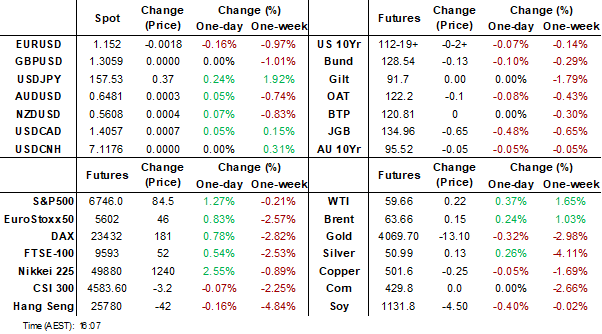

MNI EUROPEAN MARKETS ANALYSIS: Equity Bounce Aids Yen Crosses

- Risk appetite was much firmer in the equity space, after Nvidia results were better than expected. Focus elsewhere was the on the weaker yen and sharp move higher in JGB yields, amid on-going fiscal concerns. We saw further FX comments from Japan officials but they appeared in line with other remarks recently.

- Later the Fed’s Hammack, Barr, Cook, Goolsbee, Miran and Paulson speak as well as BoE’s Mann and Dhingra. US November 15 jobless claims, delayed September payrolls, November Philly & Kansas Fed Indices, October existing home sales and euro area preliminary November consumer confidence print.

MARKETS

US TSYS: Labour Data Tonight Last Chance for Rate Cuts

- The ever diminishing hope for a December rate cut hinges on the labour market data out Thursday in the US.

- Bond futures were lower across maturities with the 10-Yr down -03 to 112.19, remaining at the mid-point between the 50-day EMA of 112-25+ and the 100-day EMA of 112-14+.

Whilst the ultra long end was broadly flat on the day, elsewhere on the curve saw yields higher by up to +1.5bps as rate expectations continue to re-price. Fed meeting expectations re-priced further: Dec'25 at -6bp (-7bps at open), Jan'26 at -20.1bp, Mar'26 at -0.29bps (-30.3bp), Apr'26 at -36.6 (-38.1bp).

- The 2-Yr is up +1.3bps to 3.606%

- The 5-Yr is up +1.1bps to 3.721%

- The 10-Yr is up +0.4bps to 4.143%

- The 30-Yr is flat at 4.75%

Key focus for issuance tonight will be 4-week and 8-week bills and a 10-Yr TIPS auction.

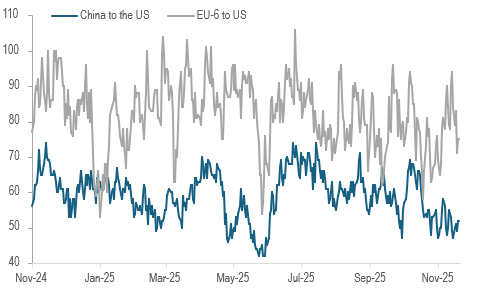

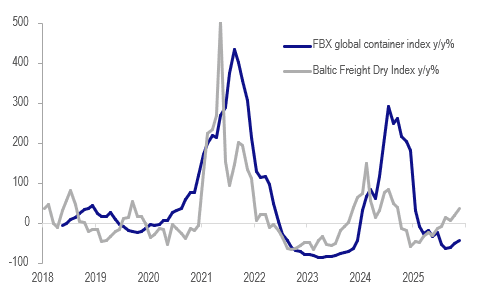

GLOBAL MACRO: Data Point To Robust Global Export Volumes

Shipping companies reported Q3 volumes were strong in line with CPB data showing higher monthly global export volumes in July and August. There had been fears for global trade following the announcement of US reciprocal tariffs in April but it appears to have been more resilient with it up 3.7% y/y in August. After frontloading of shipments to the US in H1, container rates fell from July but have risen sharply in November to date, possibly a sign of continued solid export volumes.

- After rising over H1, departures to the US have normalised over H2 with only those from the EU-6 below the pre-February 2025 average with major Asian shippers all now around their averages, according to Bloomberg’s container ship count.

- Departures from China peaked in July and trended lower thereafter but then took a sharp turn down from mid-October coinciding with the latest US-China trade dispute centred around rare earths. Presidents Trump and Xi met on 31 October and came to an agreement on many issues and as a result ships leaving China for the US tentatively appear to have increased again and are around average.

Bloomberg container ship count

- FBX global container rates fell each month from July but are up 21.3% m/m in November, possibly signalling tighter capacity. They are still down 41.9% y/y but off the 60% y/y decline in September. Rates on the China-East Asia to east coast North America route have also been weak but outperformed the global aggregate and to the Mediterranean.

- There have been reports of tanker shortages pushing up rates for oil and LNG given the current record amount of seaborne crude. Bulk rates are also higher with the Baltic Freight Index up 7.5% m/m in November to be up almost 40% y/y.

