RBNZ: OCR Path “Signals” Further Easing

The pace of NZ’s economic recovery appears to have disappointed the MPC with Q2 GDP expected to contract again. The MPC decided to cut rates 25bp to 3% by a vote of 4-2 with two members voting for a 50bp reduction. The MPC said that the OCR path was a “central expectation” “needed to ensure inflation” is sustainably at the band mid-point and it was revised lower which was said to likely provide “sufficient signalling effects”. The revised OCR path now troughs 30bp below the May assumption at 2.55% - the bottom of the RBNZ’s estimated neutral range.

- The revised OCR path implies another 43bp of easing by year end with 16bp in Q1 2026. This suggests that the last two meetings of 2025 on October 8 and November 26 are both “live” with around an even possibility of another one in February 2026. However, the MPC was clear that it remains highly data dependent.

- Headline inflation was revised higher over H2 2025 and H1 2026 and is forecast at 2.2% in Q4 2026 with it not returning to the 2% mid-point of the target band until H1 2027. It is now expected to be at the top of the band in Q3 2025.

- Rates were cut by 25bp as upside and downside risks were seen as “broadly balanced”, financial conditions continue to ease due to previous cuts and the OCR would signal the MPC’s easing bias.

- The case for a 50bp cut included “declining inflationary pressure and significant spare capacity”, global uncertainty could have “self-reinforcing” effects on domestic demand, a larger cut would send a clearer signal and excess capacity would put downward pressure on inflation.

- Arguments to hold rates were discussed which included global uncertainty had eased since May, the full effect of previous easing was yet to be felt, July data “suggest some improvements” and inflation is close to the top of the band and near-term expectations are rising. One member supported this view.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

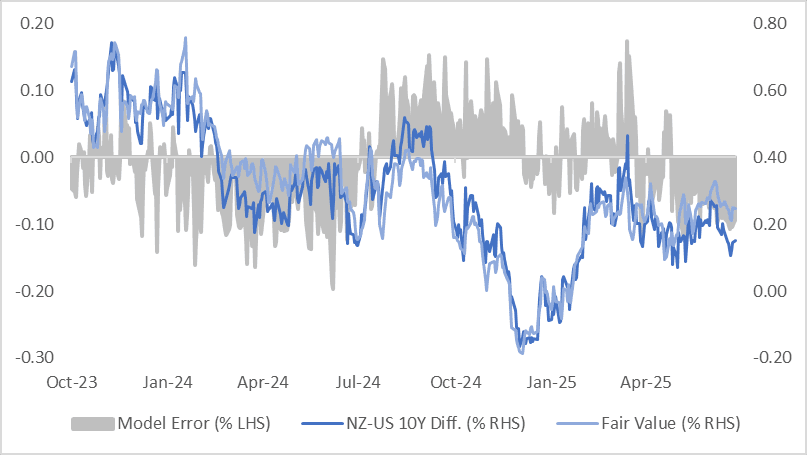

BONDS: NZ-US 10Y Differential Near Mid-Point Of This Year’s Range

NZGBs are 3-5bps richer today on the day and after today’s Q2 CPI data.

- With cash U.S. Treasuries not trading during today’s Asia-Pac session (due to the Japan holiday), and U.S. futures trading slightly higher, the move leaves the NZ–US 10-year yield differential around +15bps.

- At this level, the spread remains near the midpoint of the -20bps to +40bps range observed year-to-date.

- However, a simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the differential is currently about 10bps below its estimated fair value of +25bps.

- The regression’s standard error has remained within ±15bps over the past year, underscoring some inherent variability in the relationship.

- The 1Y3M spread continues to anchor market expectations around the longer-term path of yield convergence.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

