BONDS: NZGBS: RBNZ Forward Guidance Sparks Massive Rally

NZGBs closed 10-16bps richer, with a steeper 2/10 curve, after today’s RBNZ policy decision.

- The pace of NZ’s economic recovery appears to have disappointed the MPC, with Q2 GDP expected to contract again. The MPC decided to cut rates 25bp to 3% by a vote of 4-2, with two members voting for a 50bp reduction.

- The MPC said that the OCR path was a “central expectation” “needed to ensure inflation” is sustainably at the band mid-point and it was revised lower which was said to likely provide “sufficient signalling effects”. The revised OCR path now troughs 30bp below the May assumption at 2.55% - the bottom of the RBNZ’s estimated neutral range.

- The revised OCR path implies another 43bp of easing by year end with 16bp in Q1 2026.

- Swap rates closed 11-18bps lower, with a steeper 2s10s curve.

- RBNZ dated OIS pricing closed 14-23bps softer for meetings beyond August. 35bps of cumulative easing is priced by November 2025.

- Tomorrow, Governor Hawkesby will appear before a parliamentary committee to talk about the latest Monetary Policy Statement.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: Asia Wrap - USD/JPY Claws Back Early Gap Lower

The Asia-Pac USD/JPY range has been 147.91 - 148.66, Asia is currently trading around 148.50, -0.20%. USD/JPY gapped lower on its open in a surprising reaction to the ruling coalition losing its upper house majority. The risk back drop still looks pretty good and this election outcome should only add to the headwinds for JPY longs, was this morning's reaction a “buy the rumour sell the fact” ? I expect there will continue to be demand on dips in the short-term, first support towards 147.00 then the important pivot area around 144/145. CFTC Data shows a clear turning in sentiment now as Asset managers reduced their shorts meaningfully and Leveraged accounts actually began to build JPY shorts.

- Focus will be on whether Ishiba is able to stay in the PM role. Bloomberg notes: "The last three LDP prime ministers who lost an upper house majority stepped down within two months, including Shinzo Abe in 2007 during his first stint as premier." But adds: "The opposition is split among roughly a dozen parties that are too fractured to pull together any kind of stable alternative if it brings a no-confidence vote against Ishiba, meaning the LDP will probably trudge along by cutting deals to cobble together support on an issue-by-issue basis."

- (Bloomberg) - “Dollar-yen may climb above 152 as Japan’s ruling Liberal Democratic Party and its partner Komeito grapple with their poor showing at Sunday’s upper-house election, according to HSBC. Yen weakness may overshoot if the Bank of Japan sees the need to adjust its JGB purchases to smooth potential bond market volatility, Paul Mackel, global head of FX research, writes in a note.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.50($1.29b).Upcoming Close Strikes : 147.00($1.44b July 22), 147.50($1.45b July 24), 147.00($495m July 24) - BBG.