Global shipping rates y/y%

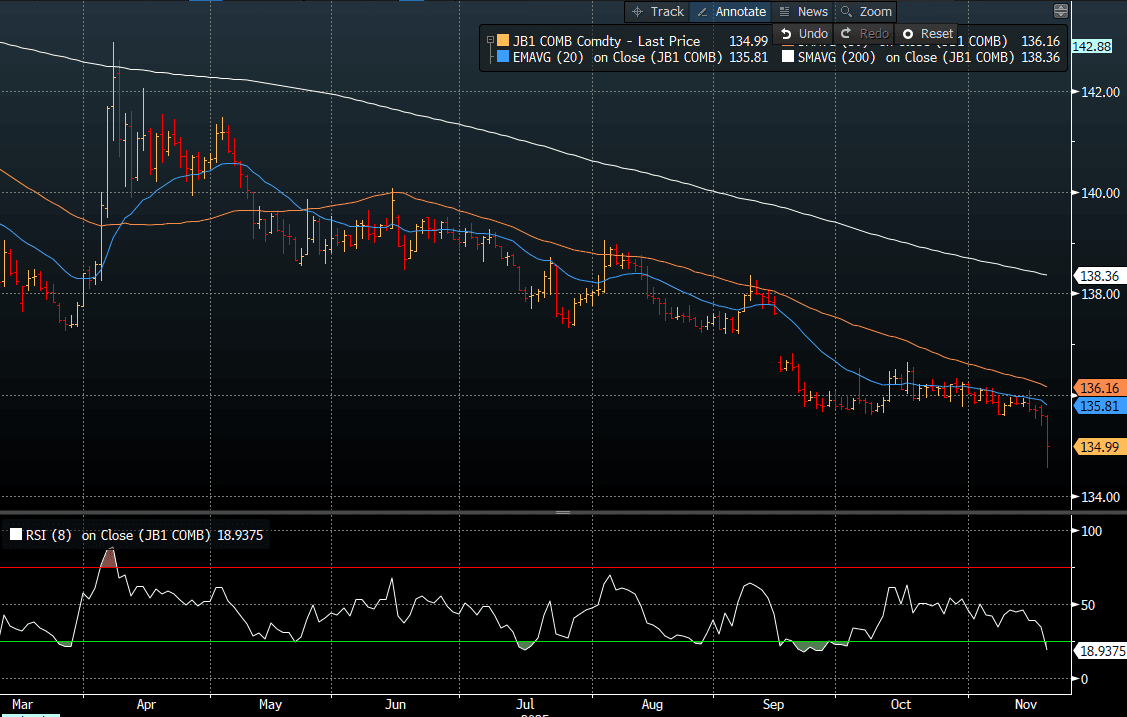

JGBS: Yields Explode Higher As Fiscal Fears Drive Positioning Change

JGB futures are trading sharply weaker at 134.99, -62 compared to settlement levels, albeit well above the session low of 134.56. (see chart)

- MNI’s technical analysts had viewed fresh cycle lows as confirmation of the downtrend that had dominated prices since mid-September. Their Fibonacci projection of 134.69 was hit today.

- “The Japanese government is making final arrangements to compile an economic stimulus package of ~21.3t yen, public broadcaster NHK reports, citing an unidentified person.” - BBG

- "Major investors, including domestic banks, insurers, and overseas accounts, collectively pared net purchases of 10-year JGBs to the lowest since October 2023, according to the latest Japan Securities Dealers Association data. In contrast, demand remained firm for 2- to 5-year notes, while super-long bonds also continued to see modest net buying." – BBG

- BoJ Koeda's speech appeared to be in line with recent rhetoric from key BoJ board members. There were some hawkish undertones, although she didn't give any hints on rate hike timing.

- Cash JGBs are off worst levels but remain 2-7bps cheaper across benchmarks. The 10-year yield is currently at 1.813% versus a session high of 1.845%.

- Tomorrow’s local calendar will see National CPI, Trade Balance and S&P Global PMI(P) data alongside an Enhanced Liquidity Auction for 1-5-year JGBs.

Source: Bloomberg Finance LP

BOJ: Koeda - Gives Upbeat Comments On Inflation But No Hint On Rate Hike Timing

Headlines have crossed from BoJ board member Koeda's speech. At first glance they appear in line with recent rhetoric from key BoJ board members. There were some hawkish undertones, with Koeda noting that the central bank must normalize rates to avoid distortions in the future and that underlying inflation is around 2%. She added that inflation is relatively strong, but via RTRS: "IN ORDER TO ACHIEVE THE PRICE STABILITY TARGET, IT IS IMPORTANT TO EXAMINE THE EXTENT TO WHICH UNDERLYING INFLATION REMAINED STABLE OR BEEN ANCHORED". She also didn't give any hints on rate hike timing (which is hardly surprising ahead of Ueda's speech on Dec 1).

- On growth she reiterated the viewpoints from the Oct meeting around growth risks being skewed to the downside for fiscal 2026, but said the economy wasn't in bad shape.

- Note before Ueda's speech on Dec 1 we also hear from board member Noguchi on Nov 27.

- USD/JPY has crept higher as the headlines from the speech crossed, hitting fresh highs of 157.45/50 (but cross asset trends are supportive of yen losses, with US equity futures trending higher, while Tsy yields are ticking higher).

- JGB futures remain in a downtrend, sitting at 135.10, -.51, at the lunch time break.

JAPAN DATA: Offshore Investors Buy Both Local Stocks & Bonds

The highlights from last week's offshore investment flows, was strong inflows into both Japan stocks and bonds. The offshore buying of local stocks more than offset the prior week's outflow. It adds to the cumulative sum of net inflows going back to the start of Oct, which is now just short of ¥8trln. This week's flow update will be interesting, as local stock indices faltered amid the global tech rout. However, sentiment may end the week better due to Nvidia results lifting broader sentiment in the space.

- We also saw offshore investors buy local bonds for the third straight week. Cumulative inflows into local bonds are also positive since the start of Oct (albeit less so than equities). Focus will be on whether such inflows continue amidst a break higher in some JGB yields (amid fiscal spending concerns from the new government).

- In terms of Japan outbound flows, we saw Japan investors buy offshore bonds for the second straight week, but not enough to offset earlier net selling since the start of Oct. Local investors also bought offshore equities last week, but again this wasn't enough to offset recent net selling pressures.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending Nov 14 | Prior Week |

