AUSSIE BONDS: Cheaper With US Tsys Post-FOMC, Risk-On After Nvidia Beat

ACGBs (YM -5.0 & XM -4.5) are weaker after cash US tsys finished 2-3bps cheaper following the release of the October Meeting FOMC Minutes.

- Wall Street rebounded ahead of Nvidia’s earnings but finished below its early highs. After the close, US equity futures moved higher after Nvidia reported results that topped expectations.

- The improvement in risk appetite weighed on US tsys, as did expectations that the FOMC will hold off on a December rate cut.

- While opinions "differed strongly", the minutes suggest that it may only be a minority of the Committee that is pushing for a follow-up cut.

- That was largely in line with MNI's view that a majority of the broader Committee may be leaning to a December hold based on post-October FOMC commentary.

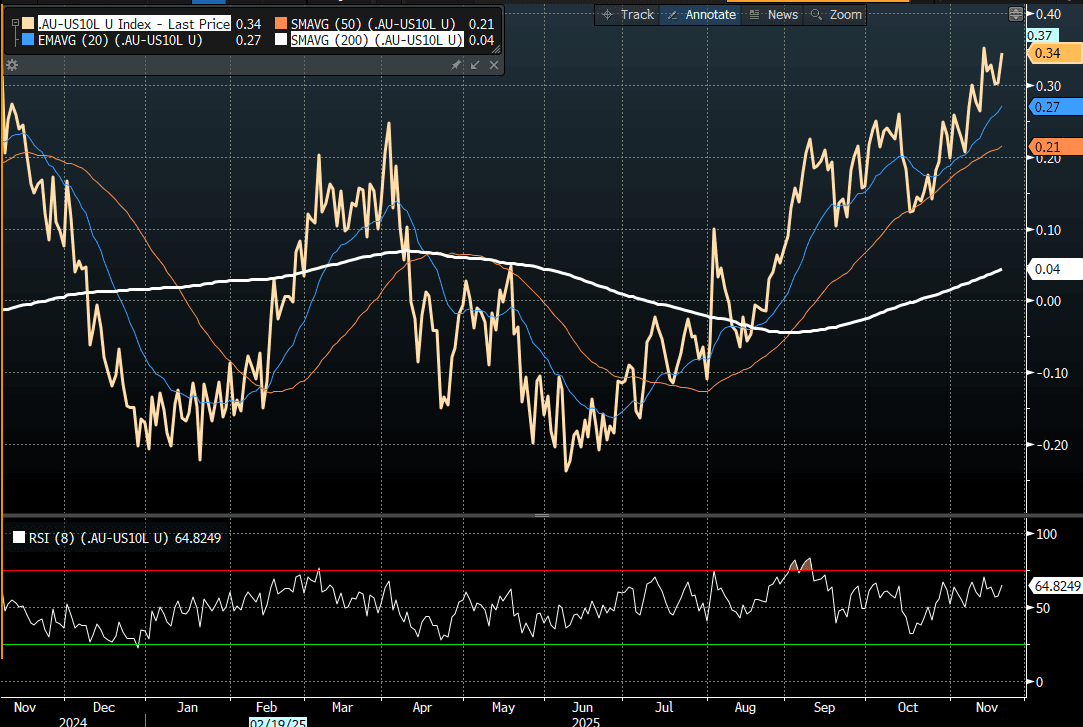

- Cash ACGBs are 5bps cheaper with the AU-US 10-year yield differential at +33bps. (see chart)

- The bills strip is -2 to -5 across contracts, with a flattening bias.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 11bps of easing priced by mid-2026.

- Today, the local calendar will see RBA's Sarah Hunter speak at the Australia Industry Group.

- The AOFM plans to sell A$700mn of the 1.25% 21 May 2032 bond on Friday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

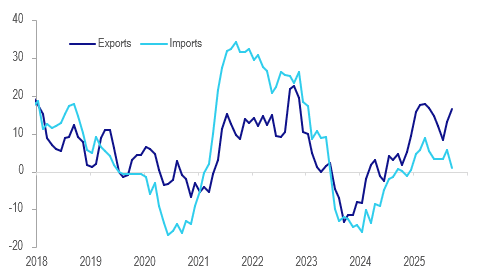

NEW ZEALAND: Export Growth Strong, Imports Reflect Soft Domestic Growth

Export growth is a bright spot in the NZ economy which was up 19% y/y in September after 21% y/y. The strength is being driven by higher dairy prices but also an increase in milk & cheese export volumes. Import growth remains lacklustre reflecting ongoing soft domestic demand. As a result the goods trade deficit in the year to September narrowed to $2.25bn from $3.06bn.

