ASIA STOCKS: Most Major Markets Weaker, Led By Tech Exposure

Some of the key Asian equity benchmarks are down sharply today, particularly those with a tech focus. This follows sharp US losses in this space during cash Tuesday trade. Tuesday saw some profit-taking after stalling around 6500 for the main US benchmark, as the market awaits Powell's Jackson Hole speech. Big Tech was hardest hit, having the largest concentration of positioning. We have also seen follow on US equity futures weakness, led by the tech side so far today. Nasdaq futures were last down a little over 0.50%, while Eminis were off close to 0.30%.

- There are some outperformers within Asia Pac so far today, with New Zealand up over 1.6% after the dovish RBNZ 25bps rate cut. The NZX 50 was last around Jan highs.

- Conversely, Taiwan's Taiex is down around 2.5%, while the Kospi is off close to 2%, as these markets feel the brunt of tech related sell-off. Offshore investors have turned net sellers of these markets in recent sessions as well.

- The NKY225 is down by around 1.8% in Japan, while the Topix is down by 0.75%.

- China's CSI 300 is down a modest 0.1%, while the HSI is down by nearly 0.6% at the lunch time break. The HSI tech sub index is off by 1.26% though.

- In South East Asia, Indonesia is outperforming modestly, up +0.55%, while most other markets are down a touch.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

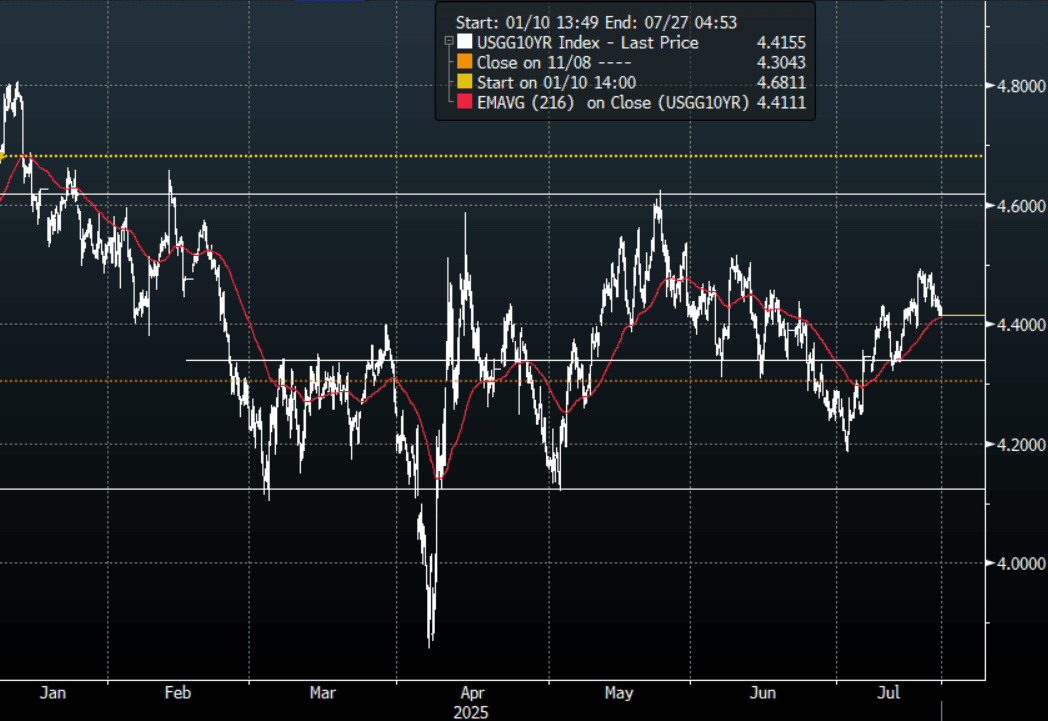

US TSYS: TYU5 Up Slightly On The Day

The TYU5 range has been 110-24 to 110-28 during the Asia-Pacific session. It last changed hands at 110-26, up 0-01 from the previous close.

- No Cash market today

- The 10-year yield broke above 4.45% in response to the CPI Data, this implies price is likely to turn its focus back to 4.65% and could see further paring back of longs. Support is now back towards the 4.35/40% area which has been the pivot in the larger 4.10% - 4.65% range.