| Foreign Buying Japan Stocks | 1020.9 | -346.6 |

| Foreign Buying Japan Bonds | 961.6 | 101.5 |

| Japan Buying Foreign Bonds | 348.4 | 566.5 |

| Japan Buying Foreign Stocks | 183.3 | -424.2 |

Source: Bloomberg Finance L.P./MNI

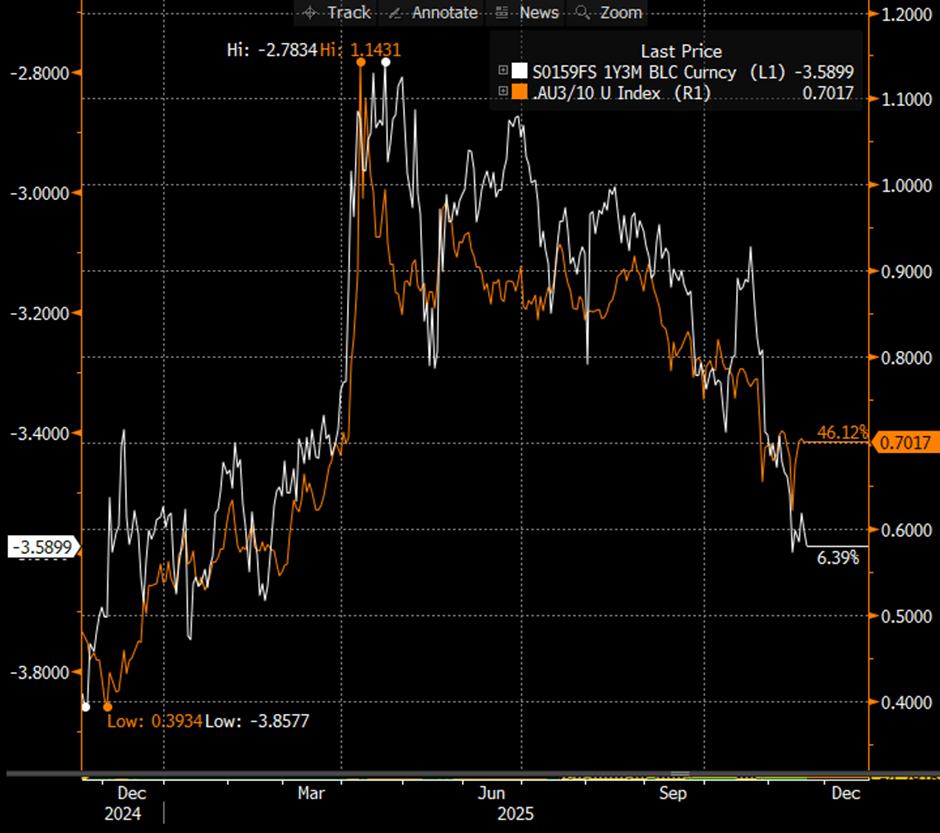

AUSSIE BONDS: Trading Heavy As RBA Research Suggests Prolonged Pause

ACGBs (YM -5.0 & XM -5.0) are weaker and at/near session lows.

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session as the market continues to digest yesterday's release of the FOMC Minutes.

- Cash ACGBs are 5bps cheaper, with the AU-US 10-year yield differential at +33bps.

- Unlike its New Zealand counterpart, which has recently steepened to its highest level since 2021, the ACGB yield curve remains near its flattest point since April, albeit slightly steeper than its recent low. Moreover, the AU 3s10s yield curve appears vulnerable to any upward revision in year-ahead cash rate expectations (see chart).

- Assistant Governor Hunter spoke today on RBA research in areas where the transmission of monetary policy may have changed. The research appears to reflect that the economy has been stronger than the RBA expected, including inflation. This may be another indication that its current pause could be prolonged.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 10bps of easing priced by mid-2026.

- The bills strip is -4 to -7 beyond the 1st contract (-1).

- Tomorrow, the local calendar will see S&P Global PMIs (P).

- The AOFM plans to sell A$700mn of the 1.25% 21 May 2032 bond on Friday.

Bloomberg Finance LP

RBA Researching Why Inflation & Housing Stronger Than It Expected

Assistant Governor (Economic) Hunter spoke today on RBA research in areas where the transmission of monetary policy may have changed. She said it is looking at if businesses have changed price-setting after Covid, how to estimate capacity and full employment, and if monetary policy transmission channels have changed, given the larger than expected housing response to 2025’s 75bp of easing. The research appears to reflect where the economy has been stronger than the RBA expected, including inflation. This may be another indication that its current pause could be prolonged.

- Q3 CPI printed above the RBA’s August forecasts and Hunter reiterated that the bank was “materially surprised by the latest data” but won’t respond to one month’s outcome. So, it is looking at whether businesses are now faster to pass on cost increases and how their margins change with activity.

- Research is particularly focussed on measuring labour market capacity and Hunter said “we think the labour market is currently a bit tight”, which is not sustainable with the inflation target. This could be a reason for the pickup in core CPI. The October unemployment rate returned to 4.3%.

- They are also looking at the uptrend in women and older people joining the labour force, if people are working less now inflation is lower and if there’s a skills mismatch.

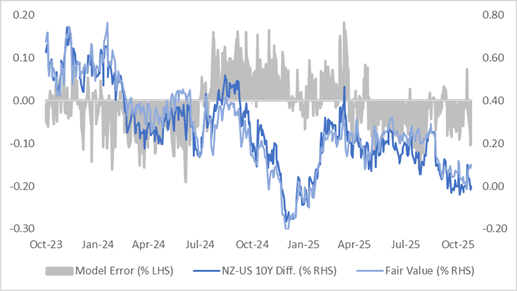

BONDS: NZGBS: Bear-Steepener, NZ-US 10Y Diff Looks Too Low

NZGBs closed showing a bear-steepener, with benchmark yields flat to 4bps higher.

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session as the market continues to digest yesterday’s release of the FOMC Minutes for the October meeting.

- The NZ-US 10-year yield differential finished 2bps wider at flat. A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past three years suggests the current differential is about 10bps below its estimated fair value of +10bps. The regression’s standard error has been ±15bps over the past two years, highlighting the inherent variability in the relationship. Even so, the 1Y3M spread continues to anchor market expectations around the longer-term path of yield convergence. (see chart)

- Swap rates closed 2-5bps higher, with implied swap spreads wider.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for November, with a cumulative 34bps by February 2026.

- Tomorrow, the local calendar will see Trade Balance data.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

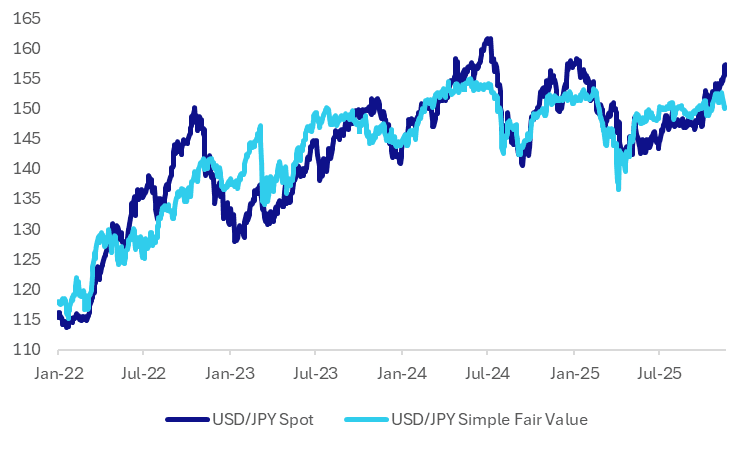

JPY: USD/JPY High Relative To Simple Fair Value, But Short Of Recent Extremes

We saw further jawboning around FX from Japan's Chief Cabinet Minister earlier. Kihara expressed concern around the recent sharp one-sided movements in the exchange rate and noted FX markets should reflect fundamentals. Kihara's comments echo those of other Japan officials recently, which point to increased concern around FX moves, but appear to stop short of warning of imminent intervention (of course for intervention to be successful the authorities arguably wouldn't give strong pre-warning). A simple short term fair value model of USD/JPY suggests current spot levels are getting stretched relative to fair value, but we remain within extremes seen in recent years.

