GOLD: Gold Continues Range Trading

Gold fell 0.5% to $3315.78/oz on Tuesday, close to the intraday low, as markets position themselves ahead of Fed Powell’s speech on Friday. Not a quite full 25bp Fed Funds cut is priced for September 17 and this appearance will be watched closely for the Chair’s thinking on the immediate policy outlook. Meanwhile, President Trump continues to put pressure on Powell. The US dollar was stronger with the BBDXY up 0.15% but Treasury yields slightly lower. Bullion has started today around $3314.7.

- Gold continues to range trade between support at $3268.2, 30 July low, and resistance at $3409.2, 8 August high, but appears to be corrective. However, moving average studies continue to signal that the metal remains in a bull mode.

- Silver underperformed dropping 1.7% to $37.393 after a low of $37.280. It had reached $38.149 before the decline. It is currently around $37.370. Technicals continue to signal that silver is in an uptrend. A clear break of the 50-day EMA at $37.077 is needed to strengthen the short-term bearish threat. Initial resistance is at $39.655.

- Equities were mixed with the S&P down 0.6% but Euro stoxx up 0.9%. The S&P e-mini is so far slightly lower today. Oil prices continued falling with WTI -1.4% to $62.51/bbl. Copper is down 0.9%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

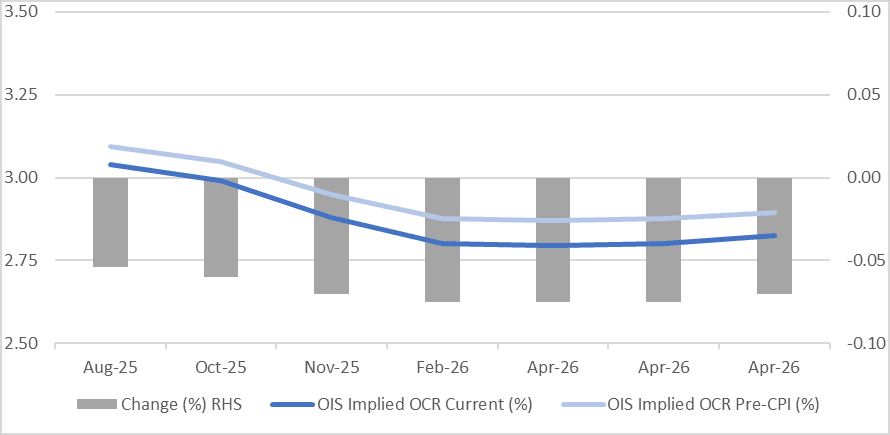

STIR: RBNZ-Dated OIS Softer After Q2 CPI Miss

RBNZ-dated OIS pricing is 5-8bps softer across meetings following today’s Q2 CPI data.

- While Q2 NZ headline CPI picked up 0.2pp to 2.7% y/y, it was less than expected and only 0.1pp above the RBNZ’s May forecast, and so well within usual errors. Thus, the RBNZ is likely to cut rates 25bp when it announces its decision on August 20.

- There was also a moderation in domestically driven non-tradeables inflation to its lowest in four years.

- 21bps of easing is priced for August, with a cumulative 37bps by November 2025 versus 16bps and 30bps before the data.

Figure 1: RBNZ Dated OIS Post-CPI vs. Pre-CPI (%)

Source: Bloomberg Finance LP / MNI

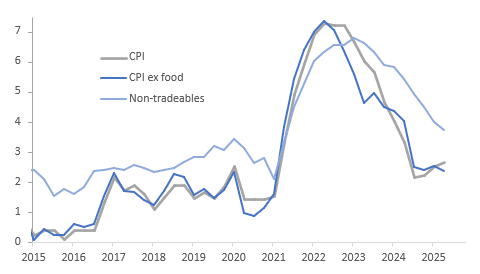

NEW ZEALAND: Inflation Low Enough For August Cut, Core Out Later Today

While Q2 NZ headline CPI picked up 0.2pp to 2.7% y/y, it was less than expected and only 0.1pp above the RBNZ’s May forecast and so well within usual errors. Thus the RBNZ is likely to cut rates 25bp when it announces its decision on August 20. There was also a moderation in domestically-driven non-tradeables inflation to its lowest in four years.

- Q2 CPI rose 0.5% q/q, in line with RBNZ expectations, bringing the annual rate to 2.7% from 2.5%, the highest in a year. Higher food prices, which had been signalled by the monthly data, were a reason for the pickup as CPI ex food rose 0.2% q/q and 2.4% y/y, down from 2.5% in Q1, the lowest since Q1 2021.

- The monthly data had also flagged a strong rise in electricity prices which rose 4.9% q/q and contributed 25% of the quarterly CPI increase, according to Statistics NZ.

- Non-tradeables rose 0.7% q/q to be up 3.7% y/y after 4.0%, while tradeables rose 0.3% q/q to be up 1.2% y/y following Q1’s 0.3%.

- Non-tradeables inflation was supported by the 12.2% y/y increase in local authority rates, but it will be updated in Q3 to capture July 1 rises. Rents rose 3.2% y/y, the lowest since 2021.

- RBNZ data on core inflation from its sector factor model will be released at 1300 AEST/1500 NZST today.

NZ CPI y/y%

AUSSIE BONDS: Little Changed After A Moderately Strong Friday For US Tsys

ACGBs (YM -1.0 & XM -1.0) are little changed despite a moderately strong close for US tsys on Friday.

- FT - "Donald Trump has escalated his demands in trade negotiations with the EU, pushing for a minimum tariff of 15 to 20 per cent in any deal with the bloc, according to three people briefed on the talks.”

- The U.Mich consumer survey saw inflation expectations surprise lower in the preliminary July survey, with the 1Y at 4.4% (cons 5.0 after 5.0 in June) and 5-10Y at 3.6% (cons 3.9 after 4.0 in June). The 1Y is the lowest since January and the 5-10Y is the lowest since February.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at -7bps.

- The bills strip is little changed.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in August is given a 99% probability, with a cumulative 66bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar will be empty, ahead of the RBA Minutes for the July Meeting tomorrow.

- A new 21 October 2036 Treasury Bond is planned to be issued via syndication this week (subject to market conditions).