- Daily Chartbook on X: “On Wednesday, "the US Treasury reported the largest inflow of foreign capital to that market (net purchases) since 2022, obliterating the narrative that foreign investors are fleeing Treasuries (or US equities) due to political risks.”@bespokeinvest

- “China Daily reports that it is a 'strategic necessity' for the scaling back of holdings in US Treasuries, given the declining confidence in the dollar as the reserve global currency.” - BBG

- (Bloomberg) -- “EU envoys will meet as early as this week to draft a retaliatory plan in response to a possible no-deal scenario with Donald Trump. The move follows a hardened stance from the US trade team ahead of the Aug. 1 deadline.”

Data/Events: Leading Index

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

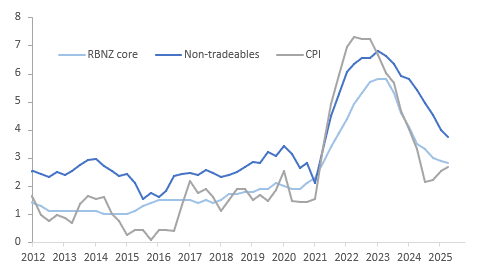

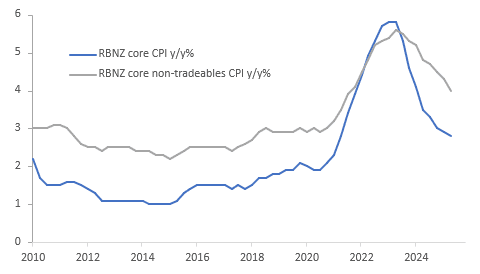

NEW ZEALAND: RBNZ Core Inflation Measure Moderates Slightly

The RBNZ’s sector factor model result for Q2 was in line with other underlying CPI measures showing that core inflation remained below the top of the 1-3% target band. Its measure of core inflation eased 0.1pp to 2.8% y/y, the lowest rate since Q2 2021, and is now only 0.1pp above headline CPI. Underlying non-tradeables also continued to moderate. Thus with activity data still lacklustre, another 25bp rate cut on August 20 seems likely coinciding with an update in staff forecasts.

NZ inflation y/y%

- The sector factor model’s estimate of core non-tradeable inflation declined to 4.0% y/y in Q2 from 4.3%, the lowest in almost 4 years. The headline measure dropped 0.3pp to 3.7%.

- Underlying tradeable inflation remained very low at 0.7% y/y up slightly from Q1’s 0.5%, compared to the headline at 1.2% y/y.

- Earlier today Q2 trimmed mean CPI was steady at 2.5% y/y but CPI ex food, fuel & energy ticked up 0.1pp to 2.7% y/y.

NZ underlying inflation y/y%

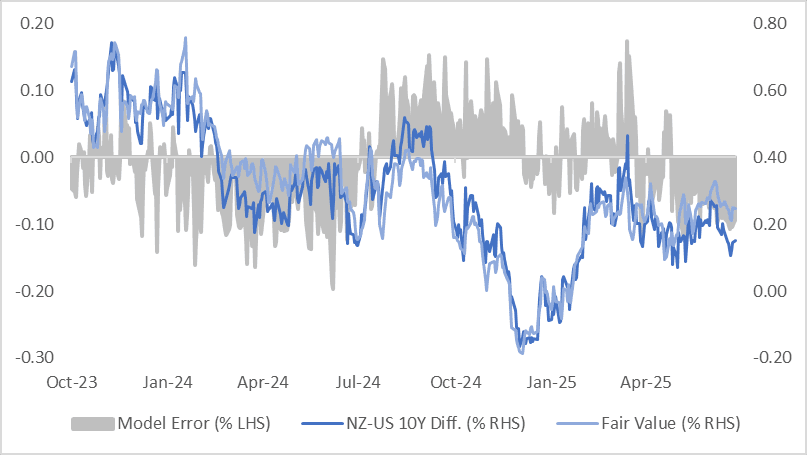

BONDS: NZ-US 10Y Differential Near Mid-Point Of This Year’s Range

NZGBs are 3-5bps richer today on the day and after today’s Q2 CPI data.

- With cash U.S. Treasuries not trading during today’s Asia-Pac session (due to the Japan holiday), and U.S. futures trading slightly higher, the move leaves the NZ–US 10-year yield differential around +15bps.

- At this level, the spread remains near the midpoint of the -20bps to +40bps range observed year-to-date.

- However, a simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the differential is currently about 10bps below its estimated fair value of +25bps.

- The regression’s standard error has remained within ±15bps over the past year, underscoring some inherent variability in the relationship.

- The 1Y3M spread continues to anchor market expectations around the longer-term path of yield convergence.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI