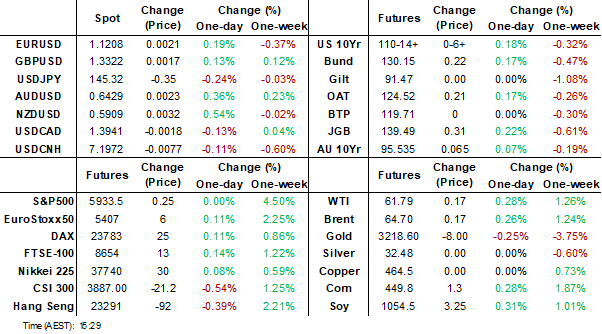

MNI EUROPEAN MARKETS ANALYSIS: Higher Inflation Exp Aids NZD

- The USD has remained on the backfoot, while Tsy yields have drifted a little lower.

- NZD/USD has outperformed following a rise in NZ inflation expectations, while Q1 GDP in Japan contracted but hasn't impacted local FX sentiment.

- Asia stocks are mixed today as the impetus given from the news of the trade truce fades away and a focus on fundamentals reasserts. Gold has remained volatile, giving back some of Thursday's gains.

- Looking ahead, the main focus will be on US data, particularly the May preliminary U. of Mich. sentiment read.

MARKETS

US TSYS: Asia Wrap - Yields Extend Lower

TYM5 has traded higher within a range of 110-10 to 110-15 during the Asia-Pacific session. It last changed hands at 110-13+, up 0-05 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.946%, down 0.01 from its close.

- The US 10-year yield has drifted lower, dealing around 4.424%, down 0.01 from its close.

- In the US, softer-than-expected retail sales and PPI data yesterday outweighed slightly lower jobless claims, prompting a modest dovish reaction in Fed pricing. Earlier in the week, CPI data came in broadly in line with expectations and had limited impact on market re-pricing.

- MNI BRIEF: US Firms Expect To Shed Jobs In 2025: U.S. purchasing and supply executives expect to shed jobs this year as tariffs, inflation and geopolitical uncertainty hold down growth, according to the Institute for Supply Management semiannual economic forecast released Thursday.

- The 10-year Yield could not maintain its foothold above 4.5%. A sustained break above this level could see another round of selling targeting the 4.75% area. Support now seen back towards 4.35/40% where supply should now be seen.

- Data/Events : Business Inventories, NAHB Housing Index, Housing Starts, Un of Mich sentiment

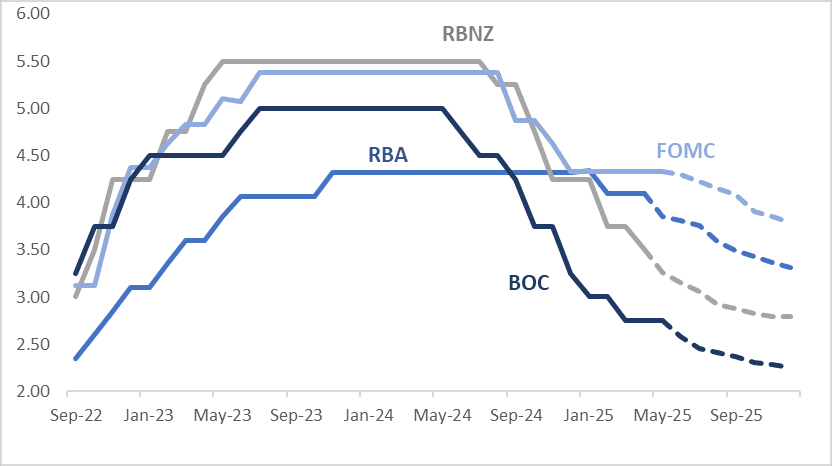

STIR: $-Bloc Markets Firm Over Past Week Led By Australia

Interest rate expectations across dollar-bloc economies have firmed through December 2025 over the past week — with the exception of Canada. Australia saw the most significant shift, with a 23bp rise in expected year-end rates, followed by the US (+16bps) and New Zealand (+6bps). In contrast, Canada’s implied rate softened by 8bps.

- In the US, softer-than-expected retail sales and PPI data yesterday outweighed slightly lower jobless claims, prompting a modest dovish reaction in Fed pricing. Earlier in the week, CPI data came in broadly in line with expectations and had limited impact on market re-pricing.

- In Australia, April employment data surprised to the upside with an 89k increase in jobs, while the unemployment rate held steady at 4.1%. The figures highlight continued labour market tightness, with employment growth keeping pace with labour force expansion. Combined with stronger-than-expected wage data earlier this week, the RBA may reinforce a more cautious stance on future easing. Nonetheless, it is unlikely to derail expectations for a 25bp rate cut at the RBA’s May 20 meeting.

- Across the $-bloc more broadly, markets appear content to consolidate recent hawkish repricing, which has largely stemmed from a reduction in downside risks, particularly surrounding trade policy, as headlines around potential deals gained traction.

- The next key event for the region is the RBA’s May 20 policy meeting, where a 25bp rate cut is currently fully priced in.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.79%, -54bps; Canada (BOC): 2.26%, -49bps; Australia (RBA): 3.31%, -79bps; and New Zealand (RBNZ): 2.79%, -71bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

JGBS: Modest Twist-Steepener After 1st GDP Contraction Since Q1-24

JGB futures are stronger, +22 compared to the settlement levels, but hovering near session cheaps.

- Japan Q1 GDP contracted for the first time since Q1 2024. Q/Q growth was -0.2% (-0.1% forecast and 0.6% prior), while in annualised terms we fell -0.7%, against a -0.3% forecast but Q4 revisions were higher to +2.4%.

- "With the economy already shrinking on the eve of the trade war, the Bank of Japan will probably wait even longer before resuming its tightening cycle than we had anticipated," said Marcel Thieliant, head of Asia-Pacific at Capital Economics.” (WSJ via BBG)

- For the BoJ/authorities, the rise in business spending will be encouraging but the flat consumption result will be a watch point. The policy aims remains for better spending outcomes boosted by positive real wages.

- BoJ Nakamura currently speaking.