- The chart below plots USD/JPY against the simple fair value estimate, which has two inputs, the US-JP 2yr swap rate differential and global equities. For the past few years this has an R^2 of just over 81%.

- At present the fair value estimate is closer to 150.00 and is diverging in terms of directional trends in spot, as US-JP yield differentials haven't tracked higher, while global equities also saw risk off recently (although that trend is likely to improve post the Nvidia results from this morning.

Fig 1: USD/JPY Spot Versus Simple Fair Value

Source: Bloomberg Finance L.P./MNI

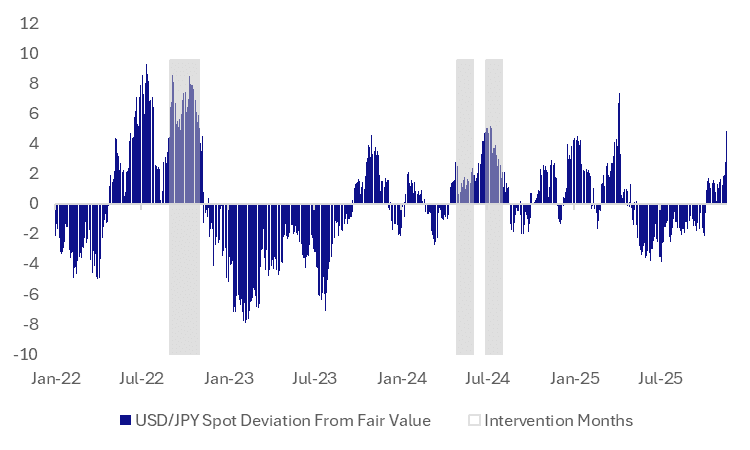

- The second chart below plots deviations in spot and this fair value estimate in percentage terms. The shaded areas indicate intervention months. Positive readings indicate USD/JPY spot is above fair value and vice versa for negative readings. We are currently around 4.8% above fair value. This is elevated but we have seen more extreme episodes in recent years.

- As the shaded areas on the chart indicate, intervention periods are associated with a positive valuation gap, but the thresholds have varied. This makes sense from the perspective that other factors are also in play, such as USD/JPY levels and also rate of change in the pair.

- On the rate of change front, the 1 month USD/JPY gain is around 3.15%, 3 month at 6.75%. Again we are getting more stretched relative to history but remain short of extremes seen in recent years.

- Still if divergences grow with fair value further, particularly if we approach the 160.00 area, market fears around intervention are only likely to become more heightened.

Fig 2: USD/JPY Deviation From Simple Fair Value & Intervention Episodes

Source: Bloomberg Finance L.P./MNI

OPTIONS: USD/JPY Option Volumes Surge, Strikes 160 & Above In Focus

USD/JPY option volumes have dominated Thursday Asia Pac trade, per DTCC. At this stage we have seen around $7bn of trades go through, which is around 57% of total options volumes per DTCC. This is well up on typical volumes seen by this part of the day (usually closer to $2.5bn or so). In terms of some of the larger volume transactions, we have seen a 170 strike call go through for expiry Feb 23 next year. There have also been numerous calls go through with 160 or higher strikes for January of next year. In terms of USD/JPY implied vols, we are looking to break higher, the 1 month was last near 10.475%, close to fresh highs since July. Previous intervention periods in 2022 and 2024 saw higher levels of implied vol, with peaks in and around the 16% region for the 1 month.

