y/y (-2.1% forecast and -0.5% prior), while imports were -7.5%y/y, (-10.0% forecast and 0.3% prior). The trade deficit was -¥117.5bn, against a ¥198.5bn forecast. In seasonally adjusted terms we printed at -¥303bn, against a -¥67.2bn forecast (June's outcome was -¥247.6bn).

- Exports to the US were down -10.1%y/y, to China -3.5%y/y, while to the EU -3.4%y/y. In volume terms the falls weren't as large, -2.3%y/y for the US. For aggregate exports we actually rose 1.2%y/y. Import volumes were up 4.0%y/y.

- Broader export trends are lagging nominal growth seen in the likes of Taiwan and South Korea, along with China (all of which remained in positive territory for July in y/y terms. See the chart below, where Japan is the red line. Taiwan, the orange line, remains the standout.

- Via BBG: "The downturn, led by cars, auto parts and steel, was the biggest since February 2021. Export volumes rose by 1.2%, suggesting exporters are continuing to absorb US tariff costs by cutting selling prices to preserve market share."

- Japan's trade surplus with the US was ¥585.1bn, down from recent highs (¥918.48bn recorded in Feb). The trade deficit recorded as a whole for Japan was within recent ranges for 2025.

- Whilst there is some relief around the trade deal struck with the US, it is yet to be fully implemented (as Japan awaits written documentation from the US).

Fig 1: Key Asia Economy Exports - Y/Y, Japan Lagging Some Other Parts Of Asia

Source: Bloomberg Finance L.P./MNI

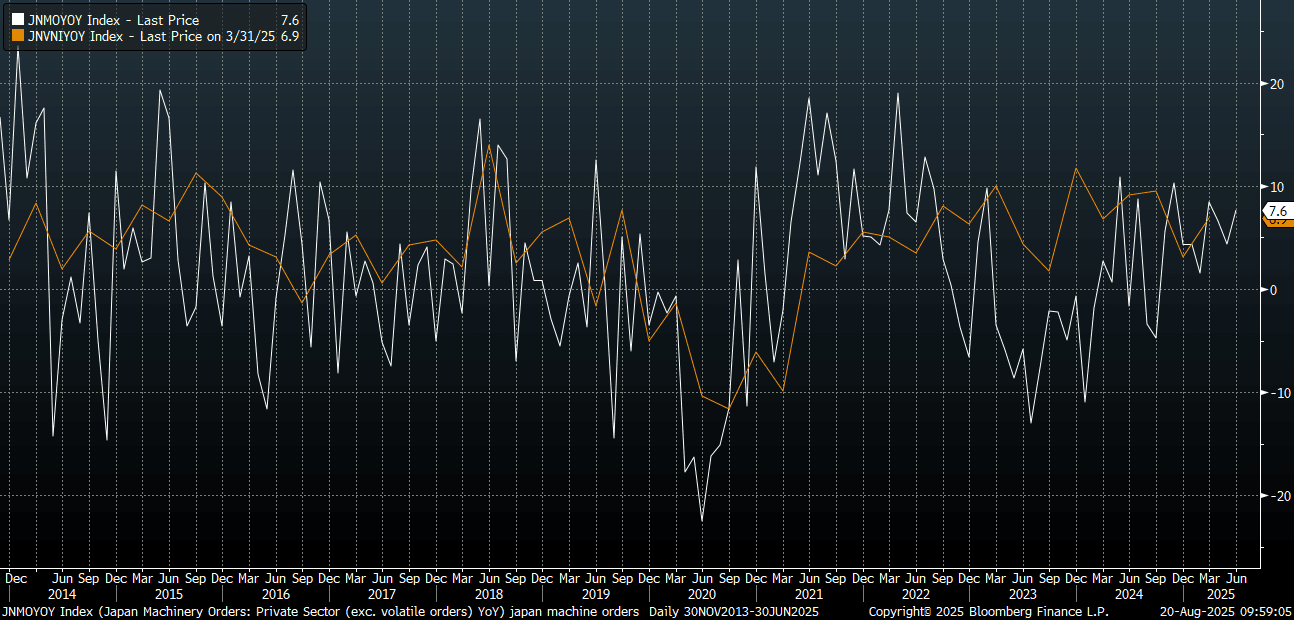

JAPAN DATA: Core Machine Orders Above Forecasts, Suggesting Resilient Capex

Japan June core machine orders were better than forecast. We rose 3.0%m/m, versus -0.5% forecast and -0.6% prior. The y/y print was 7.6%, against a 4.7% forecast and 4.4% prior. The chart below overlays y/y core machine orders (the white line on the chart) against capex for Japan in y/y terms (ex Software). Today's machine orders print continues to paint a resilient capex picture for Japan's economy.

- We don't get the full capex read for Q2 until the start of Sep. Still, the recent Q2 GDP print (preliminary) showed business up 1.3% in Q2, which was above forecasts (+0.7%). So today's core machine orders result is consistent with that backdrop.

