AUSSIE BONDS: Trading Heavy As RBA Research Suggests Prolonged Pause

ACGBs (YM -5.0 & XM -5.0) are weaker and at/near session lows.

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session as the market continues to digest yesterday's release of the FOMC Minutes.

- Cash ACGBs are 5bps cheaper, with the AU-US 10-year yield differential at +33bps.

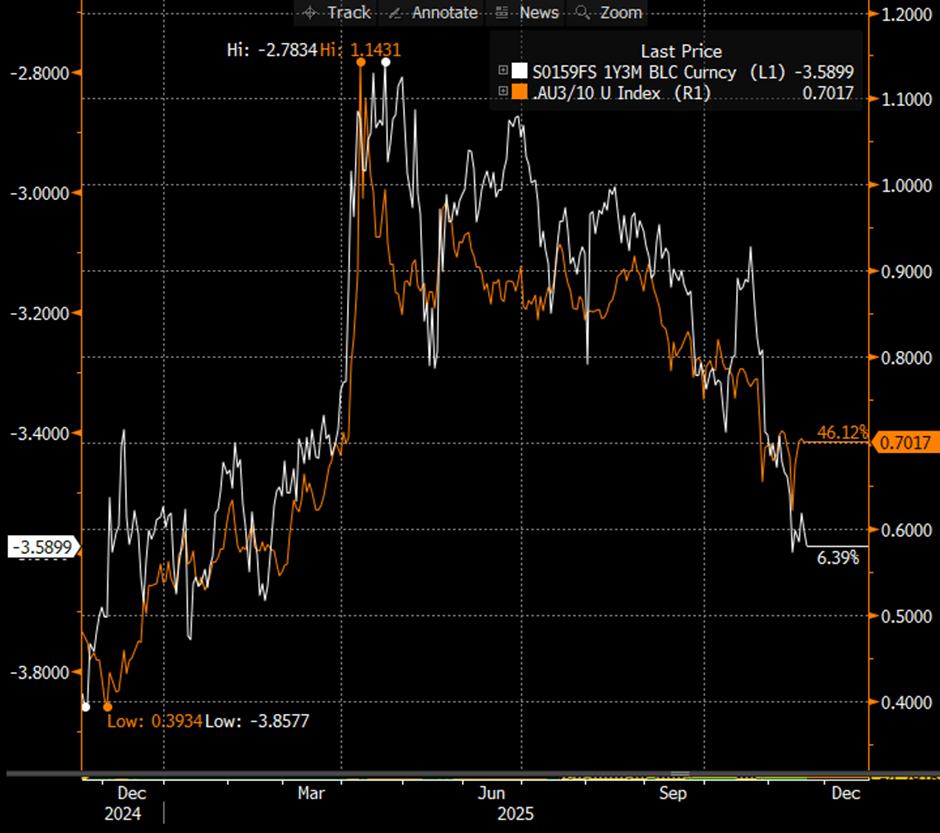

- Unlike its New Zealand counterpart, which has recently steepened to its highest level since 2021, the ACGB yield curve remains near its flattest point since April, albeit slightly steeper than its recent low. Moreover, the AU 3s10s yield curve appears vulnerable to any upward revision in year-ahead cash rate expectations (see chart).

- Assistant Governor Hunter spoke today on RBA research in areas where the transmission of monetary policy may have changed. The research appears to reflect that the economy has been stronger than the RBA expected, including inflation. This may be another indication that its current pause could be prolonged.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 10bps of easing priced by mid-2026.

- The bills strip is -4 to -7 beyond the 1st contract (-1).

- Tomorrow, the local calendar will see S&P Global PMIs (P).

- The AOFM plans to sell A$700mn of the 1.25% 21 May 2032 bond on Friday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold & Silver Fall As Equities & US Dollar Strengthen, Focus Remains On US

Gold has stabilised today during the APAC session after rising 2.5% on Monday. Prices rose to $4375.38/oz and then fell to $4332.95 and are now down 0.4% to $4340.5. Equities are rallying and the US dollar is slightly stronger (BBDXY +0.1%) but the factors bullion ignored yesterday may have also contributed to the pause in the rally. It is in overbought territory, 2025 Fed easing is already priced in, there is talk that the US government shutdown could end this week and US-China trade tensions appear to have eased.