- Cash JGBs have twist-steepened, pivoting at the 30-year, with yields 1bp lower to 1bp higher.

- In contrast, the swaps curve has twist-flattened with rates 1bp higher to 2bps lower.

- On Monday, the local calendar will see the Tertiary Industry Index alongside 1-year supply.

- The G7 will be holding a meeting from the 20th to the 22nd, there will be attention on any discussion between the US and Japan, particularly if foreign exchange rates are discussed concerning the tariffs.

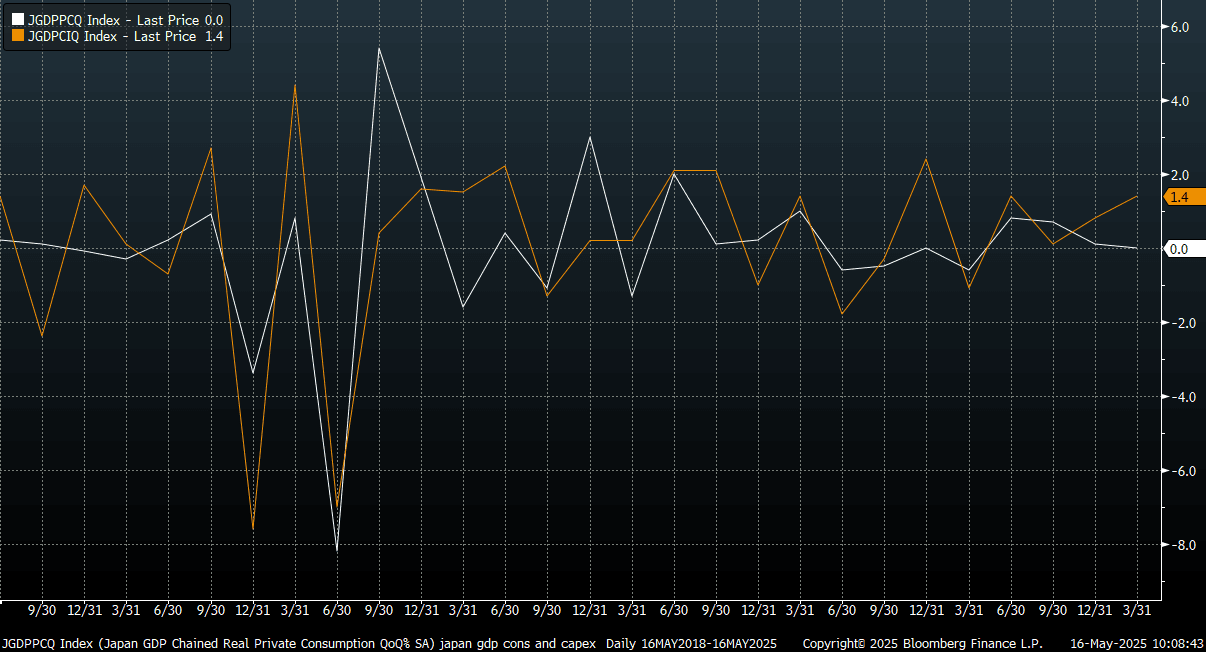

JAPAN DATA: Q1 GDP Contracts, Business Spending The One Bright Spot

Japan Q1 GDP contracted slightly more than market forecasts. Q/Q growth was -0.2% (-0.1% forecast and 0.6% prior), while in annualized terms we fell -0.7%, against a -0.3% forecast but Q4 revisions were higher to +2.4%. This is the first GDP q/q growth contraction since Q1 2024. It comes ahead of likely trade disruptions from US tariffs, while trade negotiations continue. The softer aggregate growth backdrop underscores recent downward revisions to the BoJ growth forecasts, which suggests little prospects of further policy rate hikes in the near term.

- In terms of the detail, private consumption spending was flat, against a 0.1%q/q forecast. Q4's outcome was revised up to a 0.1% gain (originally reported as a flat outcome).

- Business spending was a bright spot, up 1.4%q/q, versus 0.6% forecast, while Q4 was revised higher to +0.8%.

- Net exports dragged more than forecast at -0.8%, while net inventories were positive at 0.3%, close to expectations.

- In nominal terms GDP rose 0.8%q/q, in line with forecasts. The y/y deflator was 3.3%, slightly above forecasts.

- For the BoJ/authorities, the rise in business spending will be encouraging but the flat consumption result will be a watch point. The policy aims remains for better spending outcomes boosted by positive real wages.

Fig 1: Japan GDP - Consumption (White Line) & Business Spending (Orange Line) Q/Q - Diverging Trends

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Richer But Off Bests, RBA Policy Decision On Tues

ACGBs (YM +3.0 & XM +5.5) are stronger but off the Sydney session's bests on a local data light session.

- Cash US tsys are dealing flat to 2bps richer in today's Asia-Pac session after yesterday's solid rally. Friday's US data: Housing Starts, Building Permits, Import/Export Prices, U. of Mich. Sentiment and TIC Flow data.

- Cash ACGBs are 4-6bps richer with the AU-US 10-year yield differential at +5bps.

- The bills strip has bull-flattened, with pricing flat to +3.

- Interest rate expectations across the $-bloc firmed through December 2025 over the past week, led by Australia (+23bps). Broadly speaking, markets have been content to consolidate recent hawkish repricing, which has largely stemmed from a reduction in downside risks, particularly surrounding trade policy, as headlines around potential deals gained traction.

- RBA-dated OIS pricing is slightly mixed across meetings today. A 25bp rate cut in May is given a 94% probability, with a cumulative 77bps of easing priced by year-end.

- The local calendar will be empty until next Tuesday’s RBA Policy Decision.

- Next week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$800mn of the 2.75% 21 November 2028 bond on Friday.

BONDS: NZGBS: Bull-Flattener After Higher Inflationary Expectations

NZGBs closed showing a bull-flattener, with benchmark yields flat to 4bps lower despite a rise in the RBNZ’s measure of inflationary expectations.

- 2-year inflation expectations rose to 2.29% in Q2, highest since Q2 2024, from 2.06% in Q1. 1-year inflation expectation rises to 2.41% from 2.15%, also the highest since Q2 2024.

- “On average, respondents see the official cash rate declining to 3.2% by the end of the June quarter from the current 3.5%. The rate is expected to fall further to 2.91% by the end of the March 2026 quarter, according to the RBNZ.” (per MTN)

- NZGBs held by foreigners fell to 61.6% in April from 61.9% in March.

- Cash US tsys are dealing flat to 2bps richer in today’s Asia-Pac session after yesterday’s solid rally. Friday's US data: Housing Starts, Building Permits, Import/Export Prices at 0830ET; U. of Mich. Sentiment at 1000ET followed by TIC Flow data at 1600ET.

- Swap rates closed showing a twist-flattener, with leads 1bp higher to 4bps lower.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for May, with a cumulative 68bps by November 2025.

- On Monday, the local calendar will see Performance Services Index and PPI Input/Output data.

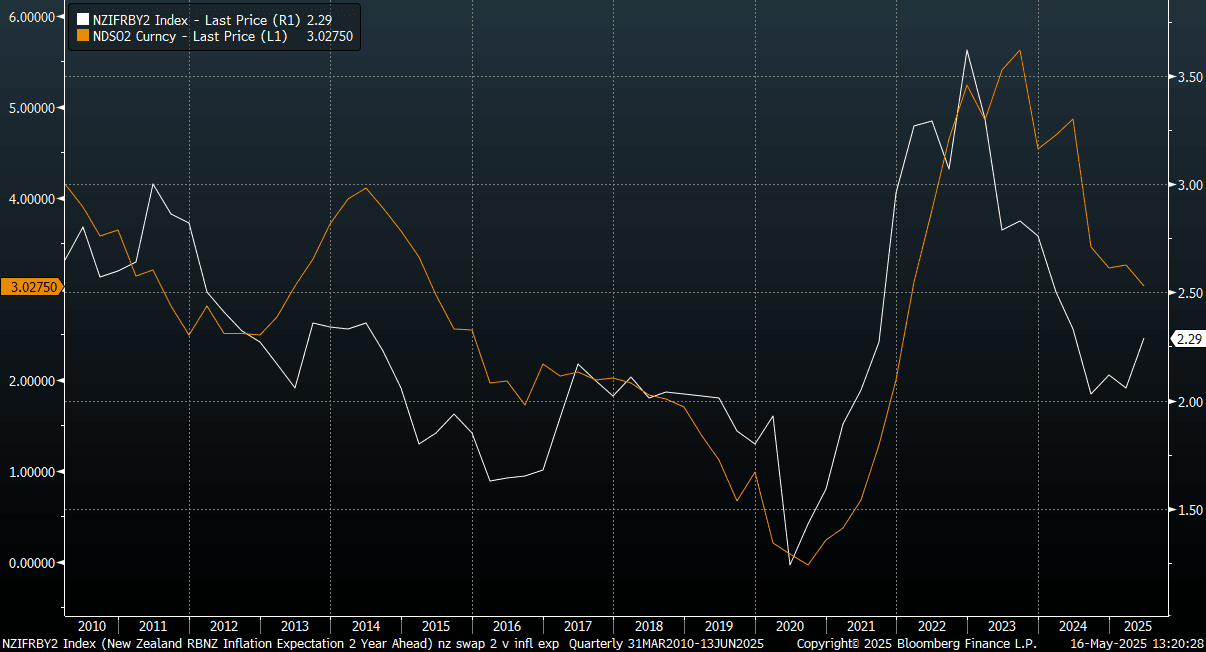

NEW ZEALAND: Inflation Expectations Rise In Q2, Up From Mid-Point Of RBNZ Band

New Zealand's inflation expectations edged up in Q2, per the RBNZ survey. The 2yr ahead expectations rose to 2.29%, from 2.06% in Q1. Expectations had been near 2.0% (the mid point of the RBNZ band) since Q3 last year. We are still well off late 2022 cycle highs of 3.62%, but at face value this isn't a welcome development from an RBNZ standpoint, as it waits to see greater economic traction from its easing efforts.

- 1yr inflation expectations also pushed higher from 2.41%, versus 2.15% in Q1. 5 yr and 10yr inflation expectations edged slightly higher and remain above 2%.

- The chart below plots 2yr RBNZ inflation expectations against the 2yr swap rate. The broader trends in both series line up well with each other. The 2yr swap rate has struggled to see much downside traction in recent months sub 3.00%.

- NZD/USD has edged higher push the print, but is yet to regain the 0.5900 handle (last 0.5895/00, +0.35% for the session)

