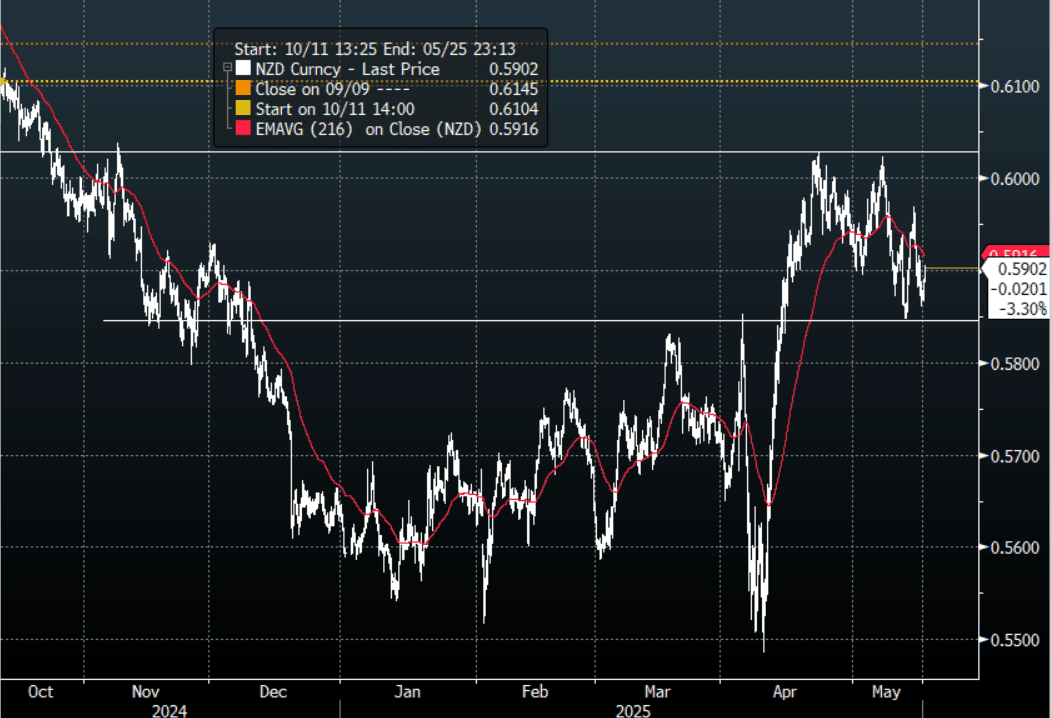

NZD: Bounces On Higher Inflation Data

The NZD/USD had a range of 0.5861 - 0.5905 in the Asia-Pac session, going into the London open around 0.5902. The NZD has popped higher this morning on inflation expectations rising.

- New Zealand's inflation expectations edged up in Q2, per the RBNZ survey. The 2yr ahead expectations rose to 2.29%, from 2.06% in Q1. Expectations had been near 2.0% (the mid point of the RBNZ band) since Q3 last year. We are still well off late 2022 cycle highs of 3.62%, but at face value this isn't a welcome development from an RBNZ standpoint, as it waits to see greater economic traction from its easing efforts.

- The NZD now seems to be comfortable in a 0.5800/0.6050 range and awaits a catalyst to provide the impetus to break-out.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break above here is needed to regain momentum.

- MNI FX OPTIONS: Expiries for May16 NY cut 1000ET (Source DTCC): NZD/USD: 0.5875(NZD446m), Notable upcoming strikes: 0.5915(NZD1.05bln May 19), 0.5875(NZD349.6m May 21)

AUD/NZD has turned lower today after stalling just above 1.0900, with the inflation data giving it the push it needed to top out. Support should now be seen back towards 1.0800 again.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Quiet Session

TYM5 traded in a narrow 110-30+ to 111-04 range during the Asia-Pacific session, heading into the London open. It last changed hands at 111-01, down 0.01 from the previous close.

- The US 10-year yield has consolidated in a tight range of 4.3117 - 4.3369% in Asia, dealing around 4.33% as we head into the London open.

- US yields continued to benefit from comments made overnight by Deputy Treasury Secretary Michael Faulkner who said officials are discussing a move to loosen bank regulations and allow lenders to keep more Treasuries on their balance sheets.

- The market is keenly awaiting Fed Chair Jerome Powell’s speech later today discussing the economic outlook.

- Dips back towards 4.25/30% should now find supply, as the market consolidates heading into a long weekend.

- Today's Data: Retail Sales, Industrial Production, Capacity Utilization, NAHB Housing Market Index.

JGBS: Cash Bond Bull-Flattener Holding At Lunch Break

At the Tokyo lunch break, JGB futures are stronger, +44 compared to settlement levels, hovering just below session highs.

- Cash US tsys are 1bp cheaper to 3bps richer, with a steepening bias, in today's Asia-Pac session after yesterday's modest gains.

- BoJ Governor Ueda has commented to local newspaper Sankei, noting the central bank will have to monitor the tariff impact and may need to respond if the economy is impacted. (per RTRS)

- The next BoJ policy meeting is at the start of May. Market expectations for rate hikes have been sharply scaled back over the past month in response to President Trump's announcement of reciprocal tariffs. Markets now assign a 0% probability to a 25bp hike at the May meeting, with less than a cumulative 50% chance not priced in by December.

- This marks a significant shift from just a month ago when a full hike was priced by October and a 50% probability was expected by June.

- Cash JGBs are 2-7bps richer across benchmarks, with a flattening bias. The benchmark 10-year yield is 3.9bps lower at 1.332% versus the cycle high of 1.596%.

- Swaps have also bull-flattened, with rates 2-8bps lower. Swap spreads are mixed.

AUD: AUDUSD Range Trading, Safe Have Currencies Outperforming

AUDUSD bounced on the generally stronger-than-expected March China activity data but it has reversed those gains to be down 0.1% as China/HK equities sell off. The pair is now at 0.6338 after a low of 0.6323 early in trading following the decline in the S&P. The USD index is 0.2% lower.

- Safe haven currencies are outperforming today leaving AUDJPY down 0.5% to 90.42, after an intraday low of 90.38. AUDEUR is also 0.5% lower at 0.5595, close to today’s low. AUDGBP is down 0.25% to 0.4783.

- Kiwi is also risk sensitive but continues to marginally outperform Aussie. AUDNZD is down 0.2% to 1.0739 after a trough of 1.0738.

- The Westpac leading index for March fell 0.11% m/m leaving the 6-month annualised rate at 0.6% down from 0.9% in February. There are signs that it is being impacted by the effect on markets of recent global developments.

- Equities are generally weaker with the Hang Seng down 2.0%, CSI 300 -0.9% and S&P e-mini down 0.8%, but ASX up 0.3%. Oil prices are lower with WTI -0.3% to $61.12/bbl. Copper is down 0.7% and iron ore tested $97/t.

- Later Fed Chairman Powell speaks to Chicago’s Economic Club, also Hammack and Schmid appear. US March retail sales, IP and April NY Fed services & NAHB housing indices print. UK March CPI, euro area final March CPI and February current account are released. The BoC decision is announced and with expectations for unchanged rates.