AUSSIE BONDS: ACGB May-32 Auction Result

The AOFM sells A$1500 million of the 1.25% 21 May 2032 bond, #TB158:

- Average Yield (%): 3.9240 (prev. 4.2349)

- High Yield (%): 3.9250 (prev. 4.2375)

- Bid/Cover: 2.9267x (prev. 4.4486x)

- Allotted at Highest Accepted Yld as % of Bid at that Yld (%): 66.2 (prev. 19.8)

- Bidders: 34 (prev. 38), 17 (prev. 16) successful, 6 (prev. 7) allocated in full

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

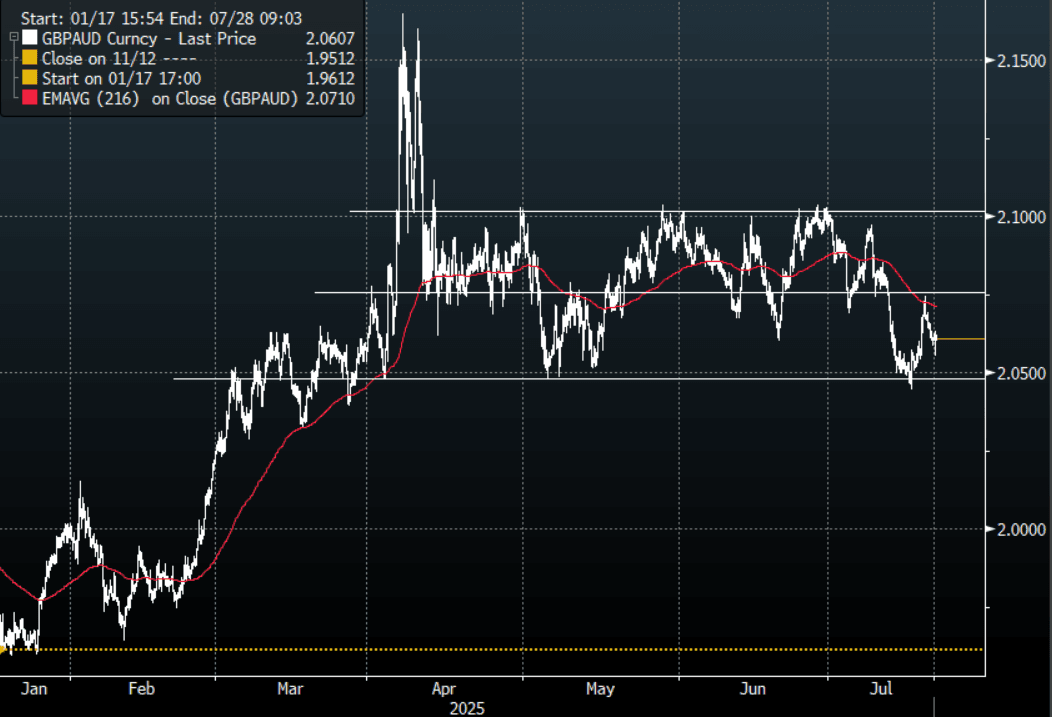

FOREX: AUD Crosses - Trade Sideways, AUD/NZD Reacts To NZ CPI

US stocks are consolidating near their new all-time highs. This morning has seen US futures open slightly higher, ESU5 +0.12%, NQU5 +0.13%. The AUD trades sideways in the crosses as awaits a catalyst for some clearer direction.

- EUR/AUD - Friday night range 1.7833 - 1.7875, Asia is currently trading around 1.7865. The pair seems to be consolidating in a 1.7650 - 1.8050 range as the market awaits some clearer direction.

- GBP/AUD - Friday night range 2.0585 - 2.0650, Asia is trading around 2.0605. The pair bounced nicely off its support around 2.0500 and last week but has found some good supply in exactly the right spot as well drifting back off from the 2.0750 area. This pair is also now back within its wider 2.0450 - 2.1050 range with the 2.0750/2.0800 area acting as the pivot.

- AUD/JPY - Friday night range 96.66 - 96.96, Asia is trading around 96.60. The pair strangely gapped lower on the open in reaction to the Japanese election result it found good demand back towards the breakout area around 96.00, and this will need to hold to build a platform from which to probe higher again. The positive risk backdrop is providing tailwinds. CFTC Data shows a clear turning now as Asset managers reduced their shorts meaningfully and Leveraged accounts actually began to build JPY shorts.

- AUD/NZD - Friday night range 1.0911 - 1.0931, the cross is dealing in Asia around 1.0950. The cross moved higher this morning in response to the NZ CPI. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: GBP/AUD spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

NEW ZEALAND: VIEW: Westpac Thinks CPI Below RBNZ Expectations, August Cut Likely

Q2 CPI rose 0.5% q/q to be up 2.7% y/y after 2.5% in Q1, slightly below the 0.6% that consensus and Westpac were forecasting. Westpac believes that while the quarterly rate was in line with the RBNZ’s May forecast, its “July policy statement indicated that they were braced for a stronger result”. It continues to expect a 25bp rate cut at the August 20 meeting but doesn’t think the inflation data did “much to change the RBNZ’s mind relative to the cautious easing bias it signalled at its recent policy review”.