Fig 1: 2yr Ahead Inflation Expectations & NZ 2yr Swap Rate

Source: MNI - Market News/RBNZ/Bloomberg

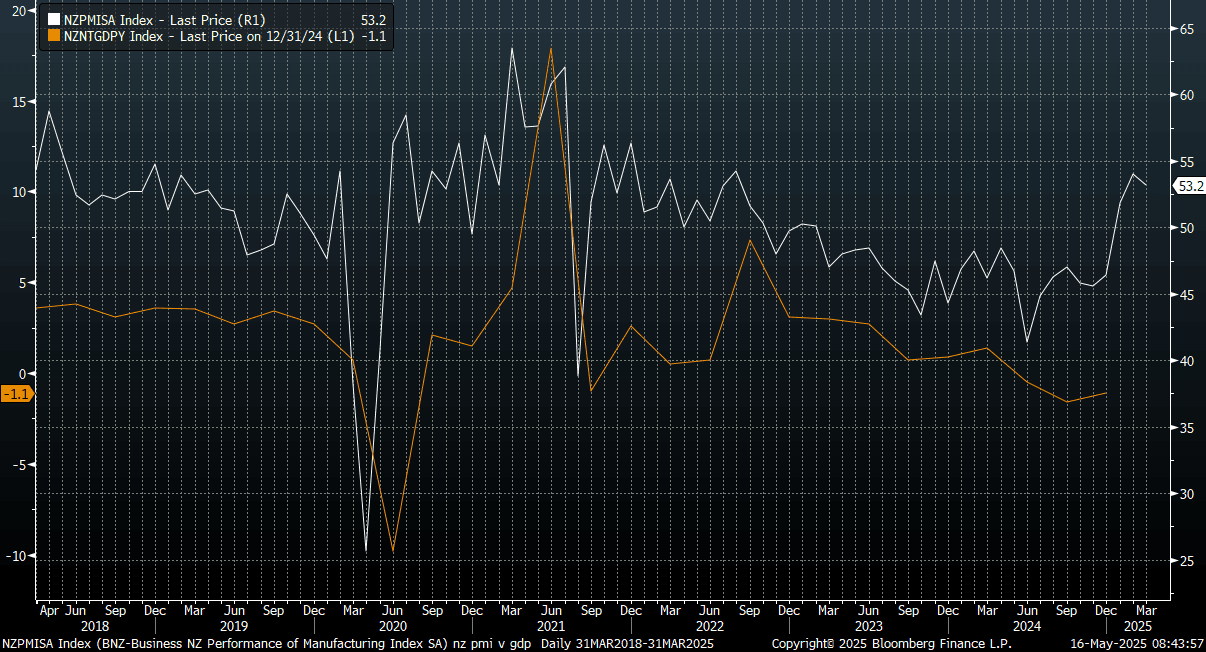

NEW ZEALAND: PMI Edges Higher, Remains Comfortably In Expansion Territory

The BusinessNZ manufacturing PMI rose to 53.9 in April, from 53.2 in March. This is just below recent highs, with 54.1 recorded in Feb. The index is well up from cycle lows seen in 2024 though (41.4). It continues to point to an improved cyclical backdrop for NZ, with hopes that the RBNZ's easing cycle aids a firmer domestic backdrop. This print follows generally softer retail card spending figures from earlier in the week.

- The chart below overlays the PMI versus NZ GDP growth in y/y terms. The headline PMI read is pointing to improved GDP momentum. Note the Q1 GDP report doesn't print until June 19.

- In terms of the detail, BBG noted production easing to 53.8, while employment jumped to 55, which is the highest read since 2021. This will hopefully translate into better employment outcomes, with the Q1 labour force report showing y/y jobs growth still negative at -0.7%.

- New orders edged up to 51.4.

- Note later on we have the Q2 inflation expectations report for NZ.

Fig 1: NZ Manufacturing PMI Versus NZ GDP Y/Y

Source: BusinessNZ/BNZ/MNI - Market News/Bloomberg

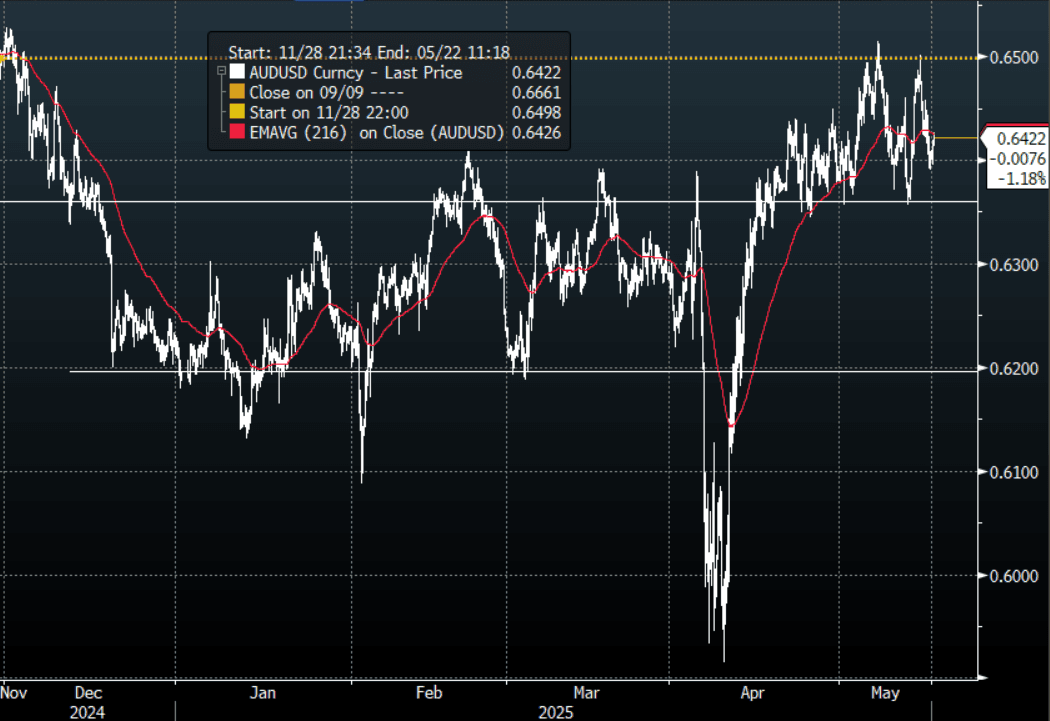

FOREX: AUD Wrap - AUD Sees Demand In Asia

The AUD/USD had a range of 0.6395 - 0.6426 in the Asia- Pac session, it is going into London trading around 0.6420. AUD has found some demand sub 0.6400 in a relatively quiet trading day.

- Western Australian - “Australia’s biggest bank(CBA) believes the battle against inflation has been won, tipping mortgage holders to get back-to-back rate cuts.”

- “Despite national inflation figures coming in hotter than expected and a surge in Aussies employed in April, a Commonwealth Bank economist is “confident” the RBA will cut interest rates in May before leaving the “door ajar” for a second rate cut in July.”

- “We expected the RBA to commence normalising the cash rate in February with a 25bp rate cut, which was delivered, and we also forecast another 25bp rate decrease in May,” CBA head of Australian economics Gareth Aird said in an economic note.”

- The AUD/USD has found decent demand sub 0.6400 today, expect buyers to be around on dips while the support in the AUD holds. A close back below 0.6300/50 would start to challenge the newly formed uptrend.

- MNI FX OPTIONS: Expiries for May16NY cut 1000ET (Source DTCC) : AUD/USD: $0.6420(AUD683.4m), 0.6540(AUD625.4m), 0.6475(AUD603.9m).