Fig 1: Japan Core Machine Orders & Capex Y/Y (Ex Software)

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Holding Richer After RBNZ's Forward Guidance

ACGBs (YM +4.5 & XM +3.5) are richer but off session bests.

- The local market has benefited from positive spillover from a strong post-RBNZ rally in NZGBs.

- The RBNZ cut the OCR by 25bps to 3.0%, as expected (4-2 vote; some favoured a 50bp cut), with forward guidance that saw the OCR averaging 2.71% in 4Q 2025, 2.56% in 2Q 2026, and 2.59% in 3Q 2026 (down from May's trough forecast of 2.9%). It indicated scope for further rate cuts if inflation pressures ease; forecasts imply a good chance of two more 25bp cuts.

- Cash US tsys are little changed in today's Asia-Pac session after modest gains.

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at -2bps.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in September is given a 30probability, with a cumulative 37bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will see S&P Global PMIs (P) and Consumer Inflation Expectation data.

- The AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Friday.

BONDS: NZGBS: RBNZ Forward Guidance Sparks Massive Rally

NZGBs closed 10-16bps richer, with a steeper 2/10 curve, after today’s RBNZ policy decision.

- The pace of NZ’s economic recovery appears to have disappointed the MPC, with Q2 GDP expected to contract again. The MPC decided to cut rates 25bp to 3% by a vote of 4-2, with two members voting for a 50bp reduction.

- The MPC said that the OCR path was a “central expectation” “needed to ensure inflation” is sustainably at the band mid-point and it was revised lower which was said to likely provide “sufficient signalling effects”. The revised OCR path now troughs 30bp below the May assumption at 2.55% - the bottom of the RBNZ’s estimated neutral range.

- The revised OCR path implies another 43bp of easing by year end with 16bp in Q1 2026.

- Swap rates closed 11-18bps lower, with a steeper 2s10s curve.

- RBNZ dated OIS pricing closed 14-23bps softer for meetings beyond August. 35bps of cumulative easing is priced by November 2025.

- Tomorrow, Governor Hawkesby will appear before a parliamentary committee to talk about the latest Monetary Policy Statement.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

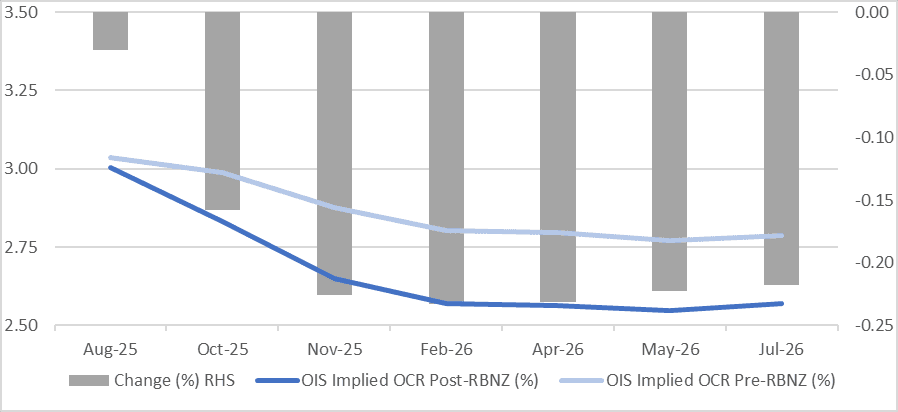

STIR: RBNZ-Dated OIS Shunt Softer After RBNZ Decision

RBNZ dated OIS pricing closed 14-23bps softer for meetings beyond August following today’s RBNZ Policy Decision.

- The market had priced 22bps of today’s 25bp cut going into the decision.

- 35bps of cumulative easing is now priced by November 2025 versus 12bps before the decision.

Figure 1: RBNZ Dated OIS Post-RBNZ vs. Pre-RBNZ (%)

Source: Bloomberg Finance LP / MNI

RBNZ: Rates Cut As Expected, OCR Path Revised Lower

The RBNZ cut rates 25bp to 3% bringing total easing to 250bp, as was widely expected. It revised down its OCR path with Q1 2026 now at 2.56% (May 2.85%). See press release here. More details to follow.

RBNZ: OCR Path “Signals” Further Easing

The pace of NZ’s economic recovery appears to have disappointed the MPC with Q2 GDP expected to contract again. The MPC decided to cut rates 25bp to 3% by a vote of 4-2 with two members voting for a 50bp reduction. The MPC said that the OCR path was a “central expectation” “needed to ensure inflation” is sustainably at the band mid-point and it was revised lower which was said to likely provide “sufficient signalling effects”. The revised OCR path now troughs 30bp below the May assumption at 2.55% - the bottom of the RBNZ’s estimated neutral range.

- The revised OCR path implies another 43bp of easing by year end with 16bp in Q1 2026. This suggests that the last two meetings of 2025 on October 8 and November 26 are both “live” with around an even possibility of another one in February 2026. However, the MPC was clear that it remains highly data dependent.

- Headline inflation was revised higher over H2 2025 and H1 2026 and is forecast at 2.2% in Q4 2026 with it not returning to the 2% mid-point of the target band until H1 2027. It is now expected to be at the top of the band in Q3 2025.

