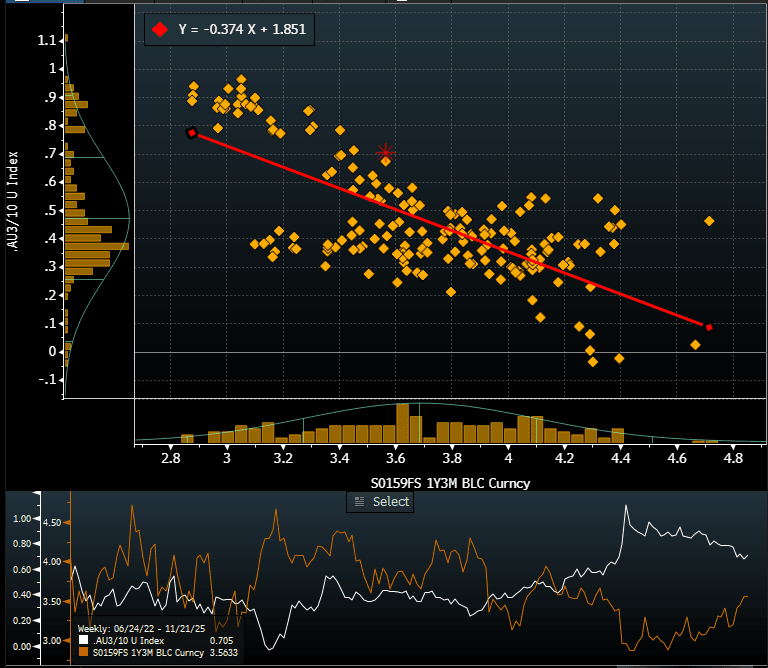

AUSSIE BONDS: Yield Curve Looks Too Steep Vs. Mkt Exp For RBA Cash Rate

The Australian 3s/10s cash curve is little changed today at +71bps, close to its flattest level since April. The recent curve flattening has occurred alongside a steady rise in market forward expectations for the RBA cash rate.

- Minutes from the November meeting reiterated that the RBA’s central scenario remains “in balance,” with risks to both the upside and downside. How these risks evolve will shape whether policy stays on hold or shifts toward further easing. While it is “not yet possible to be confident” about which path will prevail, the Board will remain cautious and data-dependent. With core inflation still above target and demand showing signs of recovery, policy is likely to remain on hold in December and into early 2026, subject to incoming data.

- Market pricing, proxied by the 1-year forward 3-month swap rate (1Y3M), has risen about 50bps since mid-June. RBA-dated OIS now assigns only a 3% probability to a 25bp cut in December, with a cumulative 13bps of easing priced by mid-2026.

- A simple regression of the 3s/10s curve against the 1Y3M rate over the past three years suggests the current curve is roughly 20bps too steep relative to its fair value.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

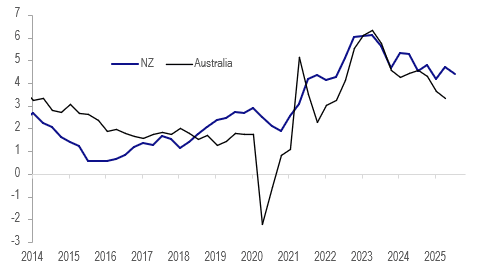

AUSTRALIA: NZ CPI Data Suggests Stable Q3 Australian Core

Q3 NZ CPI was released this week and given high correlations it has some information for Australia’s CPI out on 29 October. The RBNZ’s sector factor model measure of core was stable at 2.7% y/y in Q3 signalling that Australia’s may also remain around Q2’s 2.7%, which is consistent with monthly data. NZ’s domestic-related non-tradeables and services annual inflation moderated while goods and tradeables were higher.

Australia vs NZ underlying CPI y/y%

- NZ services inflation moderated to 4.4% y/y in Q3 from 4.7% while it picked up to 1.2% q/q from 1.1%. There is around an 85% correlation with Australia’s headline annual services inflation and 50% with the quarterly rate. Even if there is an increase in Australia’s quarterly rate in Q3 from Q2’s 0.7%, the 3.3% annual rate should moderate given it rose 1.1% q/q in Q3 2024.

- NZ’s services inflation has been running well ahead of Australia’s and has seen little disinflation since the start of 2024, which may be warning.

- It is worth noting though that the RBA focuses on market services (ex volatile items) which rose 0.6% q/q & 2.9% y/y in Q2. Governor Bullock has stated that the RBA was concerned about some of the components and sticky services prices overseas.

- NZ non-tradeables moderated 0.2pp to 3.5% y/y in Q3 and Australia’s could also ease given the correlation is over 90%. The two have been trending lower for around 2 years.

- NZ goods and tradeables inflation picked up in Q3, which given the global nature of many and high correlations Australia could see this too.

- Australia’s headline CPI continues to be impacted by temporary government electricity rebates and so it is currently not helpful to look at the relationship with NZ.

Australia vs NZ services CPI y/y%

Source: MNI - Market News/LSEG

CNH: USD/CNY Fixing Edges Up, Fixing Error Close To Unchanged, CNH Steady

The USD/CNH fix printed at 7.0954, which is modestly up on yesterday's print (which was a fresh YTD low). The fixing error is close to unchanged at -297pips, so it didn't widen despite the firmer USD index levels through Tuesday. USD/CNH was last 7.1265/70, unchanged for the session. Today's fixing is unlikely to give fresh downside impetus to the pair. Broader USD sentiment is a touch softer with yen modestly outperforming the G10 space (amid a slight downtick in both US equity futures and Tsy yields).

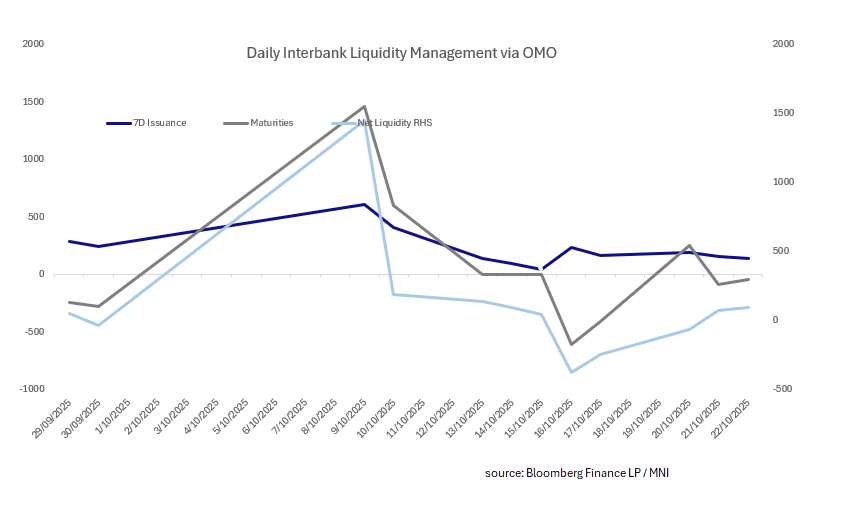

CHINA: Central Bank Injects CNY94.7bn via OMO

- The PBOC issued CNY138.2bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY43.5bn.

- Net liquidity injects CNY94.7bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.44%.

- The China overnight interbank repo rate is at 1.30%, from the prior close of 1.30%.

- The China 7-day interbank repo rate is at 1.40%, from the prior close of 1.44%.