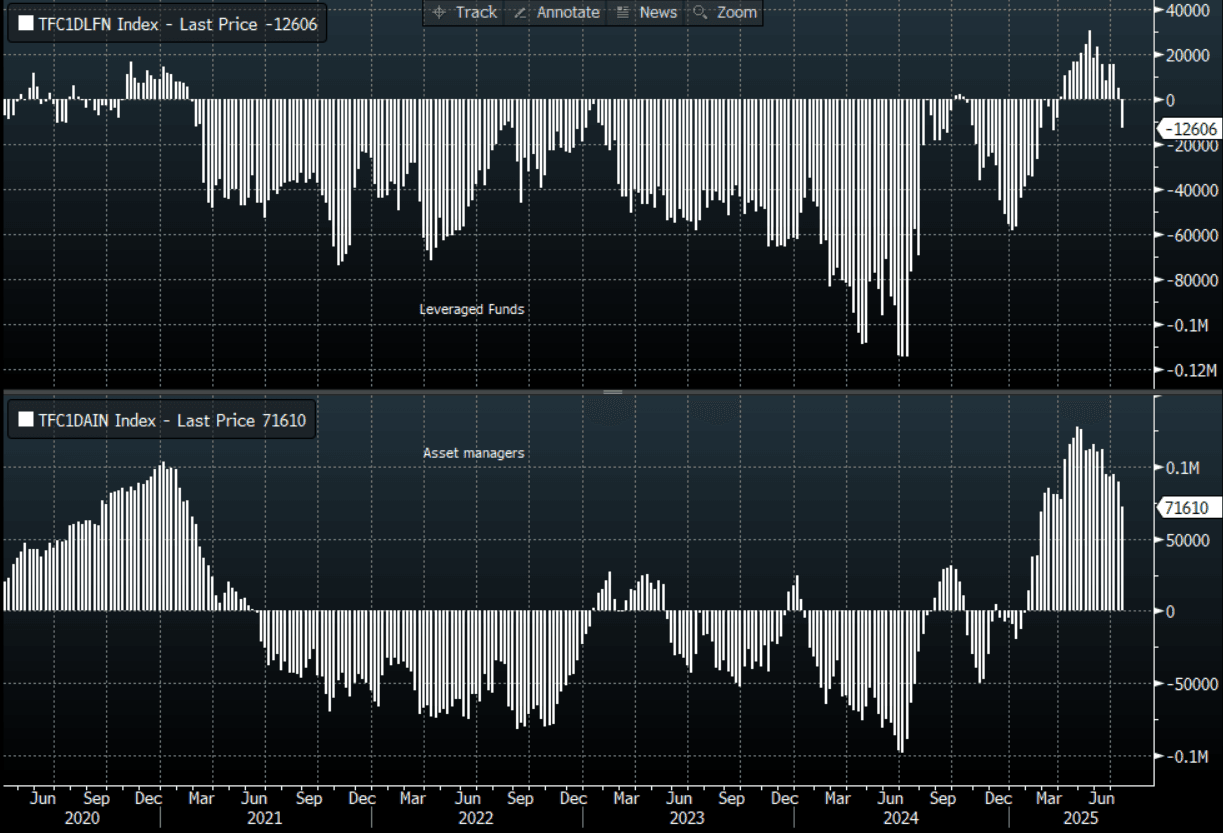

CFTC data shows Asset managers starting to reduce JPY longs more aggressively +71610, while leveraged funds have started to build into a new short JPY position -12606.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Positive Momentum Continues For HK/China, Aust Dip From Record

Regional Asia Pac stocks are off to a mixed start this week. This follows a fairly indifferent lead from offshore markets in Friday cash trade, with US bourses little changed. US futures are up a touch, while EU futures are down modestly so far today, as focus remains on EU/US trade outcomes. BBG reported that EU officials are meeting this week to plan retaliatory measures if no deal can be reached before the Aug 1 deadline.

- Japan markets are out, so we can't judge the market reaction to the weekend election result, where the ruling LDP coalition lost its majority. The result was in line with opinion polls from last week, while USD/JPY hasn't moved much so far today.

- China and Hong Kong markets are up around 0.25-0.30% so far today. The CSI 300 is building on recent positive momentum, with a weekend dam project approved aiding steel futures and iron ore prices, potentially providing some positive spill over. The index finished last week at fresh highs back to late last year. The HSI is off session highs, but still close to re-testing the 25000 level, which would be multi year highs back to 2022.

- Taiwan markets are down slightly, after a strong run through the tail end of last week. We were last down around 0.20% to 23330. The Kospi is higher though and aiming to close above 3200. Morgan Stanley raised the local index to market weight, citing reforms as a positive.

- Australia's ASX 200 has retreated from record highs and is underperforming so far today, the index down over 1%. Bank stocks underperformed in the first part of trade.

- In SEA, trends are mixed, with Malaysia and Thailand down modestly, while Indonesia is outperforming. The JCI was last around 0.80% higher and aiming to test the 7400 region.

AUD: AUD/USD - Consolidating Above 0.6500

The AUD/USD has had a range of 0.6498 - 0.6520 in the Asia- Pac session, it is currently trading around 0.6510, +0.02%. The pair found decent supply back towards 0.6550 again on Friday. The follow through below 0.6500 is quite disappointing for AUD shorts but with Stocks making new highs and risk outperforming, it makes it a hard environment for AUD/USD to collapse in. The Pair looks to be consolidating in a 0.6450 - 0.6600 range as the market awaits a catalyst to provide clearer direction.

- The focus this week is likely to be on the RBA with the July meeting minutes published on Tuesday and Governor Bullock speaking at the Anika Foundation lunch on Thursday. Both will be monitored for further information on what lay behind the unexpected decision to hold and central bank thinking following the disappointing June jobs data.