- Rates were cut by 25bp as upside and downside risks were seen as “broadly balanced”, financial conditions continue to ease due to previous cuts and the OCR would signal the MPC’s easing bias.

- The case for a 50bp cut included “declining inflationary pressure and significant spare capacity”, global uncertainty could have “self-reinforcing” effects on domestic demand, a larger cut would send a clearer signal and excess capacity would put downward pressure on inflation.

- Arguments to hold rates were discussed which included global uncertainty had eased since May, the full effect of previous easing was yet to be felt, July data “suggest some improvements” and inflation is close to the top of the band and near-term expectations are rising. One member supported this view.

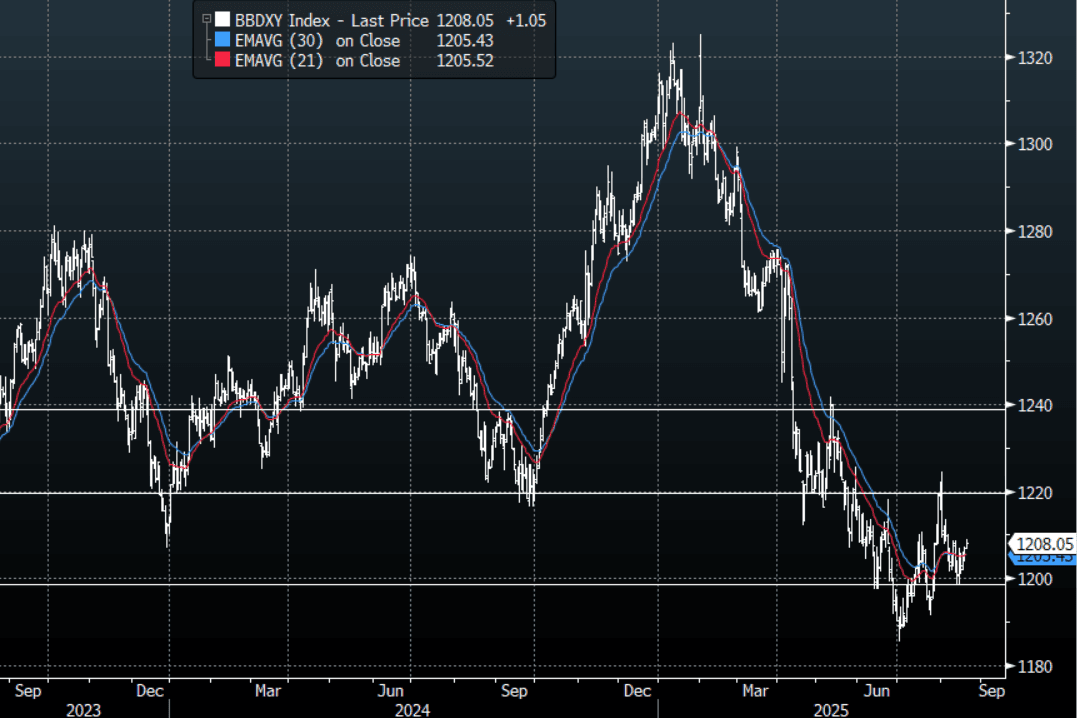

FOREX: Asia FX Wrap - The USD Bid Remains Steady Heading Into Jackson Hole

The BBDXY has had a range of 1206.79 - 1208.95 in the Asia-Pac session, it is currently trading around 1208, +0.10%. The USD continues to see profit-taking as the market pares back some risk as we head into Jackson Hole at the end of the week. Depending on the contents of Powell's speech this could change very quickly but the BBDXY looks to be putting in a third higher low which would be a worrying sign to the bears that we could be putting in a short-term base. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows, but risk is more likely skewed to the USD shorts continuing to be reduced into Powell's speech.

- EUR/USD - Asian range 1.1622 - 1.1651, Asia is currently trading 1.1635. The market is trading sideways in a 1.1600-1.1750 range heading into Jackson Hole. The pair is unlikely to extend too far as the market awaits Powell's speech.

- GBP/USD - Asian range 1.3462 - 1.3493, Asia is currently dealing around 1.3475. Having broken back above its pivot look for dips to again be supported, with risk retracing the pair is probing its first support seen towards 1.3400.