- Both gold and silver continue to hold well above initial support levels of $4140.8, 15 October low, and $48.736, 20-day EMA, respectively.

- The 1 November deadline for a US-China trade deal remains but President Trump said that the US will “be fine” with China. Economic Council Director Hassett also gave indications that the government shutdown could conclude this week.

- Silver is down 1.1% to $51.87 after falling to $51.607. It is a smaller market than gold and so moves tend to be amplified. It is also signalling that it is overbought.

- Equities are stronger across the region with the Hang Seng up 1.7% and ASX +0.7% but the S&P e-mini is flat. Oil prices are lower with WTI -0.3% to $56.84/bbl. Copper is 0.2% higher.

- Later US October Philly Fed non-manufacturing and September Canadian CPI print. ECB President Lagarde and Board member Lane speak.

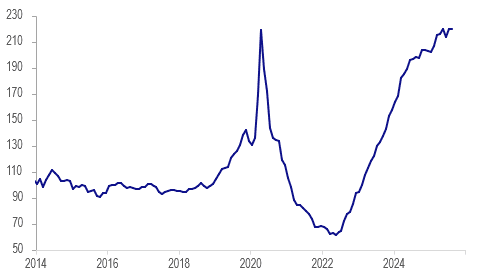

AUSTRALIA: Improved Q3 Job Ads May Signal Better Q4 Labour Market

SEEK data show that labour demand improved over Q3 while supply remains positive it slowed. With Q3 employment rising only 0.2% q/q down from Q2’s 0.6%, SEEK job ads may be signalling some possible improvement over Q4. A stabilisation of the labour market would be helpful for monetary policy decision makers if inflation prints to the upside.

Australia SEEK job ads %

- September SEEK new job ads rose 1.1% m/m, the third straight monthly increase. Ads increased 1.7% q/q in Q3 a clear pick up after Q2’s 0.6% q/q contraction. They are still down 2.4% y/y in September but that follows -12.6% y/y in March and is the best result in almost three years.

- Applicants per job were little changed in August rising 0.1% m/m and 10.9% y/y following July’s 2.8% m/m & 11.7% y/y. It seems that growth in labour supply slowed in Q3 after rising 4% q/q in Q2. In Q3, the labour force grew 1.8% y/y while employment was up 1.5% y/y.

- SEEK noted that a number of large industries had increased job ads including trades & services, manufacturing and transport & logistics. Professional and financial services continue to decline.

Australia SEEK applicants per job 2013=100

Source: MNI - Market News/SEEK

JGBS: Modestly Richer, Oct 30 BOJ Hike At 25% Chance

JGB futures are stronger, +16 compared to the settlement levels, but off session bests.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session after yesterday's gains.

- Cash JGBs are slightly richer across benchmarks, with yields 1-2bps lower. The benchmark 10-year yield is 1.0bp lower at 1.664%, outperforming the futures-linked 7-year. This continued the recent trend, which has unwound the relative cheapening of the 10-year earlier in the year.

- Japan sold ¥300bn of 10-year climate transition notes at a cut-off yield that was lower than expectations, signalling lacklustre investor demand. The cut-off yield was 1.680%, compared with 1.695% estimated by traders in a Bloomberg survey. The bid-to-cover ratio was 3.56x, compared with 3.31x in October 2024, the last time the government sold the bonds.

- Swap rates are little changed.

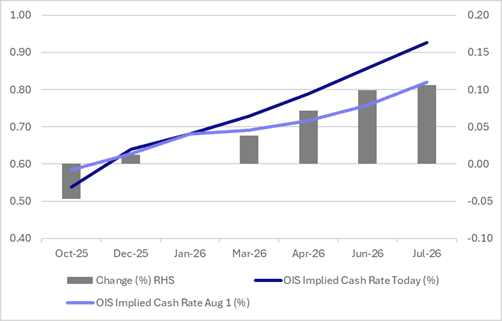

- BOJ-dated OIS pricing is little changed across 2025 meetings compared to early August levels. Pricing is, however, firmer for 2026 meetings out to July. Current OIS pricing implies just a 24% probability of a 25bp hike in October, rising to 65% by December and 82% by January. A full 25bps hike is not fully priced until March 2026. (see chart)

- Tomorrow, the local calendar will see Trade Balance data.

Figure 1: BOJ-Dated OIS – Today Vs. August 1

Source: Bloomberg Finance LP / MNI