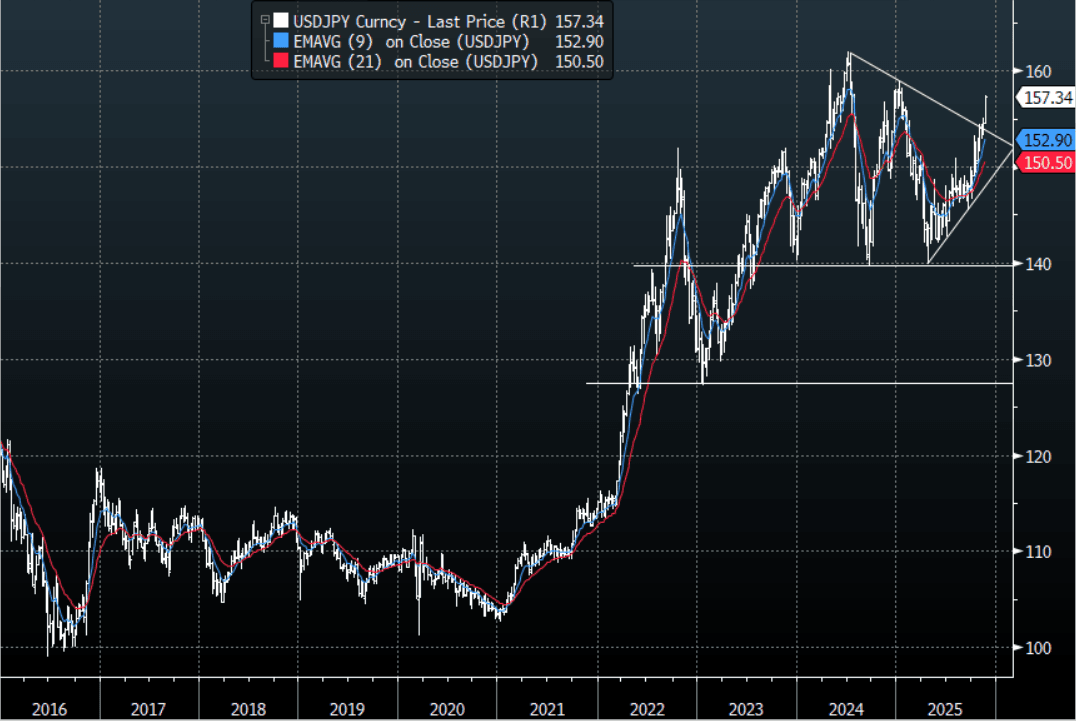

JPY: USD/JPY - Building On Gains Above 157.00

The USD/JPY range today has been 156.88 - 157.47 in the Asia-Pac session, it is currently trading around 157.35, +0.15%. The pair continued to extend higher in our session as dips remain well supported. This price action will certainly worry officials as this acceleration above 155 looks ominous and on track for a very quick test of the 160 highs seen in 2024. Japan is in a tough bind, they want to provide a significant stimulus package to boost the economy, they want to cap bond yields and they also do not want USD/JPY to explode higher. Some would say that is an impossible task and they will have to let something go, the easiest lever to pull back on is the Yen. This will not make the US happy but it's a far easier and palatable outcome than bond yields getting out of control. I suspect they will have to show some sign of fighting this above 160, but given the current inputs this could potentially go a lot higher than that.

- MNI AU - Koeda - Gives Upbeat Comments On Inflation But No Hint On Rate Hike Timing: Headlines have crossed from BoJ board member Koeda's speech. At first glance they appear in line with recent rhetoric from key BoJ board members. There were some hawkish undertones, with Koeda noting that the central bank must normalize rates to avoid distortions in the future and that underlying inflation is around 2%. She didn't give any hints on rate hike timing (which is hardly surprising ahead of Ueda's speech on Dec 1).

- "JAPAN’S 30-YEAR YIELD HITS FRESH RECORD HIGH SINCE 1999 DEBUT" - BBG

- “JAPAN CHIEF CABINET SECRETARY KIHARA: WATCHING MARKET MOVES, INCLUDING BOND MARKET, CLOSELY. RECENT FX MOVES ARE SHARP, ONE-SIDED" RTRS

- “KATAYAMA: HARD TO STRIKE BALANCE BTWN PRICES, RATES, WEAK YEN. RATES, FX ARE DECIDED BY MARKET ON VARIOUS FACTORS" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($1.49b). Upcoming Close Strikes : 155.00($933m Nov 21), 155.00{$824m Nov 24), 156.00($795m Nov 21) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 105 Points

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: USD - BBDXY Consolidates Overnight Gains

The BBDXY has had a range today of 1224.32 - 1226.47 in the Asia-Pac session; it is currently trading around 1225, +0.05%. The USD has grinded higher in our session trying to build on its overnight gains. The break back above 1221-1222 saw the USD accelerate higher and is now looking to challenge the pivotal 1230-40 area. On the day I would now be looking for dips toward 1222-1224 to be supported as the market tries to build a base from which to extend higher.

- EUR/USD - Asian range 1.1510 - 1.1542, Asia is currently trading 1.1520. The pair broke lower overnight as the USD moved higher across the board. On the day look for sellers to reemerge back toward the 1.1545-65 area, as the market looks to challenge the support toward 1.1400.

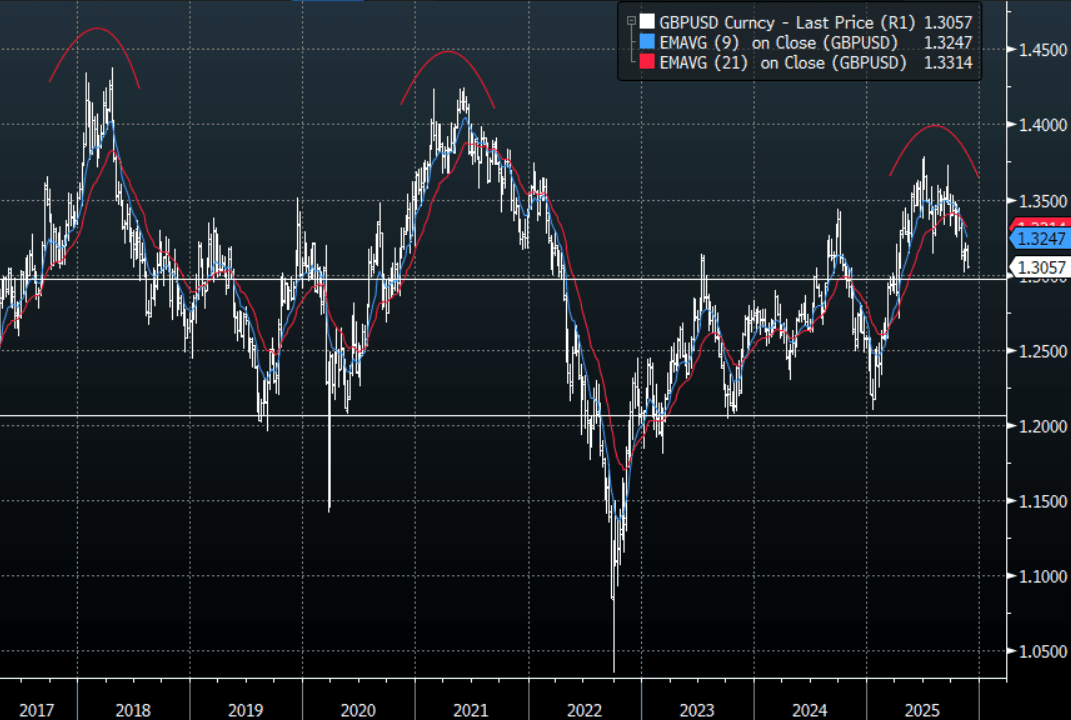

- GBP/USD - Asian range 1.3038 - 1.3063, Asia is currently dealing around 1.3145. I continue to favor fading rallies, as GBP looks to have put in a medium term top. GBP broke back below the 1.3100 support and accelerated toward the 1.3000 area overnight. I suspect rallies back toward the 1.3075-1.3095 area will be faded if we do see a bounce as the market looks to challenge the 1.3000 support.