- USD/CNH - Asian range 7.1868-7.1931, the USD/CNY fix printed 7.1384, Asia is currently dealing around 7.1890. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.30%, Gold $3320, US 10-Year 4.31%, BBDXY 1208, Crude Oil $62.41

- Data/Events : EZ CPI, Germany PPI

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

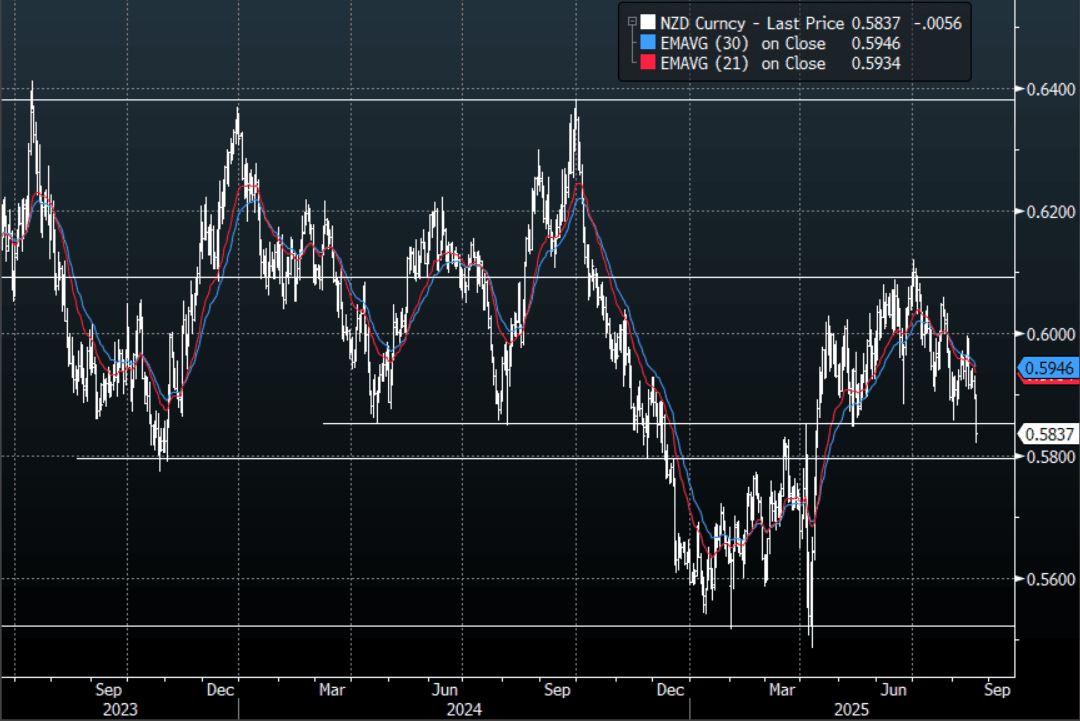

NZD: Asia Wrap - NZD/USD Probing Pivotal Support On A Dovish RBNZ Cut

The NZD/USD had a range of 0.5821-0.5900 in the Asia-Pac session, going into the London open trading around 0.5935, -0.95%. A dovish RBNZ that contemplated a cut of 50bps saw NZD/USD break lower and is now probing some pivotal support around the 0.5800/0.5850 area. Some of the crosses have broken some key levels AUD/NZD above 1.1000 & NZD/JPY below 86.50. Risk has extended its move lower this morning, E-minis -0.30%, NQU5 -0.45% adding to the weight in the NZD.

- RBNZ: OCR Path “Signals” Further Easing. The pace of NZ’s economic recovery appears to have disappointed the MPC with Q2 GDP expected to contract again. The MPC decided to cut rates 25bp to 3% by a vote of 4-2 with two members voting for a 50bp reduction. The MPC said that the OCR path was a “central expectation” “needed to ensure inflation” is sustainably at the band mid-point and it was revised lower which was said to likely provide “sufficient signaling effects”. The revised OCR path now troughs 30bp below the May assumption at 2.55% - the bottom of the RBNZ’s estimated neutral range.

- "RBNZ GOV HAWKESBY: NEXT TWO MEETINGS ARE LIVE, NO DECISIONS HAVE BEEN MADE, OCR PROJECTION TROUGHS AROUND 2.5%, CONSISTENT WITH FURTHER CUTS” - [RTRS]

- "RBNZ GOV HAWKESBY: NEVER HAD A 4 TO 2 VOTE BEFORE, RANGE OF VIEWS AROUND THE RISKS TO OUTLOOK, MPC DEBATED RISKS AROUND MORE AGGRESSIVE CUT - [RTRS]"

- Whole Milk Prices Edge Higher At Latest Auction : Overnight the whole milk powder auction (held around 2 times per month) saw average prices rise 0.3% to $4036. Whole milk powder prices are up from recent lows but still around 7.7% off 2025 highs (albeit presenting a supportive backdrop for NZ's terms of trade).

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5925(NZD400m), 0.5950(NZD320m). Upcoming Close Strikes : 0.5980(NZD660m Aug 21). - BBG

- AUD/NZD range for the session has been 1.0939 - 1.1064, currently trading 1.1035. The dovish RBNZ has seen the Cross surge higher breaking back above 1.100 convincingly. This move should now see dips supported as it looks to build momentum to push higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