- Westpac will continue to monitor “core inflation measures closely to see how strong the underling trend in prices is”. It also noted that “core inflation remains contained in the RBNZ’s target band. However, it isn’t dropping like it did last year and remains a little above 2%”. The RBNZ’s measure of core is released later today.

- “Trimmed mean inflation remained at 2.5%. Weighted median inflation fell to 2.2%. Inflation excluding food, fuel and energy costs nudged higher to 2.7% from 2.6% previously.”

- The easing in domestic inflation has been due to “the softness in domestic activity which has seen muted growth in wages and service sector prices. We’ve also seen an easing in rents and subdued increases in the cost of new housing. But even with that softness in domestic activity, overall non-tradables inflation has been easing only gradually over the past year due to continued increases in administered costs.”

- “Food prices (19% of the CPI) were the largest upside contributors to quarterly inflation, with prices up 1.6% over the quarter. … There has also been a large increase in household energy prices (3% of the CPI), with electricity prices up 4.7% over the quarter. That's in part due to increases in lines and transmission charges.”

- “On the downside, petrol prices (4% of the CPI) fell around 5% over the past few months.”

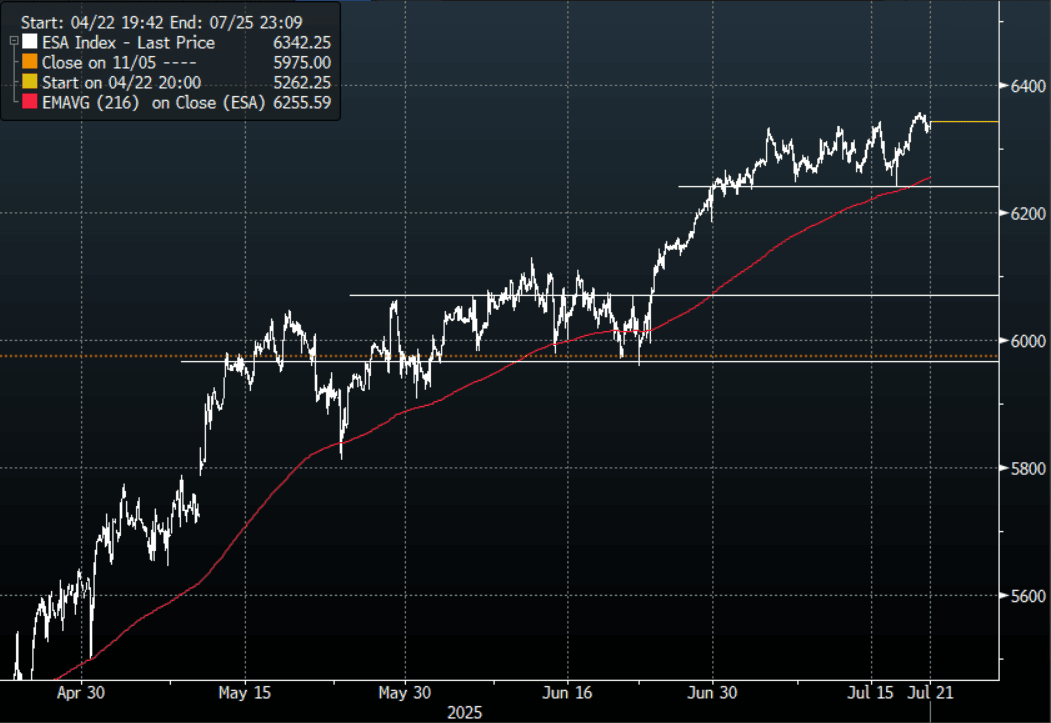

US STOCKS: S&P Consolidating Towards Its Highs

The ESU5 Friday night range was 6323.25 - 6357.00, Asia is currently trading around 6342. The September contract stalled just above the 0.6350 area but price continues to consolidate its recent gains. This morning has seen US futures open slightly higher, ESU5 +0.12%, NQU5 +0.13%. The animal spirits remain strong even though price is looking stretched. While above the 6230/50 area dips will probably continue to be supported, a break below this support is needed to signal a possible correction.

- (Bloomberg) - Big tech takes over the earnings season, with investors watching reports from the US’s Alphabet, Tesla, Intel, and SAP in Europe.

- Lance Roberts on X: “We bought some cheap "out of the money" S&P puts this past week. Stocks are at all-time highs. Gross equity exposure is at all-time highs. Cost to protect risk is extremely cheap. That isn't a hard call.”

- Sven Henrich on X: “Wild: The top 5 stocks in the NDX 100 comprise 52% of the index's combined market cap. The top 2 stocks, NVDA & MSFT, with $8 trillion in combined market cap, represent 27% of the index. Even wilder: Since the April lows both stocks show a 95% directional price correlation.”

- Daily Chartbook on X: “On Wednesday, "the US Treasury reported the largest inflow of foreign capital to that market (net purchases) since 2022, obliterating the narrative that foreign investors are fleeing Treasuries (or US equities) due to political risks."

- Short-term this continues to look stretched but it's very hard to fight a market with this type of momentum. First support is back towards the 6000/6100 area.

Fig 1: SPX(ESU5) 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P