GOLD: Gold Holds Losses, Fed Speakers & Minutes Later

Gold has been range trading today falling to $3311.6/oz before rising to $3319.59. It is currently 0.1% higher around $3318.8 holding onto Tuesday’s losses driven by steps taken towards a Ukraine truce. With markets hoping Fed Chair Powell will reveal his thinking for the September 17 decision on Friday, they are moving in narrow ranges. US yields are little changed and the USD index is 0.1% higher.

- Silver is down 0.5% to $37.212 off the intraday low of $37.170. A clear break of the 50-day EMA at $37.077 is needed to strengthen the short-term bearish threat. Initial resistance is at $39.655.

- Equities are also generally weaker with the Nikkei down 1.7%, Hang Seng -0.6% and S&P e-mini -0.3%. Oil prices are moderately higher with WTI +0.4% to $61.99/bbl. Copper is up slightly.

- Later the Fed’s Waller and Bostic appear and the July FOMC meeting minutes are published. UK July CPI & PPI, euro area July CPI and German July PPI print. ECB President Lagarde appears on a panel.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Crude Range Trading, Currently Slightly Higher

Oil prices continue to range trade and are slightly higher in today’s APAC trading after declining moderately on Friday. There has been little new information today to drive direction. Brent is up 0.1% to $69.36/bbl and WTI is +0.3% to $67.52/bbl.

- The oil market continues to monitor geopolitical developments closely with trade talks with the US continuing ahead of the August 1 deadline. Energy prices have been very sensitive to tariff developments as it remains worried that increased US protectionism will reduce global fuel demand. The EU is preparing counter measures if negotiations are unsuccessful.

- Russia’s role as a major fossil fuel exporter remains important too with the EU & UK announcing more restrictions including a reduction in the price cap for Russian crude; however the US is yet to follow. There will also be further targeting of its shadow fleet as well as another 20 banks losing access to the global payments system SWIFT.

- Limitations on third country refined products from Russian crude are also to be introduced, which will especially impact India. China has also protested the decision.

- Later the US June leading index and Bank of Canada Q2 outlook survey are released.

AUSSIE BONDS: Subdued Session Ahead Of RBA Mins & RBA Speech Tomorrow

ACGBs (YM -0.5 & XM +0.5) are little changed after trading in narrow ranges on a local data-light session.

- Cash US tsys are closed in today's Asia-Pac session with Japan out for the Marine Day holiday. TYU5 trades slightly higher at 110-26+.

- Cash ACGBs are little changed.

- The bills strip is slightly weaker, with pricing -1 to -3.

- RBA-dated OIS pricing is 3-13bps softer across meetings versus Thursday's pre-employment data levels. A 25bp rate cut in August is given a 98% probability, with a cumulative 66bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar will be empty, ahead of the RBA Minutes for the July Meeting tomorrow.

- A new 21 October 2036 Treasury Bond is planned to be issued via syndication this week (subject to market conditions).

- The focus this week is likely to be on the RBA, with the July meeting minutes published on Tuesday and Governor Bullock speaking at the Anika Foundation lunch on Thursday. Both will be monitored for further information on what lies behind the unexpected decision to hold and the central bank's thinking following the disappointing June jobs data.

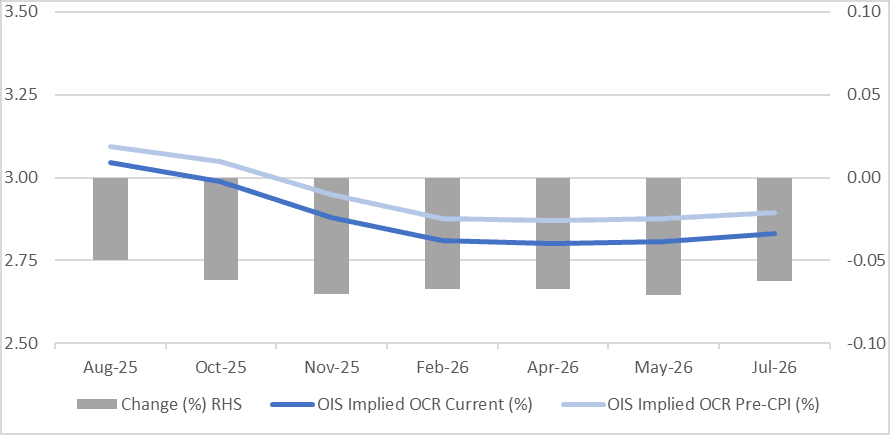

STIR: RBNZ-Dated OIS Softer After Q2 CPI Miss

RBNZ-dated OIS pricing closed 5-8bps softer across meetings following today's Q2 CPI data..

- NZ CPI rose less than economists expected in Q2. Headline CPI rose 0.5% q/q 2.7% y/y (estimate +0.6% and 2.8%). Tradeables rose 0.3% q/q, less than forecast, while non-tradeables were in line at 0.7% q/q.

- 21bps of easing is priced for August, with a cumulative 37bps by November 2025 versus 16bps and 30bps prior to the data.

Figure 1: RBNZ Dated OIS Post-CPI vs. Pre-CPI (%)

Source: Bloomberg Finance LP / MNI