- Cross asset : SPX +1.30%, Gold $4075, US 10-Year 4.135%, BBDXY 1225, Crude Oil $59.58

- Data/Events : EZ Construction Output MoM, Germany PP

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD/USD - Drifts Higher With Risk

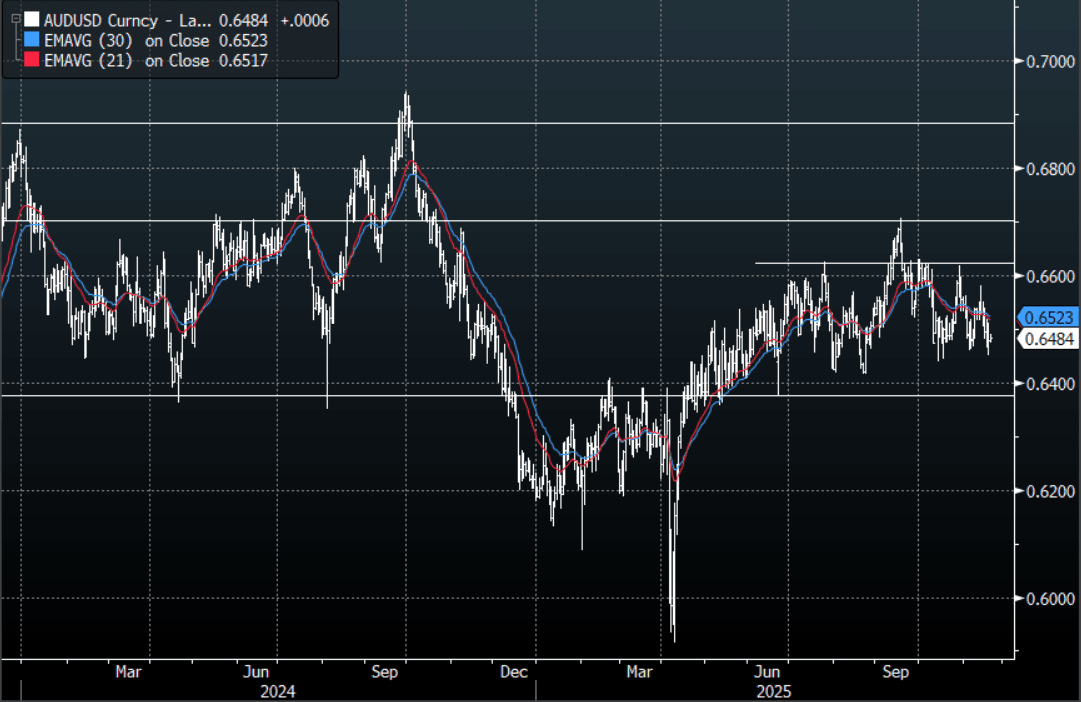

The AUD/USD has had a range today of 0.6474 - 0.6491 in the Asia- Pac session, it is currently trading around 0.6485, +0.10%. The AUD/USD has drifted higher in our session thanks to the gains for global risk provided by the strong Nvidia earnings. The AUD/USD continues to chop around within its wider 0.6350-0.6650 range, the first support is right here around 0.6440-0.6460 which has been pretty solid the last couple of months, then 0.6350 below that. It would need this move lower in risk to accelerate and become something more significant to challenge down there I would think. The AUD would need to move back above the 0.6530 area for the direction to change, until then suspect we see offers above 0.6500 initially.

- MNI AU - RBA Researching Why Inflation & Housing Stronger Than It Expected: Assistant Governor (Economic) Hunter spoke today on RBA research in areas where the transmission of monetary policy may have changed. She said it is looking at if businesses have changed price-setting after Covid, how to estimate capacity and full employment, and if monetary policy transmission channels have changed, given the larger than expected housing response to 2025’s 75bp of easing. The research appears to reflect where the economy has been stronger than the RBA expected, including inflation. This may be another indication that its current pause could be prolonged.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD736m), 0.6530 (AUD422m), 0.6550 (AUD739m). Upcoming Close Strikes : 0.6550(AUD2.28b Nov 21) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 51 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD/USD - Grinds Back Above 0.5600 As Risk Surges Higher

The NZD/USD had a range today of 0.5595 - 0.5615 in the Asia-Pac session, going into the London open trading around 0.5610, +0.15%. The NZD/USD has tried to push higher but the move has been very underwhelming considering the move in risk, perhaps the relief rally arrives when London comes in. The next target is the pivotal 0.5500 area which has been very strong support in the past. On the day look for rallies back toward 0.5635-0.5655 to find sellers initially if we do get a bounce.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5675(NZD300m). Upcoming Close Strikes : 0.5480(NZD644m Nov 21), 0.5600(NZD450m Nov 25), 0.5720(NZD646m Nov 25) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Tech Stocks Boosted by Nvidia, US Rate Outlook Concerns Remain

Nvidia's stronger earnings gave those tech heavy bourses a boost today, bouncing back from several days of caution. For those markets less tech-led the overnight softening of expectations for US rate cuts, the mood was less buoyant and will watch carefully for the key data release tonight on US labour markets. Korea, Japan and Taiwan led the way today with some individual stocks delivering strong daily returns.

- The NIKKEI had it's biggest daily gain since in a month as it jumped +2.8% today as it tries to hold above 49,900

- The KOSPI roared back above 4,000 with gains of almost 3% as SK Hynix jumped +1.2% and Samsung +4.8%

- TSMC in Taiwan led the way with gains of almost 4% as the TAIEX rose +3.1%

- China's major bourses were mostly green today, though returns were much more subdued. The Hang Seng rose just +0.14% and CSI 300 +0.38% whilst Shenzhen fell -0.10%

- SE Asian bourses all were up with Jakarta up +0.8%, Malaysia +0.27% and SE Thai +1.4%

- India's NIFTY 50 is up modestly at the open by +0.19% as new highs are reached of 26,108 as profits for the largest 100 firms grew 12% for the September quarter according to BBG.

ASIA STOCKS: Nvidia Results May Help Stabilize SK/Taiwan Outflows

Yesterday saw further meaningful outflows from tech sensitive plays South Korea and Taiwan. For the past trading month Taiwan's net equity outflows sit beyond $11bn, while for South Korea the same metric is just beyond $7.4bn. Focus will now be on how much Nvidia's better than expected earning results drive an improved inflow picture. The Kospi is up around +2.4% in earlier trade, while the NBUY function points to over $150mn in offshore inflows so far today. TSMC was up strongly in the US (+3%) post the Nvidia results in after market trading.