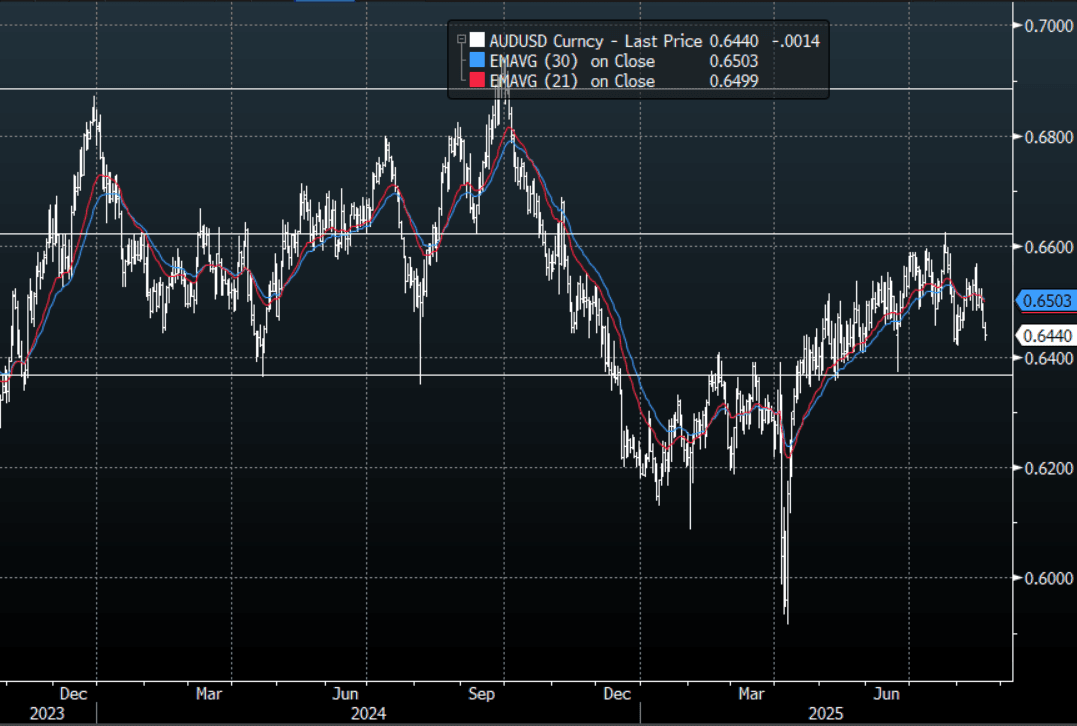

AUD: Asia Wrap - The NZD And Risk Drag AUD/USD Lower

The AUD/USD has had a range of 0.6429 - 0.6462 in the Asia- Pac session, it is currently trading around 0.6440, -0.25%. The AUD has been dragged lower by the move in the NZD and risk extending its correction lower in Asia. The AUD broke below its support just below 0.6500 overnight and looks likely to continue to trade heavy into the Jackson Hole meeting. Pivotal support is back towards 0.6300/50 which has been the bottom in its recent multi-month range of 0.6350-0.6650.

- Bloomberg - “Asian stocks fell after a selloff in big tech dragged Wall Street lower. US futures slid. Citadel Securities’ Scott Rubner said retail investors may slow their stock buying in September before resuming later this year.”

- "China Plans Broader Measures to Boost Housing Market: Paper. China is expected to roll out a fresh batch of measures to stabilize the housing market, Securities Daily reports, citing industry analysts it interviewed." - BBG

- Bloomberg - “China’s commercial banks kept loan prime rates steady for a third month, as expected.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD410m). Upcoming Close Strikes : 0.6510(AUD520m Aug 25), 0.6600(AUD1.34b Aug 21) - BBG

- CFTC Data shows Asset managers added to their shorts -67449(Last -60729), the Leveraged community though reduced their own shorts -10121(Last -13997).

- AUD/JPY - Asia-Pac range 94.87 - 95.37, Asia is trading around 94.95. The pair broke through 95.50 overnight and has put in another lower high. Although the price is still in the 94.00-97.50 range the multiple failures towards 97.00 looks like a rounded top and with risk looking vulnerable a test of the lower end of the range looks possible. A sustained break below the 94.00/94.50 area could potentially see momentum lower pick up. Not sure we see this until Jackson Hole event risk is out the way.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - Crosses Weigh On USD/JPY With Risk Extending Lower

The Asia-Pac USD/JPY range has been 147.42-147.82, Asia is currently trading around 147.50, -0.10%. USD/JPY is being weighed down by selling in the crosses as risk points to a potential retracement. Price continues to hold above the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again. While this plays out it looks to be more range trading within the wider 146.00-151.00 range. CFTC Data shows leveraged funds have bought this dip in USD/JPY betting the support remains intact. A dovish RBNZ has given NZD/JPY the nudge it needed to break below 86.50.

- Japan Export Growth Negative, Lagging Other Parts Of Asia : Japan July export and import outcomes were fairly close to market expectations, but the trade balances were slightly weaker. Exports fell -2.6%y/y (-2.1% forecast and -0.5% prior), while imports were -7.5%y/y, (-10.0% forecast and 0.3% prior). The trade deficit was -117.5bn, against a 198.5bn forecast.

- Japan Core Machine Orders Above Forecasts, Suggesting Resilient Capex : Japan June core machine orders were better than forecast. We rose 3.0%m/m, versus -0.5% forecast and -0.6% prior. The y/y print was 7.6%, against a 4.7% forecast and 4.4% prior. Today's machine orders print continues to paint a resilient capex picture for Japan's economy.

