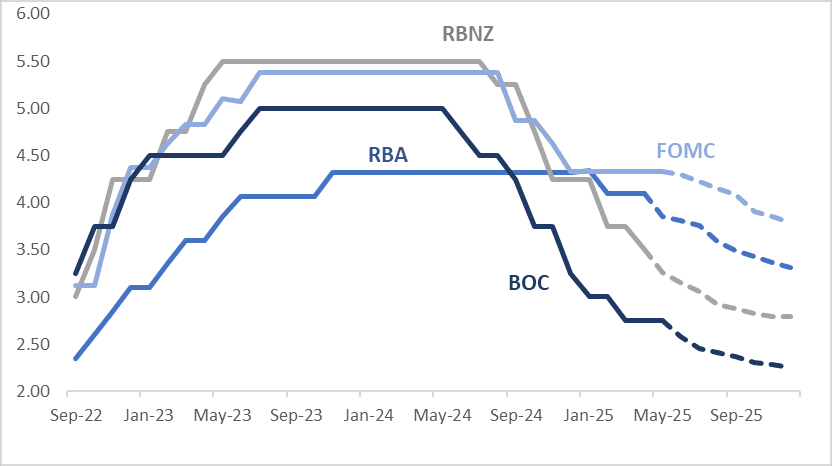

STIR: $-Bloc Markets Firm Over Past Week Led By Australia

Interest rate expectations across dollar-bloc economies have firmed through December 2025 over the past week — with the exception of Canada. Australia saw the most significant shift, with a 23bp rise in expected year-end rates, followed by the US (+16bps) and New Zealand (+6bps). In contrast, Canada’s implied rate softened by 8bps.

- In the US, softer-than-expected retail sales and PPI data yesterday outweighed slightly lower jobless claims, prompting a modest dovish reaction in Fed pricing. Earlier in the week, CPI data came in broadly in line with expectations and had limited impact on market re-pricing.

- In Australia, April employment data surprised to the upside with an 89k increase in jobs, while the unemployment rate held steady at 4.1%. The figures highlight continued labour market tightness, with employment growth keeping pace with labour force expansion. Combined with stronger-than-expected wage data earlier this week, the RBA may reinforce a more cautious stance on future easing. Nonetheless, it is unlikely to derail expectations for a 25bp rate cut at the RBA’s May 20 meeting.

- Across the $-bloc more broadly, markets appear content to consolidate recent hawkish repricing, which has largely stemmed from a reduction in downside risks, particularly surrounding trade policy, as headlines around potential deals gained traction.

- The next key event for the region is the RBA’s May 20 policy meeting, where a 25bp rate cut is currently fully priced in.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.79%, -54bps; Canada (BOC): 2.26%, -49bps; Australia (RBA): 3.31%, -79bps; and New Zealand (RBNZ): 2.79%, -71bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: AUDUSD Range Trading, Safe Have Currencies Outperforming

AUDUSD bounced on the generally stronger-than-expected March China activity data but it has reversed those gains to be down 0.1% as China/HK equities sell off. The pair is now at 0.6338 after a low of 0.6323 early in trading following the decline in the S&P. The USD index is 0.2% lower.

- Safe haven currencies are outperforming today leaving AUDJPY down 0.5% to 90.42, after an intraday low of 90.38. AUDEUR is also 0.5% lower at 0.5595, close to today’s low. AUDGBP is down 0.25% to 0.4783.

- Kiwi is also risk sensitive but continues to marginally outperform Aussie. AUDNZD is down 0.2% to 1.0739 after a trough of 1.0738.

- The Westpac leading index for March fell 0.11% m/m leaving the 6-month annualised rate at 0.6% down from 0.9% in February. There are signs that it is being impacted by the effect on markets of recent global developments.

- Equities are generally weaker with the Hang Seng down 2.0%, CSI 300 -0.9% and S&P e-mini down 0.8%, but ASX up 0.3%. Oil prices are lower with WTI -0.3% to $61.12/bbl. Copper is down 0.7% and iron ore tested $97/t.

- Later Fed Chairman Powell speaks to Chicago’s Economic Club, also Hammack and Schmid appear. US March retail sales, IP and April NY Fed services & NAHB housing indices print. UK March CPI, euro area final March CPI and February current account are released. The BoC decision is announced and with expectations for unchanged rates.

CHINA: Bond Futures Jump on Data Release.

- Bond futures jumped on a better-than-expected 1Q GDP release.

- The 10YR future jumped +0.15 post the release before backing away to be +.11 at 109.08

- The 10YR future remains established above all major moving averages; the nearest the 20-day EMA of 108.51.

- The 2YR future remains modestly higher by +0.01 at 102.55 and remains at the mid-point of the 20-day EMA of 102.53 and the 50-day EMA 102.56.

- Cash markets are strong with the CGB10YR lower by -1.5bps at 1.64%

- The data release today poses no immediate pressure for authorities for monetary policy action, rather providing them with time to assess the impact of the trade war.

JPY: JPY Crosses - Holding Gains, CNH/JPY Tests Lows

JPY crosses are consolidating at or near their recent highs as broader risk appetite market sentiment stabilised somewhat and we approach a long weekend. CNY/JPY continues to be the outlier and is pressing its recent lows. Top trade representative Ryosei Akazawa will be looking for some early results from its US Tariff negotiations. He commented this morning that he is “ Feeling ready for US trade talks, Will negotiate with Japan’s interest in mind “ - BBG

- EUR/JPY - Overnight range 161.30 - 162.80, Asia has bounced off the lows to be dealing around 161.70. EUR/JPY stuck in the middle of its wider 155 - 165 range, looking for a catalyst to challenge this.

- GBP/JPY - Overnight range 188.56 - 189.59, Asia has drifted back to 1.8900. Sellers looking to reengage the market on bounces back towards 190.00

- AUD/JPY - Overnight range 90.60 - 91.40, Asia has drifted lower from the open breaking the overnight lows as US Equity futures come under pressure, currently dealing 90.45. The pair has failed on multiple attempts back towards 92, but expect more consolidation going into a long weekend.

- CNH/JPY - Overnight range 19.4789 - 19.6119, Asia drifted lower and then got another leg after the Yuan Fix. Another fix higher in USD/CNY at 7.2133 continues to point to the PBOC slowly managing the currency lower. CNY/JPY continues to be the outlier and bounces have been limited even in the face of a bounce in risk. The first target looks to be around the 18.70 area.

- There has been little positive follow from the earlier China data outcomes, which on balance were better than forecast, particularly IP and retail sales. Local equities are down, with focus on trade/tariff issues.

Fig 1 : CNH/JPY Weekly Chart

Source: MNI - Market News/Bloomberg