AUSSIE BONDS: Holding Richer After RBNZ's Forward Guidance

ACGBs (YM +4.5 & XM +3.5) are richer but off session bests.

- The local market has benefited from positive spillover from a strong post-RBNZ rally in NZGBs.

- The RBNZ cut the OCR by 25bps to 3.0%, as expected (4-2 vote; some favoured a 50bp cut), with forward guidance that saw the OCR averaging 2.71% in 4Q 2025, 2.56% in 2Q 2026, and 2.59% in 3Q 2026 (down from May's trough forecast of 2.9%). It indicated scope for further rate cuts if inflation pressures ease; forecasts imply a good chance of two more 25bp cuts.

- Cash US tsys are little changed in today's Asia-Pac session after modest gains.

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at -2bps.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in September is given a 30probability, with a cumulative 37bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will see S&P Global PMIs (P) and Consumer Inflation Expectation data.

- The AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Bullion Slightly Higher But Little New Information

After rising a moderate 0.3% on Friday, gold prices are +0.2% during today’s APAC trading following a variety of Fed views on the impact of tariffs and thus on rates. Fed Chair Powell gives some opening remarks on Tuesday. Bullion reached a high of $3358.63/oz earlier in the session but has now eased to $3355.9 to be up around 1.6% in July. The US dollar today is also fairly steady in today’s session.

- Geopolitical uncertainty remains high with the EU set to meet with Iran this week to discuss its nuclear programme and numerous trade talks with the US continuing ahead of an August 1 deadline.

- The bull cycle begun on June 30 is intact with bullion up 1.6% this month. Medium-term trend conditions are bullish. Initial resistance is at $3377.4, 16 July high, with the bull trigger at $3500.1. The bear trigger is at $3248.7.

- Silver is 0.1% higher at $38.21 down from the intraday high of $38.33. It is now up 5.7% in July. Technical signals continue to point to an uptrend as the metal remains above key short-term resistance at $37.32. Moving average studies are also in a bull mode. Initial resistance is at $39.13, 14 July high, while support is at $36.98, 20-day EMA.

- Equities are mixed with the S&P e-mini up 0.1%, Hang Seng +0.3% but the ASX down 1.1%. Oil prices are moderately higher with WTI +0.3% to $67.52/bbl. Copper is down 0.1%. UST futures aren’t trading due to a holiday in Japan.

- Later the US June leading index and Bank of Canada Q2 outlook survey are released.

BONDS: NZGBS: Closed On A Strong Note After CPI Data

NZGBs closed just off session bests, with benchmark yields 3-4bps lower.

- The RBNZ’s sector factor model result for Q2 was in line with other underlying CPI measures, showing that core inflation remained below the top of the 1-3% target band. Its measure of core inflation eased 0.1pp to 2.8% y/y, the lowest rate since Q2 2021, and is now only 0.1pp above headline CPI. Thus, with activity data still lacklustre, another 25bp rate cut on August 20 seems likely.

- With cash US tsys not trading during today’s Asia-Pac session (due to the Japan holiday), and US futures trading slightly higher, today’s move leaves the NZ–US 10-year yield differential around +16bps. At this level, the spread remains near the midpoint of the -20bps to +40bps range observed year-to-date.

- Swap rates closed 2-6bps lower, with the 2s10s curve steeper.

- RBNZ-dated OIS pricing is 5-8bps softer across meetings following today’s Q2 CPI data. 21bps of easing is priced for August, with a cumulative 37bps by November 2025.

- Tomorrow, the local calendar will see Trade Balance data.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.0% Apr-29 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 5.0% May-54 bond.