- Elsewhere, Indian flows continue to see-saw, with the past 5-day sum of net flows close to flat.

- Indonesia remains the main bright spot in South East Asia, with a further $100mn in net inflow yesterday. In Q4 to date net inflows stand close to $1.4bn. Local stocks are elevated but have lost a little upside momentum in recent weeks. As expected, the BI kept rates on hold with a focus shifting back to IDR stability.

- Outflow pressures were evident in other parts of SEA, with Malaysia still struggling despite generally upbeat growth prospects.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -757 | -2139 | -3955 |

| Taiwan (USDmn) | -876 | -4138 | -3778 |

| India (USDmn)* | -44 | 24 | -16186 |

| Indonesia (USDmn) | 100 | 329 | -1929 |

| Thailand (USDmn) | -45 | -74 | -3280 |

| Malaysia (USDmn) | -49 | -149 | -4449 |

| Philippines (USDmn) | -16 | -49 | -711 |

| Total (USDmn) | -1686 | -6196 | -34288 |

| * Data Up To Nov 18 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Slightly Higher As Watching Russia Events, New Sanctions From Friday

Oil prices are slightly higher in today’s APAC session but have been moving in a very narrow range as they wait for key US economic data and any further developments on a Ukraine-Russia deal after reports of a new US peace plan. WTI is up 0.2% to $59.58/bbl off the intraday high at $59.81 and Brent is 0.3% higher at $63.69/bbl after peaking at $63.83.

- Bloomberg is reporting an increase in tankers booked to bring crude from the Middle East to India signalling a shift away from Russia. Sanctions on Russian majors Rosneft and Lukoil come into effect on Friday and there have already been signs of a shift away from them and to other smaller Russian suppliers and non-Russian sources.

- The pressure is likely to stay on Russia with European leaders speaking out against its aggression involving Poland and other EU members, as well as the UK this week. The EU is also looking at measures to curtail the ongoing problem of its shadow fleet. Rosneft and Lukoil have begun considering options to divest their overseas assets.

- Later the Fed’s Hammack, Barr, Cook, Goolsbee, Miran and Paulson speak as well as BoE’s Mann and Dhingra. US November 15 jobless claims, delayed September payrolls, November Philly & Kansas Fed Indices, October existing home sales and euro area preliminary November consumer confidence print.

- Bloomberg consensus expects the US unemployment rate to be stable at 4.3% in September, payrolls to rise 51k and average earnings to rise 0.3% m/m.

Gold Steady As Fed Cut Pricing Down & US$ Up, Sept Payrolls Out Later

Gold prices are slightly lower in Thursday’s APAC trading following the October FOMC minutes showing “strongly differing views” as a result pricing for a December rate cut fell substantially and the US dollar rose, both usually negatives for non-yield bearing bullion. The US dollar is slightly higher again today and risk appetite stronger following Nvidia’s results. Gold will be monitoring US data closely, especially today’s September payrolls, as delayed releases are published.

- Our US analysts believe that Q3 GDP and November payrolls & CPI should be released before the 10 December Fed decision.

- Gold is flat at $4077.2 off the intraday low of $4042.1 which followed a peak of $4110.15, above initial resistance at $4106.7, 17 November high.

- Silver is flat at $51.36 after falling to $50.694 following an increase to $51.869 earlier. The bull trigger is at $54.480.

- Equities are rallying with the S&P e-mini up 1.2% and KOSPI +3.0%. Oil prices are slightly higher with WTI +0.2% to $59.55/bbl. Copper is down 0.1%.

- Later the Fed’s Hammack, Barr, Cook, Goolsbee, Miran and Paulson speak as well as BoE’s Mann and Dhingra. US November 15 jobless claims, delayed September payrolls, November Philly & Kansas Fed Indices, October existing home sales and euro area preliminary November consumer confidence print.

- Bloomberg consensus expects the US unemployment rate to be stable at 4.3% in September, payrolls to rise 51k and average earnings to rise 0.3% m/m.

INDONESIA: BI Cautious But Retains Easing Bias, Further Cuts Forecast

Bank Indonesia left rates at 4.75% as was widely expected as it shifted its focus to rupiah stability and noted a lower “probability of a further reduction in the Federal Funds Rate this year”. Its concern around portfolio inflows also suggests it would like to rebuild FX reserves given its consistent intervention to support the rupiah. It appears that it has become more cautious after cutting rates 3 times in Q3 but retains an easing bias.

- JP Morgan notes that the slowdown in BI’s government bond purchases may be to encourage portfolio inflows by “restoring carry appeal to foreign investors”. Given the lower probability of further Fed easing and increased domestic risks from the 3% budget ceiling review, it has pushed out its remaining 2 rate cuts to Q2 2026.

- Societe Generale highlights the risks around lending observing that the government injection of IDR 200bn into state-owned banks could improve transmission of BI easing but increases inflation risks and “as credit growth accelerates amid weak economic fundamentals, banking sector stress could intensify”. It believes that growth concerns will drive BI to cut three more times bringing rates to 4.0%.

- MUFG estimates the neutral rate to be around 4.5%, only 25bp below where BI is now. It expects another 25bp cut at the 17 December decision with two in H1 next year to stimulate growth. It notes that the key risks facing Indonesia given both accommodative monetary and fiscal policy are “higher inflation, fiscal slippage, and rupiah weakness”. MUFG also expects “USDIDR to rise to 16,900 by end-2025 before easing slightly to around 16,700 by end-2026”, above BI’s 16,430 2026 forecast.

- Given its easing bias to support growth, Goldman Sachs expects BI to cut 25bp in December and then again in Q1 2026.