- Options : Close significant option expiries for NY cut, based on DTCC data: 148.00($999m), 149.00($733m).Upcoming Close Strikes : 146.80($1.24b Aug 21), 147.90($1.42b Aug 22) - BBG

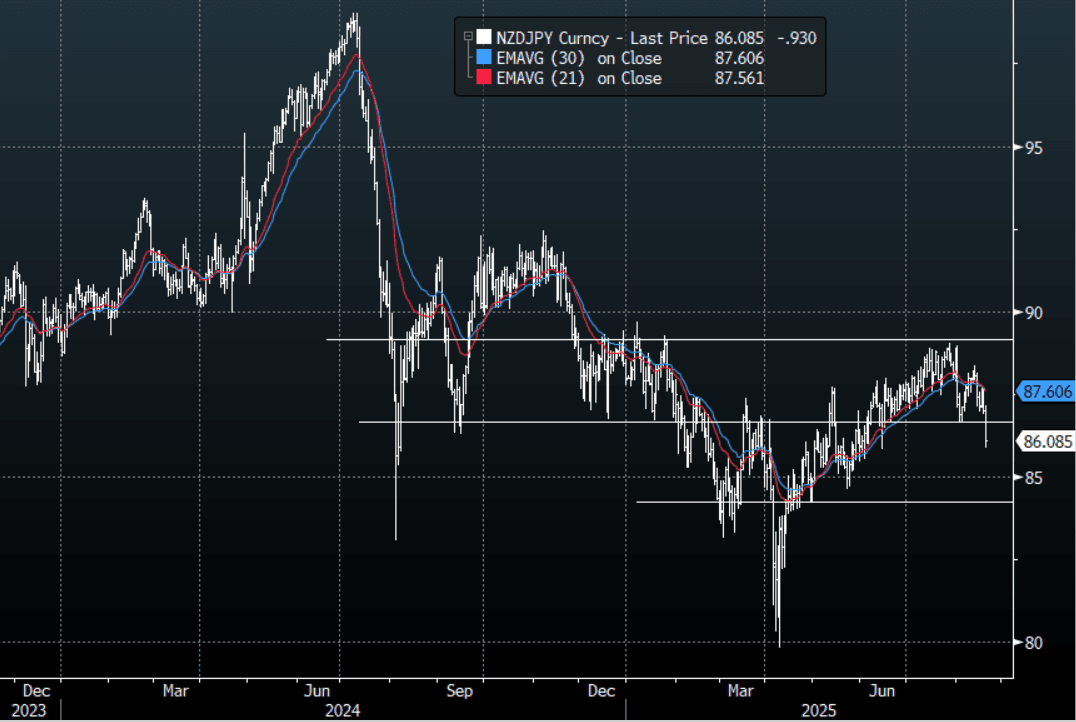

- NZD/JPY - Asia-Pac range 85.87 - 87.14, Asia is currently dealing 85.90. The pair has broken through its support around 86.50 on the back of a dovish RBNZ. This a powerful move lower and if sustained should now see bounces met with supply, especially if risk continues to retrace.

Fig 1 : NZD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Most Major Markets Weaker, Led By Tech Exposure

Some of the key Asian equity benchmarks are down sharply today, particularly those with a tech focus. This follows sharp US losses in this space during cash Tuesday trade. Tuesday saw some profit-taking after stalling around 6500 for the main US benchmark, as the market awaits Powell's Jackson Hole speech. Big Tech was hardest hit, having the largest concentration of positioning. We have also seen follow on US equity futures weakness, led by the tech side so far today. Nasdaq futures were last down a little over 0.50%, while Eminis were off close to 0.30%.

- There are some outperformers within Asia Pac so far today, with New Zealand up over 1.6% after the dovish RBNZ 25bps rate cut. The NZX 50 was last around Jan highs.

- Conversely, Taiwan's Taiex is down around 2.5%, while the Kospi is off close to 2%, as these markets feel the brunt of tech related sell-off. Offshore investors have turned net sellers of these markets in recent sessions as well.

- The NKY225 is down by around 1.8% in Japan, while the Topix is down by 0.75%.

- China's CSI 300 is down a modest 0.1%, while the HSI is down by nearly 0.6% at the lunch time break. The HSI tech sub index is off by 1.26% though.

- In South East Asia, Indonesia is outperforming modestly, up +0.55%, while most other markets are down a touch.

ASIA STOCKS: South Korea, Taiwan See Outflows, Indonesia & India See Inflows

South Korea and Taiwan markets saw outflows from offshore investors yesterday. For Taiwan the nearly $500mn in outflows was the largest since July 29. For both markets, the 5 day sum is negative. Broader tech equity weakness continued in Tuesday trade. There has been some concerns voiced around the AI outlook recently, while proximity to Fed Chair Powell's speech this Friday may also be driving some nervousness in terms of broader market trends.