AUD/JPY - Today's range 92.75 - 93.36, it is trading currently around 93.35. Decent demand seen first up as price tested below 93.00 this morning. There should be some demand around 92.00/93.00 but a sustained close back below 91.50/92.00 would turn the focus back towards the lows again.

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg

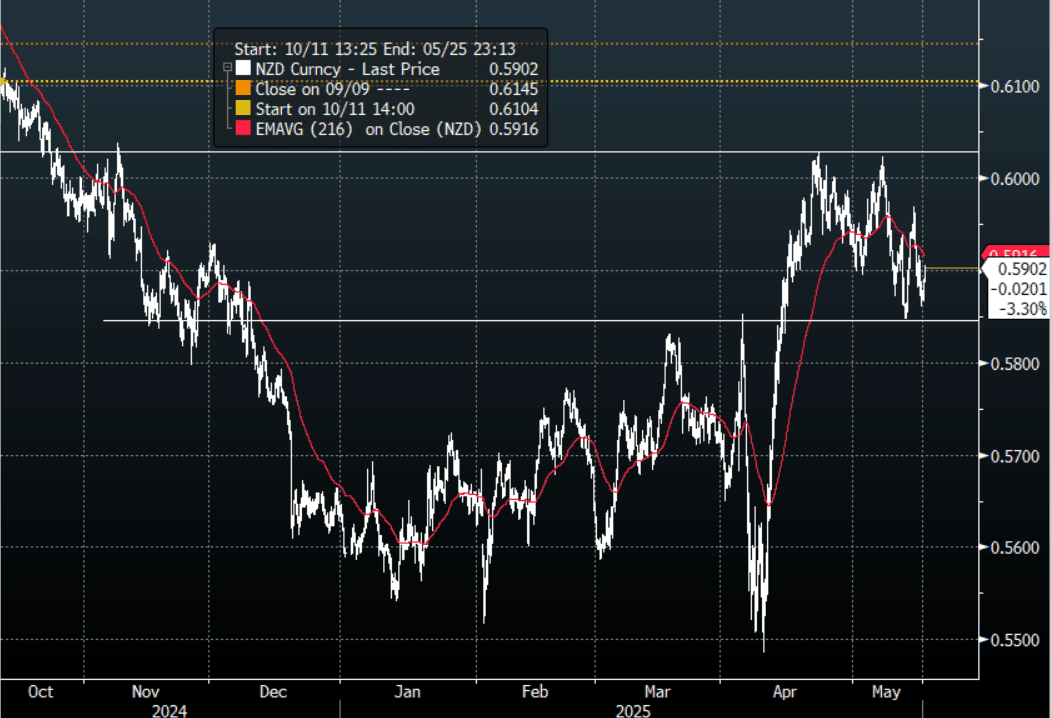

NZD: Bounces On Higher Inflation Data

The NZD/USD had a range of 0.5861 - 0.5905 in the Asia-Pac session, going into the London open around 0.5902. The NZD has popped higher this morning on inflation expectations rising.

- New Zealand's inflation expectations edged up in Q2, per the RBNZ survey. The 2yr ahead expectations rose to 2.29%, from 2.06% in Q1. Expectations had been near 2.0% (the mid point of the RBNZ band) since Q3 last year. We are still well off late 2022 cycle highs of 3.62%, but at face value this isn't a welcome development from an RBNZ standpoint, as it waits to see greater economic traction from its easing efforts.

- The NZD now seems to be comfortable in a 0.5800/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break above here is needed to regain momentum.

- MNI FX OPTIONS: Expiries for May16 NY cut 1000ET (Source DTCC): NZD/USD: 0.5875(NZD446m), Notable upcoming strikes: 0.5915(NZD1.05bln May 19), 0.5875(NZD349.6m May 21)

AUD/NZD has turned lower today after stalling just above 1.0900, with the inflation data giving it the push it needed to top out. Support should now be seen back towards 1.0800 again.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

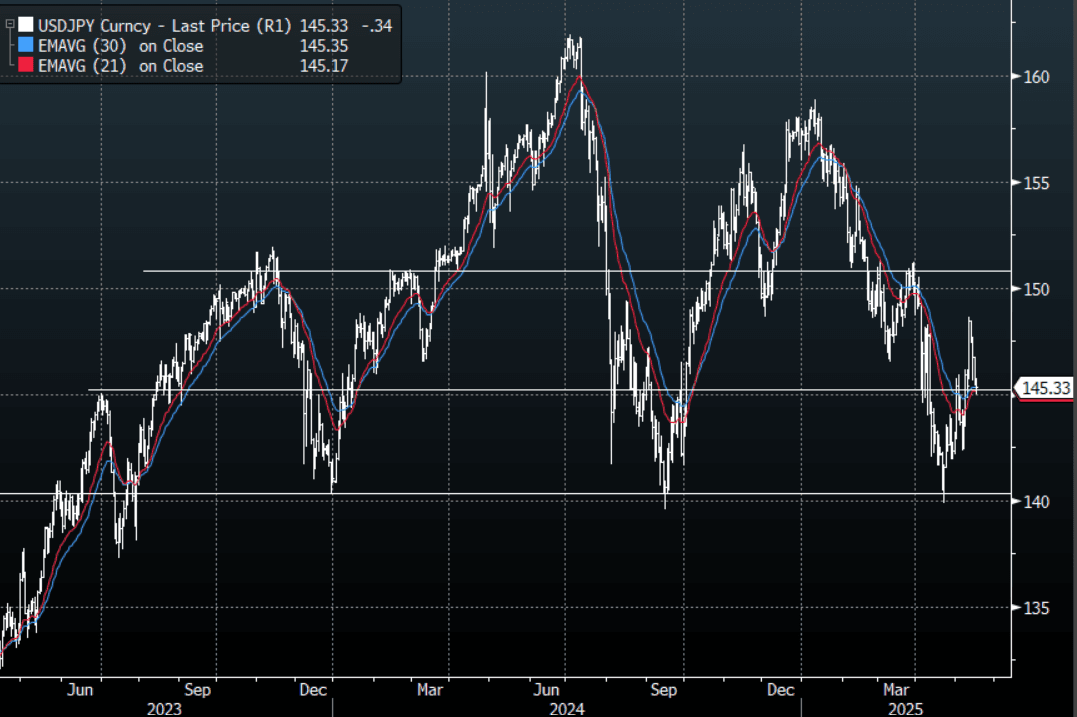

JPY Wrap - GDP Sees A Test Of 145.00

The Asia- Pac range has been 144.97 - 145.72, Asia is currently trading around 145.35. USD/JPY has extended lower for most of our session on the back of some poor data before finding some buyers back towards the pivotal 145.00 area.