NZ goods exports vs imports y/y% 3-month moving average

Source: MNI - Market News/LSEG

- Statistics NZ reports that Q3 goods export values rose 3.6% q/q after Q2’s -3.4%, while imports fell 0.1% q/q after -0.6%, signalling ongoing domestic weakness in the quarter. Another rate cut is likely in November.

- The monthly merchandise trade deficit is trending higher again after posting surpluses over February to June. September’s deficit was $1.35bn after $1.23bn.

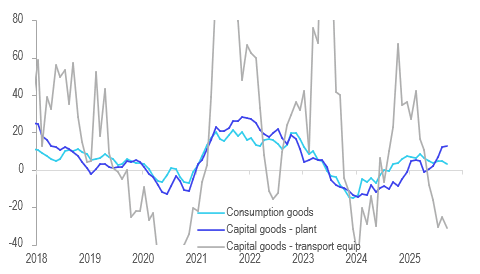

- Imports rose 1.6% y/y up from -1.0% y/y in August. The weakness has been driven by transport equipment which sank -46.1% y/y. Non-transport capital goods imports are strengthening rising 14.9% y/y in September. Consumer goods imports are recovering rising 7.4% y/y but the 3-month average growth rate is still only 3.3% y/y.

- Merchandise exports to NZ’s major destinations are growing strongly with shipments to China up 24.2% y/y driven by dairy and cereal products. They rose 10% y/y to the US due to fats/oils, pharmaceuticals and fruit. Exports to Australia are very strong up 27.7% y/y and are recovering to Japan rising 11.0% y/y 3-month average.

NZ merchandise imports y/y 3-month moving average

AUSSIE BONDS: Modestly Richer With US Tsys, PM Albanese In Washington

ACGBs (YM +1.0 & XM +2.0) are slightly stronger after a solid day for US tsys.

- The US 2-year was steady at 3.46%, holding under 3.50%. But with the Fed priced in, further downside is limited. The 10-year rate dropped 3bps to 3.98%.

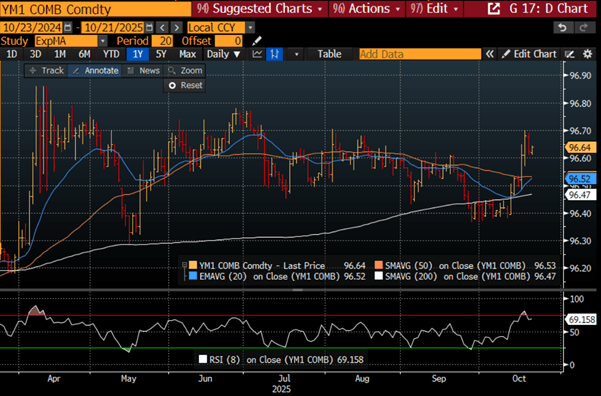

- MNI Tech: Aussie 3-yr futures surged on the resumption of trade after the weekend, returning focus higher despite the break of support last week. Short-term resistance at 96.615, the Sep 12 high, has been broken, with 96.780 as the next upside target.

- Prime Minister Anthony Albanese is in Washington for a White House meeting with Donald Trump.

- Cash ACGBs are 2bps richer with the AU-US 10-year yield differential at +15bps.

- The bills strip is slightly mixed, with pricing -1 to +1.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in November is given a 70% probability, with a cumulative 24bps of easing priced by year-end.

- The local data calendar is fairly quiet throughout the course of this week.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond today, A$900mn of the 2.75% 21 June 2035 bond on Wednesday and A$800mn of the 2.75% 21 November 2029 bond on Friday.

Bloomberg Finance LP

US TSYS: 10-Yr Below 4.00% Again as 30-Yr Outperforms

Treasury futures finished the US session modestly higher after testing morning highs as Trump talks tough on China saying that if they don't do business with the US and threaten us with rare earths, I will reply with tariffs. TYZ5 finished higher by +04 at 113-19, as it consolidates above all major moving averages. The 20-day EMA below is at 113-03. TYZ5 has opened at 113-19+ in Asia trading with limited early price action.

- The US 2-Yr did very little overnight, remaining where it ended Friday at 3.45%

- The US 5-Yr finished -2bps lower at 3.57%

- The US 10-Yr slipped back below the 4.00%, finishing at 3.98% as it again tests the recent ranges of 4.00 -4.20%.

- The USD 30-Yr was strong, rallying 3bps to finish at 4.57%. The 30-Yr is now back at levels of April.

Rumours continue to remain around regional banks credit risk, impacting risk appetite and the demand for treasuries. Two year yields are at 2022 levels as bond investors turn their attention to the US CPI out later in the week. Current forecasts are for a modest uptick in the YoY release to 3.1% (2.9% prior) and the MoM to remain flat at 0.4%.