- Elsewhere we saw offshore investors return to India at the start of the week, with the recent equity bounce (aided by potential GST changes) drawing in some inflows. Still, cumulative outflows since the start of July were close to $4.7bn, so momentum needs to meaningful shift in order to bring us closer to neutral from a Q3 standpoint.

- Indonesian flows remained positive, while weaker trends were evident elsewhere in South East Asia. Malaysia continued its outflow streak.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -298 | -238 | -5146 |

| Taiwan (USDmn) | -491 | -240 | 4046 |

| India (USDmn)* | 116 | -582 | -12721 |

| Indonesia (USDmn) | 53 | 277 | -3280 |

| Thailand (USDmn) | -13 | -273 | -1969 |

| Malaysia (USDmn) | -18 | -141 | -3408 |

| Philippines (USDmn) | -21 | -7 | -620 |

| Total (USDmn) | -671 | -1203 | -23098 |

| * Data Up To Aug 18 |

Source: Bloomberg Finance L.P./MNI

OIL: US Inventory Data Help To Stabilise Crude

Crude has stabilised during today’s APAC session after falling over a percent on Tuesday. US industry data showing a crude inventory build has provided some support with WTI up 0.4% to $62.04/bbl (Oct contract) off its intraday low of $61.83. Brent is 0.3% higher at $66.00 after falling to $65.81. The USD index is up 0.1%.

- With OPEC steadily increasing its production targets and forecasts for a growing market surplus, supply trends are being monitored closely. CBA is forecasting Brent to fall to $63/bbl in Q4 2025 due to rising global inventories, according to Bloomberg.

- While a Ukraine deal is a long way off, progress increases expectations that eventually sanctions on Russia will be eased. A setback could see the recent sell off reverse.

- Bloomberg reported that there was a US crude inventory draw of 2.4mn barrels last week, more than offsetting last week’s 1.5mn build. Gasoline stocks fell 1mn barrels but distillate rose 500k, according to people familiar with the API data. The official EIA data is out today.

- Later the Fed’s Waller and Bostic appear and the July FOMC meeting minutes are published. Friday’s Chair Powell speech is likely the key event remaining this week.

- UK July CPI & PPI, euro area July CPI and German July PPI print. ECB President Lagarde appears on a panel.

Gold Holds Losses, Fed Speakers & Minutes Later

Gold has been range trading today falling to $3311.6/oz before rising to $3319.59. It is currently 0.1% higher around $3318.8 holding onto Tuesday’s losses driven by steps taken towards a Ukraine truce. With markets hoping Fed Chair Powell will reveal his thinking for the September 17 decision on Friday, they are moving in narrow ranges. US yields are little changed and the USD index is 0.1% higher.

- Silver is down 0.5% to $37.212 off the intraday low of $37.170. A clear break of the 50-day EMA at $37.077 is needed to strengthen the short-term bearish threat. Initial resistance is at $39.655.

- Equities are also generally weaker with the Nikkei down 1.7%, Hang Seng -0.6% and S&P e-mini -0.3%. Oil prices are moderately higher with WTI +0.4% to $61.99/bbl. Copper is up slightly.

- Later the Fed’s Waller and Bostic appear and the July FOMC meeting minutes are published. UK July CPI & PPI, euro area July CPI and German July PPI print. ECB President Lagarde appears on a panel.

CHINA: Country Wrap: Fiscal Spend Ramping Up

- Nvidia is developing a new artificial intelligence chip for China based on its latest Blackwell architecture that will be more powerful than the H20 model it is currently allowed to sell there, two people briefed on the matter said. U.S. President Donald Trump last week opened the door to the possibility of more advanced Nvidia chips being sold in China. But the sources noted U.S. regulatory approval is far from guaranteed amid deep-seated fears in Washington about giving China too much access to U.S. AI technology. (source Reuters)

- The Trump administration said it will step up scrutiny of imports of steel, copper, lithium and other materials from China to enforce a US ban on goods allegedly made with forced labor in the country’s Xinjiang region. The announcement of new “high-priority sectors” targeted under the four-year-old Uyghur Forced Labor Prevention Act was included Tuesday in an annual update to the US government’s enforcement efforts. It also dovetails with President Donald Trump’s broader trade goals, as he seeks to lower the US trade deficit with China and pressures Beijing to curb shipments of fentanyl and precursor chemicals. “America has a moral, economic, and national security duty to eradicate threats that endanger our nation’s prosperity, including unfair trade practices that disadvantage the American people and stifle our economic growth,” US Homeland Security Secretary said in a statement. (source BBG)

- China’s broad fiscal spending expanded at the fastest pace in almost three years, pushing the deficit to another record as the government steers an economy grappling with weakening demand and higher tariffs. Total expenditure rose over 9% to 21.5 trillion yuan ($3 trillion) in the first seven months of 2025 from a year ago, according to data released by the Finance Ministry. That’s the fastest increase since August 2022. As a result, the broad fiscal gap reached 5.6 trillion yuan in the January-July period, with the shortfall widening 49% from a year ago. (source BBG)

- A weak day across the major bourses today with the Hang Seng down -0.57%, CSI 300 -0.12%, Shanghai -0.06% and Shenzhen -0.54%