- Dow Jones via BBG – “Japan's economy shrank in the first quarter of 2025 for the first time in a year, and faces a bumpy road ahead due to the impact of U.S. trade policy.”

- “Japan's real gross domestic product decreased 0.2% in the January-March period from the previous quarter, preliminary government data showed Friday, putting the risk of a technical recession in play.”

- "It is likely inevitable that exports and domestic production will be significantly pushed down in the April-June quarter due to higher U.S. tariffs," Taro Saito, an economist at NLI Research Institute, said in a research note published ahead of Friday's release.

- “He expects the economy to contract again in the second quarter due to weakening exports and sluggish domestic demand.”

- "JAPAN AKAZAWA: GOVT HAS NO PLAN NOW TO COMPILE FRESH STIMULUS PACKAGE BUT WILL COORDINATE APPROPRIATELY WITH RULING COALITION - [RTRS]"

- *KATO: ALSO CONFIRMED WITH US FX SHOULD BE DETERMINED BY MARKET, PLANS TO TALK WITH BESSENT ON FX IN LINE WITH AGREEMENT" - BBG

- USD/JPY is consolidating after a powerful break higher, support is now around 145.00. Stocks had a positive close but it seems USD/JPY is taking its cues from US yields which have backed off from some pretty pivotal levels.

- The support around 144/145 looks important now, the price action though does not look great and the market is still more comfortable selling rallies.

MNI FX OPTIONS: Expiries for May16 NY cut 1000ET (Source DTCC)USD/JPY: Y147.75($1.09bln), Y146.85($778.9bln), Y145.00($735.4bln)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

FOREX: FX Wrap - USD Trades A Little Soft

The BBDXY has had a range of 1227.96 - 1229.83 in the Asia-Pac session, it is currently trading around 1228. The EU is revising its proposals for a potential trade deal with the US, people familiar said. The bloc’s economy chief urged China to avoid flooding Europe with its goods as it seeks to avoid US tariffs, with data showing Beijing’s trade surplus with the EU hit a record in the first four months of this year(BBG). CNBC - “Brace for wild trading on Friday as a huge wave of options is set to expire”.

- EUR/USD - Asian range 1.1182 - 1.1209, Asia is currently trading 1.1205. EUR/USD has had a quiet session as the market consolidates. The market is still expected to use dips as a buying opportunity and dips back towards 1.09/1.10 should see buyers remerge.

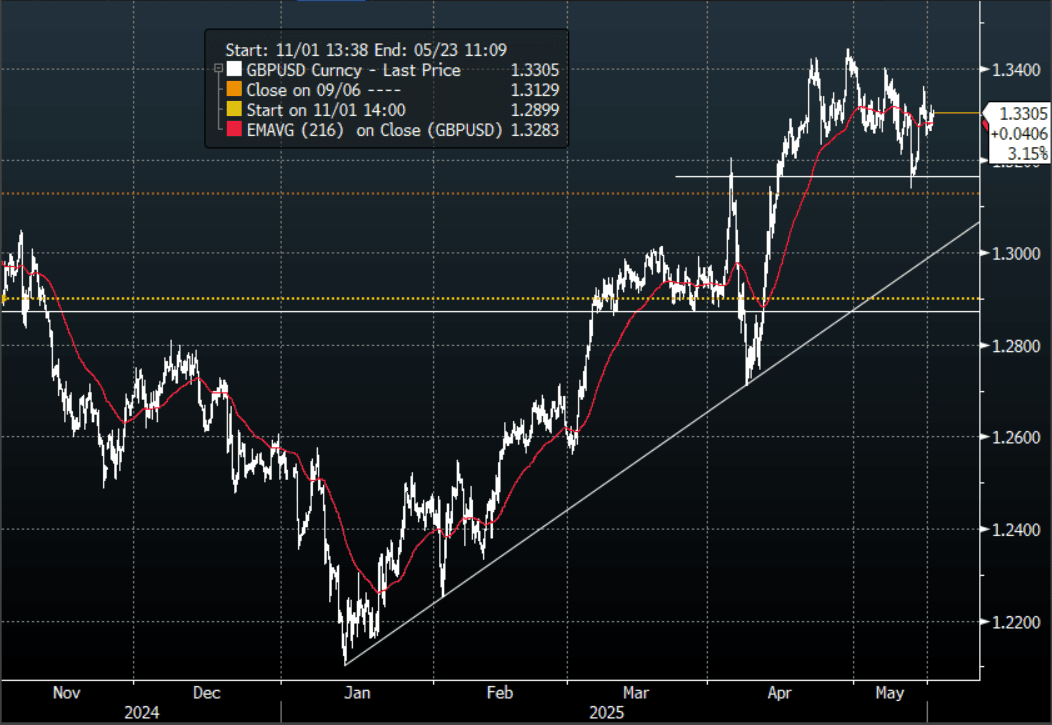

- GBP/USD - Asian range 1.3299 - 1.3319, Asia is currently dealing around 1.3320. Decent demand for GBP sub 1.3200 has seen it bounce back to the middle of its recent range 1.3150 - 1.3450.

- USD/CNH - Asian range 7.1952 - 7.2063, the USD/CNY fix printed 7.1938. Asia is currently dealing around 7.2000. Sellers should be found on a bounce back towards 7.24/25 again.

