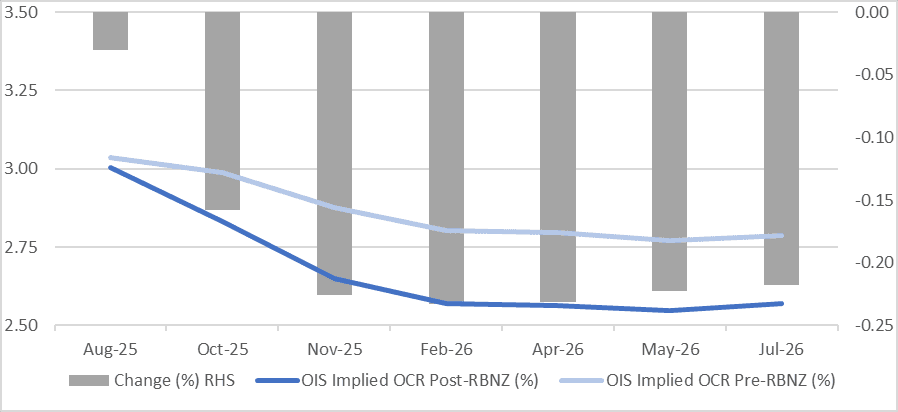

STIR: RBNZ-Dated OIS Shunt Softer After RBNZ Decision

RBNZ dated OIS pricing closed 14-23bps softer for meetings beyond August following today’s RBNZ Policy Decision.

- The market had priced 22bps of today’s 25bp cut going into the decision.

- 35bps of cumulative easing is now priced by November 2025 versus 12bps before the decision.

Figure 1: RBNZ Dated OIS Post-RBNZ vs. Pre-RBNZ (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Subdued Session Ahead Of RBA Mins & RBA Speech Tomorrow

ACGBs (YM -0.5 & XM +0.5) are little changed after trading in narrow ranges on a local data-light session.

- Cash US tsys are closed in today's Asia-Pac session with Japan out for the Marine Day holiday. TYU5 trades slightly higher at 110-26+.

- Cash ACGBs are little changed.

- The bills strip is slightly weaker, with pricing -1 to -3.

- RBA-dated OIS pricing is 3-13bps softer across meetings versus Thursday's pre-employment data levels. A 25bp rate cut in August is given a 98% probability, with a cumulative 66bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar will be empty, ahead of the RBA Minutes for the July Meeting tomorrow.

- A new 21 October 2036 Treasury Bond is planned to be issued via syndication this week (subject to market conditions).

- The focus this week is likely to be on the RBA, with the July meeting minutes published on Tuesday and Governor Bullock speaking at the Anika Foundation lunch on Thursday. Both will be monitored for further information on what lies behind the unexpected decision to hold and the central bank's thinking following the disappointing June jobs data.

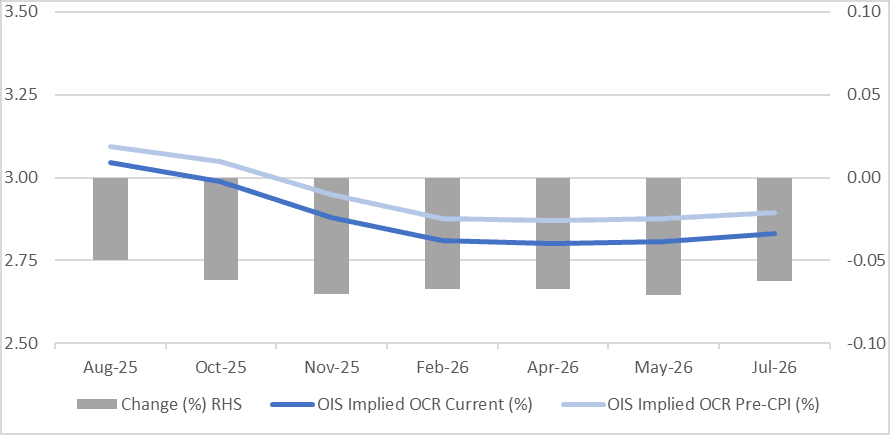

STIR: RBNZ-Dated OIS Softer After Q2 CPI Miss

RBNZ-dated OIS pricing closed 5-8bps softer across meetings following today's Q2 CPI data..

- NZ CPI rose less than economists expected in Q2. Headline CPI rose 0.5% q/q 2.7% y/y (estimate +0.6% and 2.8%). Tradeables rose 0.3% q/q, less than forecast, while non-tradeables were in line at 0.7% q/q.

- 21bps of easing is priced for August, with a cumulative 37bps by November 2025 versus 16bps and 30bps prior to the data.

Figure 1: RBNZ Dated OIS Post-CPI vs. Pre-CPI (%)

Source: Bloomberg Finance LP / MNI

NZD: Asia Wrap - NZD/USD Moves Lower On A Softer CPI Print

The NZD/USD had a range of 0.5939 - 0.5971 in the Asia-Pac session, going into the London open trading around 0.5950, -0.20%. A better than expected CPI print has seen the NZD move a little lower across the board. This 0.5850/0.5900 area is important support if the pair is to eventually push higher, a weekly close below 0.5850 would turn the picture quite bearish. Price will need a sustained break back above the 0.6025/50 area to signal a potential base might be in place.