JPY: Asia Wrap - USD/JPY Claws Back Early Gap Lower

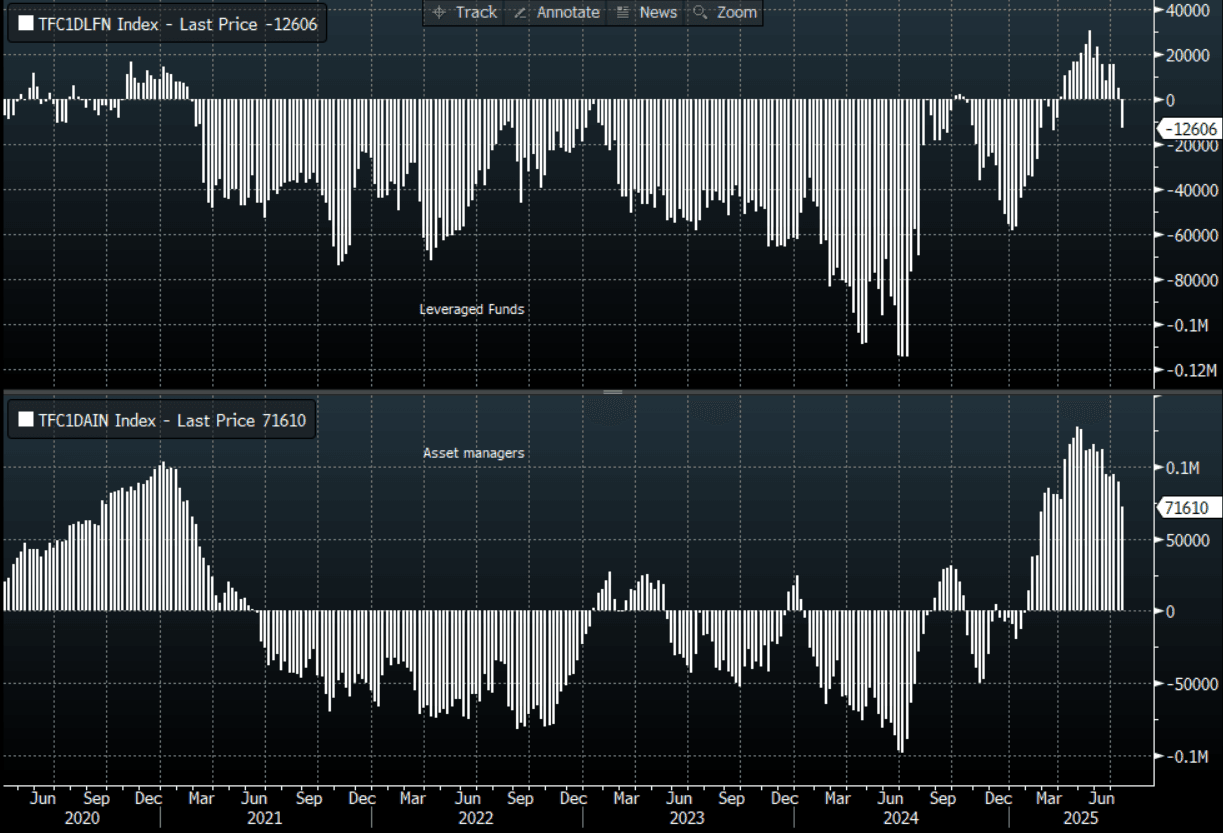

The Asia-Pac USD/JPY range has been 147.91 - 148.66, Asia is currently trading around 148.50, -0.20%. USD/JPY gapped lower on its open in a surprising reaction to the ruling coalition losing its upper house majority. The risk back drop still looks pretty good and this election outcome should only add to the headwinds for JPY longs, was this morning's reaction a “buy the rumour sell the fact” ? I expect there will continue to be demand on dips in the short-term, first support towards 147.00 then the important pivot area around 144/145. CFTC Data shows a clear turning in sentiment now as Asset managers reduced their shorts meaningfully and Leveraged accounts actually began to build JPY shorts.

- Focus will be on whether Ishiba is able to stay in the PM role. Bloomberg notes: "The last three LDP prime ministers who lost an upper house majority stepped down within two months, including Shinzo Abe in 2007 during his first stint as premier." But adds: "The opposition is split among roughly a dozen parties that are too fractured to pull together any kind of stable alternative if it brings a no-confidence vote against Ishiba, meaning the LDP will probably trudge along by cutting deals to cobble together support on an issue-by-issue basis."

- (Bloomberg) - “Dollar-yen may climb above 152 as Japan’s ruling Liberal Democratic Party and its partner Komeito grapple with their poor showing at Sunday’s upper-house election, according to HSBC. Yen weakness may overshoot if the Bank of Japan sees the need to adjust its JGB purchases to smooth potential bond market volatility, Paul Mackel, global head of FX research, writes in a note.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.50($1.29b).Upcoming Close Strikes : 147.00($1.44b July 22), 147.50($1.45b July 24), 147.00($495m July 24) - BBG.

CFTC data shows Asset managers starting to reduce JPY longs more aggressively +71610, while leveraged funds have started to build into a new short JPY position -12606.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P