- China Daily - “reports that it is a 'strategic necessity' for the scaling back of holdings in US Treasuries, given the declining confidence in the dollar as the reserve global currency.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD729m), 0.6500(AUD821m) . Upcoming Close Strikes : 0.6650(AUD495m July 24) - BBG

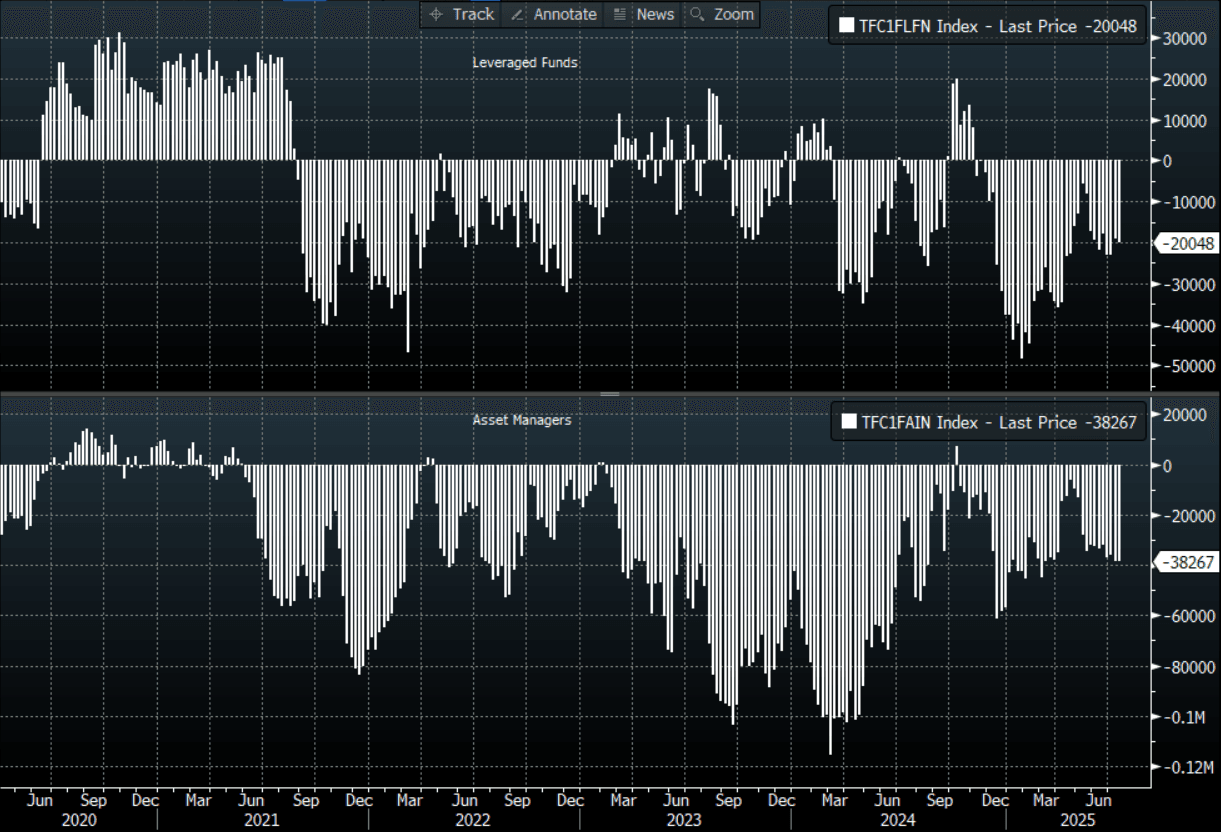

- CFTC Data shows Asset managers have maintained their shorts -38267, the Leveraged community added slightly to their shorts to -20048.

- AUD/JPY - Today's range 96.32 - 96.75, it is trading currently around 96.65, -0.20%. The pair strangely gapped lower on the open in reaction to the Japanese election result, it found good demand back towards the breakout area around 96.00, and this will need to hold to build a platform from which to probe higher again. The positive risk backdrop should provide tailwinds. CFTC Data shows a clear turning now as Asset managers reduced their shorts and Leveraged accounts actually began to build JPY shorts.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P