- “RBNZ 2Q SECTORAL FACTOR MODEL INFLATION INDEX RISES 2.8% Y/Y" - BBG, Note the Q1 rise was 2.9%y/y for the sectoral inflation model.

- MNI NEW ZEALAND: Inflation Low Enough For August Cut, While Q2 NZ headline CPI picked up 0.2pp to 2.7% y/y, it was less than expected and only 0.1pp above the RBNZ’s May forecast and so well within usual errors. Thus the RBNZ is likely to cut rates 25bp when it announces its decision on August 20. There was also a moderation in domestically-driven non-tradeables inflation to its lowest in four years.

- NEW ZEALAND: VIEW: Westpac Thinks CPI Was Lower Than RBNZ Expected, Aug Rate Cut. Westpac believes that while the quarterly rate was in line with the RBNZ’s May forecast, its “July policy statement indicated that they were braced for a stronger result”. It continues to expect a 25bp rate cut at the August 20 meeting.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5905(NZD380m). Upcoming Close Strikes : 0.5750(NZD348m July 23). - BBG

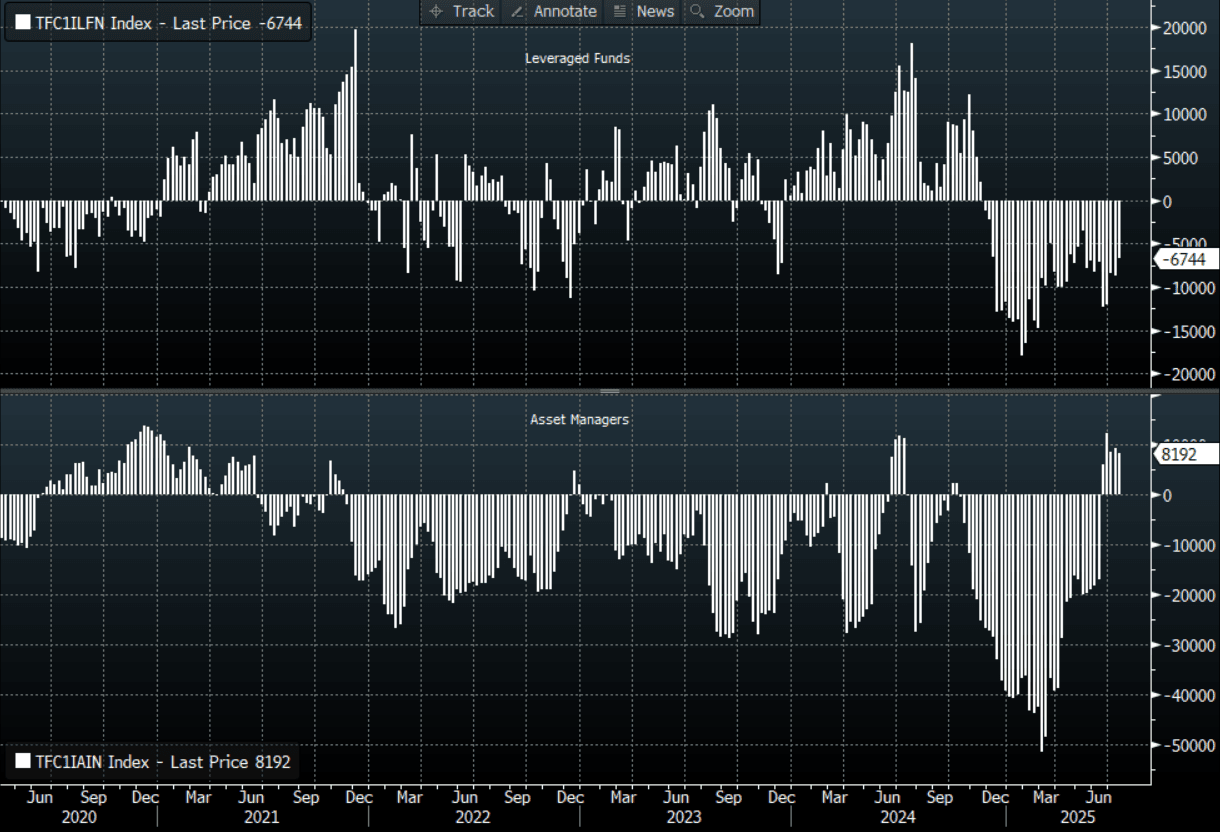

- CFTC Data shows Asset Managers slightly reduced their newly built longs in NZD +8192, the Leveraged community has continued to reduce their shorts last week -6744.

- AUD/NZD range for the session has been 1.0909 - 1.0950, currently trading 1.0935. The cross moved higher this morning in response to the NZ CPI. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P