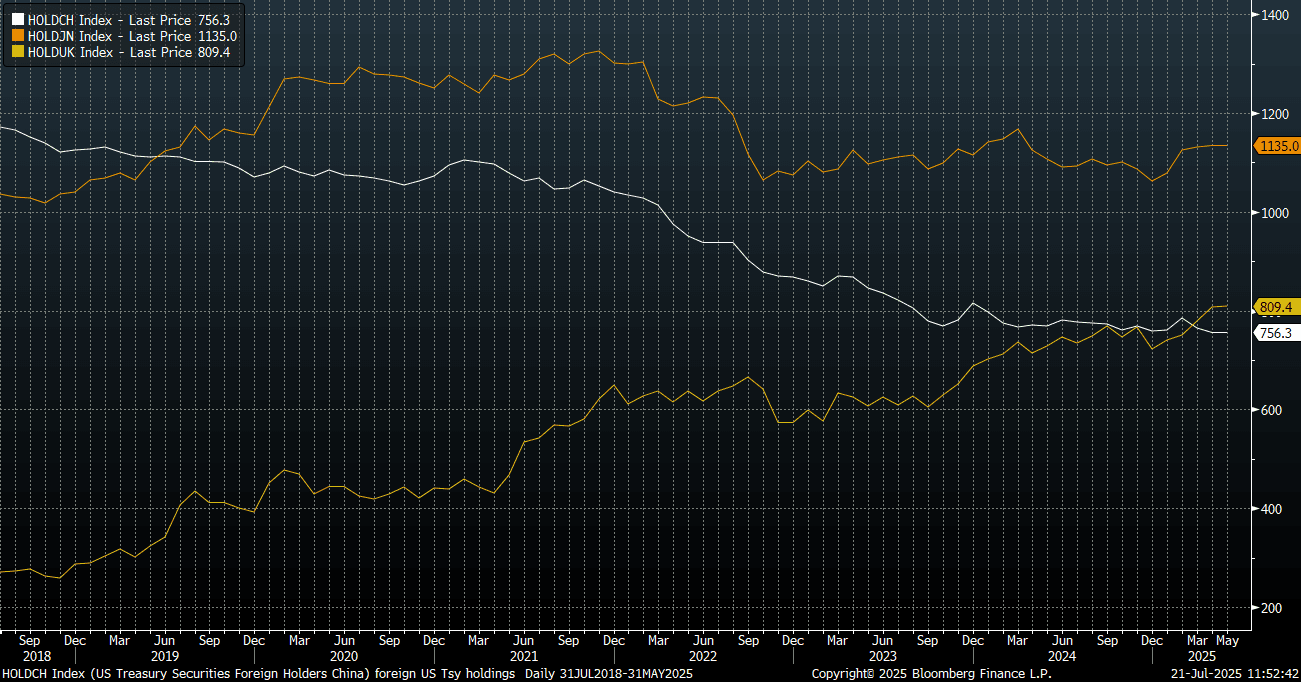

CHINA: China To Reduce UST Holdings Further

- A news article from the Government run China Daily this morning indicates that a strategic move is beginning in China, that may have profound implications for the US and their fiscal position.

- China Daily reports that is is a 'strategic necessity' for the scaling back of holdings in US Treasuries, given the declining confidence in the dollar as the reserve global currency.

- The article states that China intends to pursue a more balanced, controllable allocation of FX reserves and likely to increase its holdings of non-dollar assets, including financial instruments of Asian trading partners.

- Yu Yongding, an academic member of the Chinese Academy of Social Sciences, called for China to continue reducing US government debt holdings in an orderly manner and that in extraordinary times, extraordinary measures are called for.

- The latest Treasury holding data shows the UK taking over China as the third largest holder of US Treasury securities, see the chart below (China holdings are the white line).

- China has total holdings of USD 756.3 billion, to now rank third in largest holdings behind Japan and UK, according to US Treasury data. This shift marks a significant moment in the global financial landscape. The last time the UK ranked ahead of China in US debt ownership was in 2000—more than two decades ago. China holdings have flatlined somewhat in recent years, after falling through much of 2021-2023.

- The Governor of the PBOC Pan Gongsheng has been clear in his assessment of the risks associated with the USD dominance and that the fiscal position of the US economy, could spill over into global markets.

- China's FX reserves recently increased to US$3.32tn, its highest level in a decade.

Fig 1: China, Japan and UK Treasury Holdings

Source: Bloomberg Finance L.P./MNI

LNG: Gas Prices Driven By Weather Forecasts

European gas fell 2.0% to EUR 33.71 on Friday off the intraday low of EUR 33.41. It reached EUR 36.32 on July 14 but is still up 2.5% over the month. Forecasts for cooler weather over the rest of July have pressured prices more recently.

- The EU announced a reduction in the price cap for Russian crude and further targeting of its shadow fleet as well as measures impacting refined products and another 20 banks losing access to the global payments system SWIFT. It continues to plan a phase out of Russian gas imports.

- Norway’s Gassco announced an unplanned outage impacting 8.0 mcm/d from yesterday.

- Chevron stated that full LNG production has resumed at its Australian Gorgon export facility after repairs to Train 3 began.

- US natural gas is down 4.9% in Monday’s trading to $3.39. It rose 0.7% to $3.57 on Friday to be up 3.2% this month. The slight increase was driven by forecasts of warmer weather for the southern US towards the end of July (Atmospheric G2) thus increasing the prospect of a pickup in cooling demand.

- Ample inventories continue to keep a lid on any price rises as storage stands 6.2% above the 5-year average, according to Bloomberg. Lower-48 US production rose 5.3% y/y on Friday, while demand fell 0.3% y/y.