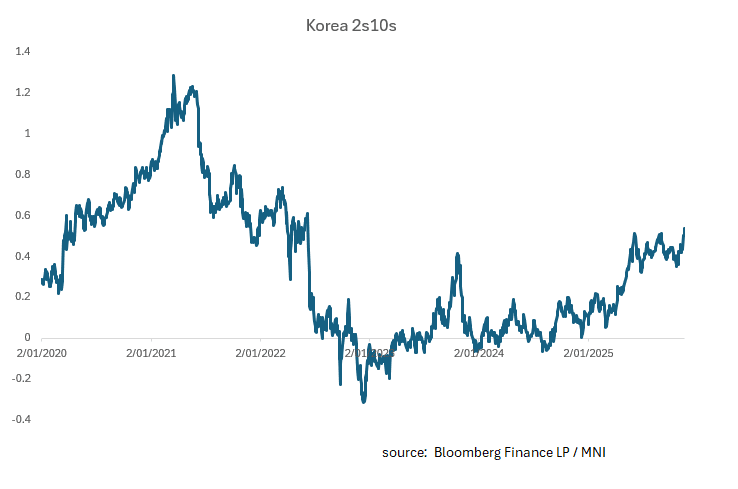

SOUTH KOREA: 2s10s Curve May Steepen on Issuance Risks

- The steepening of the curve had taken a breather leading up to the October BOK meeting having oscillated around +48 for some time.

- Rates are predominantly on hold due to concerns about the real estate sector, particularly property prices in Seoul. The outlook for growth in Korea is improving given easing trade tensions, but from a low base and may require more support. The projected fiscal deficit of -2.3% of GDP may have some upside risks given the inability to support the economy via rate cuts.

- Current forecasts suggest a mere +1.0% GDP growth for 2025 (rising to 1.9% in 2026) as South Korea’s new government plans a significant increase of its annual budget to revive an economy under pressure from US tariffs, rising welfare costs and an aging population.

- The proposed budget for 2026 is an +8.1% increase and the government plans to issue a record amount of bonds to fund the government spending and will target technology-driven growth, stronger small businesses and more balanced regional development.

- The government has shown a willingness to issue in the 10-Yr part of the curve, to meet the demand from insurance companies.

- In 2020 the COVID impacted budget resulted in a deficit of -2.7% and GDP growth the following year of 4.6%. The deficit for 2024 was -3.3% with a skew towards the back end of the year.

- This suggests there is room for further fiscal expansion and now that the trade deal is finalized, could be a focus for the Lee government.

- Looking back at the post 2020 environment, curves peaked in early 2021 at 1.2% following the impact of various COVID related policies.

- This could suggest potential steepening to occur in KTBs as issuance and growth assumptions are recalibrated.

- Swap markets indicate the BOK on hold for all or most of 2026 suggesting that the bond market may take its guidance from elsewhere meaning an uptick in issuance could see longer bond yields higher whilst the front end remains anchored.

ASIA FX: USD/KRW Still Close To 1470 As Weaker Yen Offsets Equity Bounce

In North East Asia FX, aggregate moves in FX haven't been large, amidst multiple cross asset trends. USD/CNH probed above 7.1200 but found selling interest. USD/KRW downside has proved fleeting, despite an onshore equity bounce. USD/TWD downside have also proven modest. South Korean and Taiwan shares have surged around 3%, as Nvidia earnings in the US were better than forecast and reduced fears (at least in the near term) around chip/AI bubble concerns. Some offset is coming from higher USD/JPY levels, which is probing through 157.50. The broader USD backdrop still looks supportive amidst firmer yields (although AUD and NZD have ticked higher).

- USD/CNH is back to 7.1185/90, so still close to session higher. BBG reported earlier that the authorities are considering fresh measures to boost housing demand. Local equities are higher but gains are modest so far. The USD/CNY fixing edged up but the fixing error was also wider.

- Spot USD/KRW got to lows of 1465.9 in the first part of trade, as equity sentiment was positive. We remain supported on dips though, with an upside focus on a move back above 1470. Recent highs have been marked around the 1475 region, but this may see fresh supply from exporters and/or asset managers emerge.

- Spot USD/TWD is a little lower, last near 31.22/23. Earlier we got to fresh multi month highs of 31.26. Focus will be on whether offshore inflows return in large enough size to boost TWD. Note later on we get Taiwan export orders for Oct.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 20/11/2025 | 0700/0800 | ** | PPI | |

| 20/11/2025 | 1000/1100 | ** | EZ Construction Output | |

| 20/11/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 20/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 20/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 20/11/2025 | 1330/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/11/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1330/0830 | *** | Employment Report | |

| 20/11/2025 | 1345/0845 | Cleveland Fed's Beth Hammack | ||

| 20/11/2025 | 1430/0930 | Fed Governor Michael Barr | ||

| 20/11/2025 | 1500/1000 | *** | NAR existing home sales | |

| 20/11/2025 | 1500/1000 | * | Services Revenues | |

| 20/11/2025 | 1500/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 20/11/2025 | 1600/1100 | ** | Kansas City Fed Manufacturing Index | |

| 20/11/2025 | 1600/1100 | Fed Governor Lisa Cook | ||

| 20/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 20/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 20/11/2025 | 1740/1240 | Chicago Fed's Austan Goolsbee | ||

| 20/11/2025 | 1800/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 20/11/2025 | 1830/1830 | BOE Dhingra Speech on Trade and Tariffs | ||

| 20/11/2025 | 2100/2100 | BOE Mann at IMF Statistical Forum | ||

| 21/11/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 20/11/2025 | 2315/1815 | Fed Governor Stephen Miran | ||

| 21/11/2025 | 2330/0830 | *** | CPI | |

| 20/11/2025 | 2345/1845 | Philly Fed's Anna Paulson | ||

| 21/11/2025 | 0001/0001 | ** | Gfk Monthly Consumer Confidence | |

| 21/11/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 21/11/2025 | 0700/0700 | *** | Public Sector Finances | |

| 21/11/2025 | 0700/0700 | *** | Retail Sales | |

| 21/11/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 21/11/2025 | 0800/0900 | ECB de Guindos Remarks/Q&A at Foro Gran Via | ||

| 21/11/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0830/0930 | ECB Lagarde Speech at European Banking Congress | ||

| 21/11/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 21/11/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 21/11/2025 | 1000/1100 | Negotiated Wage Growth | ||

| 21/11/2025 | 1130/1230 | ECB de Guindos Remarks/Q&A at Deusto Business School | ||

| 21/11/2025 | 1230/0730 | New York Fed's John Williams | ||

| 21/11/2025 | 1330/0830 | ** | Retail Trade | |

| 21/11/2025 | 1330/0830 | Fed Governor Michael Barr | ||

| 21/11/2025 | 1345/0845 | Fed Vice Chair Philip Jefferson |