- Cross asset : SPX +0.01%, Gold $3215, US 10-Year 4.42%, BBDXY 1228, Crude oil $61.76

Data/Events : US Business Inventories, NAHB Housing Index, Housing Starts, Un of Mich sentiment, Italy CPI & Trade Balance, EC Trade Balance

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

Asia Stocks Mixed as Trade Truce Euphoria Fades

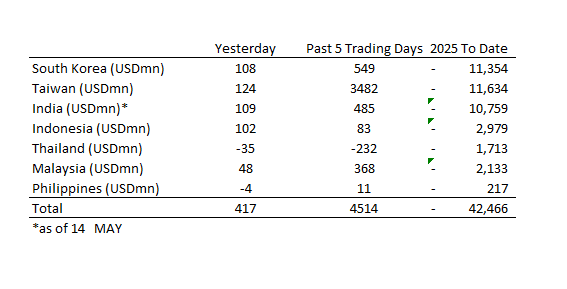

Asia stocks are mixed today as the impetus given from the news of the trade truce fades away and a focus on fundamentals reasserts. High expectations for Alibaba’s results were not met as the Chinese tech giant’s results were seen as largely underwhelming. The Asia region has experienced strong inflows led by Taiwan as flows over the last five trading days reach USD$4.5bn.

- China’s bourses were mostly down with the Hang Seng lower by -0.81%, yet remain over +1.5% higher for the week. The CSI 300 is down -0.57% today and holding onto a 1% gain for the week. Shanghai is down -0.52% yet remains up +0.65% for the week whilst Shenzhen is up today by +0.35% and up +0.95% for the week.

- Taiwan’s TAIEX has had an incredible week of inflows and is up +0.20% today and over 4% for the week.

- The KOSPI is higher by +0.30% and set to deliver a 2% increase this week.

- The FTSE Malaysia KLCI fell modestly today by -0.11% and is up +1.8% for the week.

- The Jakarta Composite has delivered another strong week of gains rising +0.30% today and almost 2% for the week.

- Singapore’s FTSE Straits Times fell modestly today but remains +0.95% higher for the week whilst the PSEi in the Philippines fell again today to erase gains at the beginning of the week. It remains just +0.3% higher on the week.

- The NIFTY 50 fell today by a modest -0.25% but has delivered a very strong week with gains over 4%

ASIA STOCKS: Strong Flows into the End of the Week for Asian Stocks

Equity flows have been very strong throughout the week led by Taiwan as flows over the last five trading days reach USD$4.5bn

- South Korea: Recorded inflows of +$108m as of yesterday, bringing the 5-day total to +$549m. 2025 to date flows are -$11,354m. The 5-day average is +$110m, the 20-day average is +$16m and the 100-day average of -$129m.

- Taiwan: Had inflows of +$124m as of yesterday, with total inflows of +$3,482m over the past 5 days. YTD flows are negative at -$11,634. The 5-day average is +$696m, the 20-day average of +$371m and the 100-day average of -$134m.

- India: Had inflows of +$109m as of the 14th, with total inflows of +$485m over the past 5 days. YTD flows are negative -$10,759m. The 5-day average is +$97m, the 20-day average of +$286m and the 100-day average of -$126m.

- Indonesia: Had inflows of +$102m as of yesterday, with total inflows of +$83m over the prior five days. YTD flows are negative -$2,979m. The 5-day average is +$17m, the 20-day average -$40m and the 100-day average -$32m

- Thailand: Recorded outflows of -$35m as of yesterday, outflows totaling -$232m over the past 5 days. YTD flows are negative at -$1,713m. The 5-day average is -$46m, the 20-day average of -$18m the 100-day average of -$18m.

- Malaysia: Recorded inflows of +$48m as of yesterday, totaling +$368m over the past 5 days. YTD flows are negative at -$2,133m. The 5-day average is +$74m, the 20-day average of +$35m and the 100-day average of -$24m.

- Philippines: Saw outflows of -$4m as of yesterday, with net inflows of +$11m over the past 5 days. YTD flows are negative at -$217m. The 5-day average is +$2m, the 20-day average of +$4m the 100-day average of -$3m.

Oil Claws Back Some Overnight Falls

- Oil had a small bounce in Asia trading after heavy falls in the US session overnight.

- WTI is up marginally by +0.10% at US$61.75 bbl, and is on track to deliver over 1% of gains for the week.

- Brent is up +0.09% at $64.66 and also up over 1% for the week.

- Overnight President Trump said that the US and Iran a edging closer to a deal regarding Tehran's nuclear program and such a deal could potentially see Iran re-enter global oil markets and hence increase supply by 200,000 to 300,000 barrels a day, increasing the likelihood of a significant oversupply later this year.

- Average US oil exports dropped 10% to 3.76 million barrels a day in the four weeks through May 9, the slowest pace since January. The drop in exports is attributed to a combination of factors, including the global trade war, reduced refinery capacity, and cheap Middle Eastern barrels flowing into the market.

- Tumbling oil prices are set to boost consumption, the International Energy Agency said in its monthly market report. Retail prices for gasoline and gasoil have already declined to multiyear lows in most countries. "More to come once April's price rout is passed through to pump prices"

Gold Gives Back Overnight Gains

- The gold market leapt on weaker than expected PPI for April overnight but couldn’t hold those gains in the Asia trading day preferring to focus on the language from the Fed that seemingly points to a period of being on hold rather than an urgent need to cut.

- Gold is down -0.80% today at US$3,214.15

- For the week Gold remains lower by more than 3%, its largest weekly fall for the year.

- Gold sits at the mid-point between the 20-day EMA of $3,260.68 and the 50-day EMA of $3,169.76

Malaysia GDP 1QF In Line with 4Q

- Malaysia’s GDP YoY for the first quarter came in line with the 4Q of 2024 at +4.4%.

- Market forecasts had been for a minor increase due to front loading of exports due to tariffs.

- The seasonally adjusted QoQ result was much better than expected at +0.7%, from -0.2% prior.

- The BNM now sees GDP growth lower than their current +4.5%-5.5% forecast with growth ably supported by consumer demand and investment. The balance of risks to the growth outlook is currently tilted to the downside,” Bank Negara Malaysia Governor Abdul Rasheed Ghaffour said at a briefing on Friday. “We are in a position of strength and we have the policy instrument and policy space to act, if we need to.”

- The BNM expects inflation to remain moderate and is likely to reset their annual forecast.