- Yuan Reference Rate at 7.1384 Per USD; Estimate 7.1905

- Bonds yields are edging lower with the CGB10yr at 1.76% (from yesterday's close of 1.77%)

SOUTH KOREA: Country Wrap: Mid Size Firms Profits Decline

- Hana Securities has introduced an “omnibus account” for foreign investors, a first among Korean financial service providers, market watchers said Tuesday. The measure will grant easier access to global investors, translating into healthier growth momentum for the local equity market. According to the financial industry, the brokerage affiliate of Hana Financial Group recently inked an omnibus account partnership with Emperor Securities, a Hong Kong-based global brokerage. (source Korea Times)

- A majority of midsized firms reported declines in operating profit in the first half of the year amid economic uncertainties, industry data showed Wednesday. According to the data from corporate tracker CEO Score, 500 listed midsized firms posted a combined operating profit of 6.34 trillion won ($4.55 billion) in the January-June period, down 4.1 percent from 6.62 trillion won a year ago. (source Korea Times)

- The KOSPI is down for a third straight day by -1.2% and is down by more than 3% for the week.

- The Won is one of the worst regional performers down -0.48% at 1,398.85

- Bonds are marginally better with the KTB 10yr at 2.86%

ASIA FX: KRW & TWD Dragged Down By Equity Market Losses

KRW and TWD have been the underperformers in the first part of Wednesday trade. This fits with accelerating equity market losses, led by the tech side. The won is down close to 0.60%, challenging the 1400 area, while TWD has lost close to 0.50%. USD/CNH is little changed, holding under 7.1900 at this stage. USD/HKD is up a little, last back close to 7.8080, after testing sub the mid-point of the band yesterday.

- Taiwan equities are tracking down by 2.6% today, the worst performer in the region. From US Tuesday trade, we saw some profit-taking after stalling around 6500 for the main US benchmark, as the market awaits Powell's Jackson Hole speech. Big Tech was hardest hit, having the largest concentration of positioning.

- This has spilled over into regional equities today, with tech sensitive plays underperforming. With the recent turn in equity flows moving out of Taiwan and South Korea, we could see more FX weakness. Spot USD/TWD is back above 30.25. May 13 highs around 30.46 may be the next upside target.

- Spot USD/KRW is challenging resistance at 1400. This puts us through all key EMAs. Earlier August intra-day highs were at 1406.45 in terms of further upside targets.

ASIA FX: USD/Asia Pairs Mostly Higher In SEA, But Some Resistance Seen

In South East Asia FX, the bias has also been for higher USD levels, although dollar gains have not been as strong as those seen against KRW and TWD. Losses are mostly more in the 0.20-0.25% region. This also fits with more muted equity price action in these markets.

- Spot USD/IDR has tested back above 16300, but sits back in the 16285/90 region in latest dealings, still off around 0.25% in IDR terms. We have unwound all of the mid August gains, although highs at the start of the month were just above 16500. Sensitivity will remain to the US Fed outlook, with any paring of easing expectations likely to push the pair higher.

- USD/PHP is facing a similar backdrop. In early trade we got to 57.376, but sit back in the 57.20/25 in latest dealings, leaving us close to multi week highs.

- USD/THB probed above 32.60 before finding some selling interest. Headlines crossed from a BoT interview on BBG. "*PITI: BOT HAS NO TARGET ON BAHT LEVEL, *PITI: BOT MOSTLY DEALS WITH EXCESSIVE VOLATILITY" - BBG, "*BOT DOESN'T HAVE MUCH ROOM FOR FURTHER RATE CUTS: PITI" - BBG

- USD/INR found support under 87.00 once again. The pair last close to 87.08. The rupee is still holding the bulk of its recent gains though. So far today we are seeing a steadier local equity market backdrop, so outperformance against some of the other markets. Rtrs noted earlier: "India and China agreed on Tuesday to resume direct flights and step up trade and investment flows as the neighbours rebuild ties damaged by a 2020 border clash." This is likely aiding broader Indian asset sentiment at the margins.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 20/08/2025 | 0600/0700 | *** | Consumer inflation report | |

| 20/08/2025 | 0600/0800 | ** | PPI | |

| 20/08/2025 | 0710/0910 | ECB Lagarde at WEF Intl Business Council | ||

| 20/08/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 20/08/2025 | 0900/1100 | *** | HICP (f) | |

| 20/08/2025 | 0900/1100 | Q2 Flash Vacancies and Labour Cost Index | ||

| 20/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 20/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 20/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 20/08/2025 | 1500/1100 | Fed Governor Christopher Waller | ||

| 20/08/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 20/08/2025 | 1800/1400 | FOMC Minutes | ||

| 20/08/2025 | 1900/1500 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 21/08/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 21/08/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/08/2025 | 0600/0800 | ** | Norway GDP | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 21/08/2025 | 0900/1100 | ** | Construction Production | |

| 21/08/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 21/08/2025 | 1130/0730 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 21/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 21/08/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 21/08/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Services Index (flash) |