- The BNM meets next on July 09 and currently there is just 8bps of cuts priced into the bond market.

ASIA FX: USD/KRW Dips Eyeing Recent Lows, CNH & TWD Respecting Recent Ranges

In North East Asia FX, the USD is weaker, but recent ranges are being respected for now. Equity markets have struggled for upside, although Taiwan and South Korean markets have been supported on dips. Won is outperforming both TWD and CNH.

- Spot USD/KRW remains biased to the downside, the pair getting to session lows of 1391.10. A clean break under 1390 could see earlier May lows just under 1382 targeted. Focus remains on scope for US-South Korea FX policy discussions. US Trade Representative Geer has been in South Korea in the past few days, where discussions have taken place on the sidelines of the APEC meetings. The return of some offshore investors flows has also likely aided the won, now up to $689.5mn for this week.

- USD/CNH has continued to track very tight ranges. We were last near 7.2000. The USD/CNY fix was lowered, but didn't have a lasting impact on sentiment. Onshore USD/CNY spot also tracks close to the 7.2000 level. On Monday we get the April activity prints, along with April home price figures.

Spot USD/TWD sits slightly up from session lows, the pair last in the 30.10/15 region. We remain above 30.00 for now. Taiwan officials again denied the US trade discussions have involved FX. The Taiex is struggling for fresh upside, although equally pullbacks remain fairly shallow at this stage.

- South Korea’s import prices fell 2.3% in April from a year ago, while export prices increased 0.7%, according to the statement from Bank of Korea. Price for imported goods to South Korea fell for the third straight month due to cheaper crude oil. The import price index declined 1.9 percent in April from a month earlier, after going down 1.0 percent in February and 0.4 percent in March, according to the Bank of Korea (BOK). The successive slide was attributed to cheaper crude oil and the local currency's appreciation versus the U.S. dollar. (source BBG)

- The government on Friday vowed to closely monitor the financial market amid lingering uncertainties stemming from ongoing talks with the United States over its tariff scheme and global economic conditions. Such remarks were made during a meeting on macroeconomic issues, presided over by acting Finance Minister Kim Beom-suk and attended by Bank of Korea (BOK) Gov. Rhee Chang-yong, along with the heads of the Financial Services Commission and the Financial Supervisory Service, according to the Ministry of Economy and Finance. (source Yonhap)

- The KOSPI is higher by +0.30% and set to deliver a 2% increase this week.

- The won gained +.35% today and is up +.37% for the week ag 1,392.90

- Bonds rallied today across the curve with the KTB 10YR lower by -2bps, whilst +3bps for the week.

CHINA: Country Wrap: Investors Believe in China’s Tech Sector - Beijing has pushed back against a US decision aimed at curbing Chinese-made artificial intelligence chips, a first sign of discord between the world’s two largest economies since they agreed to a trade truce last weekend. In a reminder of the tensions that continue to exist between the Trump administration and China when it comes to technology, the Commerce Department said earlier this week it would issue guidance to make clear that using Huawei Technologies Co.’s Ascend AI chips “anywhere in the world violates US export controls.” (source BBG)

- Almost half of investors surveyed by Cheung Kong Graduate School of Business believe that the trade tensions between China and the United States will present more opportunities than challenges to the Chinese technology sector. Forty-six percent of respondents think the tariff war will have more positive than negative effects on the Chinese tech sector in the long run, according to the findings of the Investor Sentiment Questionnaire Survey (CKISS). Twenty-eight percent anticipate long-term negative impacts, and around 20 percent expect no significant long-term impacts. (source Yicai)

- China's bourses were mostly down with the Hang Seng lower by -0.81%, yet remain over +1.5% higher for the week. The CSI 300 is down -0.57% today and holding onto a 1% gain for the week. Shanghai is down -0.52% yet remains up +0.65% for the week whilst Shenzhen is up today by +0.35% and up +0.95% for the week.

- Taiwan's TAIEX has had an incredible week of inflows and is up +0.20% today and over 4% for the week.

- Yuan Reference Rate at 7.1938 Per USD; Estimate 7.2118

- China’s bonds have moved higher in yield over the week with the CGB 10YR +5bps higher at 1.67%

- INDIA: Country Wrap: Trade Deficit at Five Month High

- India is reviewing a US request to lift restrictions on ethanol imports as it negotiates a wider trade deal with Washington to avoid punitive tariffs. US negotiators want the South Asian country to allow shipments of the biofuel for blending with gasoline, according to people familiar with the matter, a change from current rules that promote domestic supply and permit overseas purchases of ethanol only for non-fuel use. (source BBG)

- India’s trade deficit widened to a five-month high in April, as the nation’s import bill rose due to a pick up in domestic demand, exceeding the growth in outbound shipments. The gap between exports and imports stood at $26.42 billion last month, trade data showed Thursday. That was higher than the $20.5 billion deficit forecast by economists in a Bloomberg survey. The trade deficit had widened to $21.5 billion in March. Inbound shipments rose 19.1% in April to $64.91 billion from a year earlier, while outbound shipments grew 9% to $38.49 billion, the data showed. The pick up in imports comes amid signs of consumption gaining pace following measures by the government and the central bank to boost demand. (source BBG)

- The NIFTY 50 fell today by a modest -0.25% but has delivered a very strong week with gains over 4%

- The rupee is down modestly today and one of the worst regional performers for the week, down -0.30% at 85.63.

- Bonds are modestly lower in yield today and down strongly over the week following RBI purchases. The IGB 10YR is -10bps for the week at 6.26%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 16/05/2025 | 0730/0930 | ECB's Cipollone At EU Cyber Resilience Board Meeting | ||

| 16/05/2025 | 0800/1000 | *** | HICP (f) | |

| 16/05/2025 | 0900/1100 | * | Trade Balance | |

| 16/05/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/05/2025 | 1230/0830 | New York Fed's Roberto Perli | ||

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 16/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 16/05/2025 | 1500/1700 | ECB's Lane On Central Bank Communication Panel | ||

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 2000/1600 | ** | TICS | |

| 16/05/2025 | 0140/2140 | San Francisco Fed's Mary Daly |