MNI US Macro Weekly: Fed Divided As Data Trickles Back In

Nov-21 2025 19:56By: Tim Cooper and 1 more...

USFederal Reserve

Hidden PDF

Executive Summary

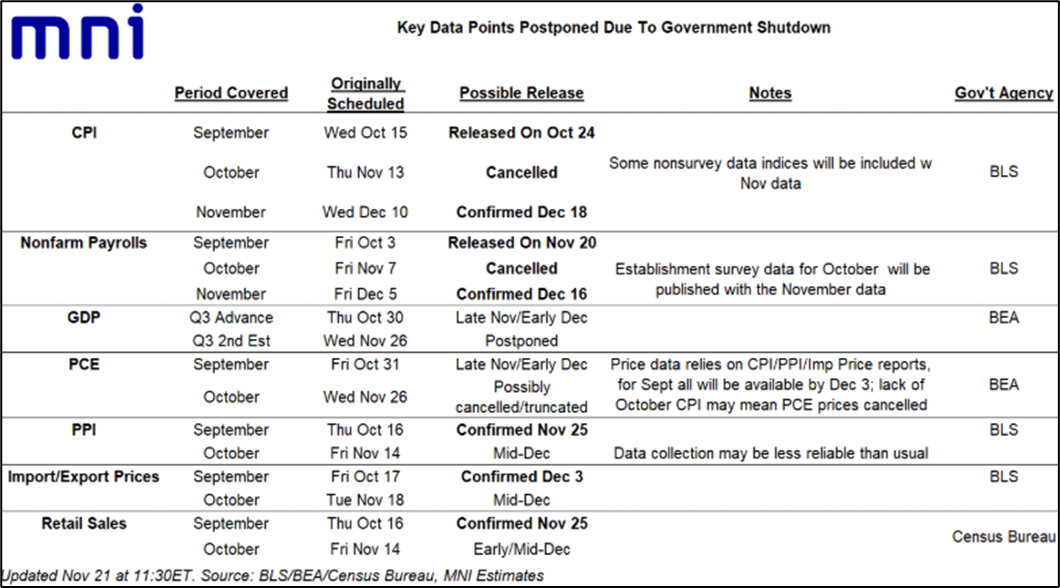

- The “fog” of data following the federal government shutdown is only slowly lifting, with the return of official national-level reports this week largely limited to August and September-vintage releases.

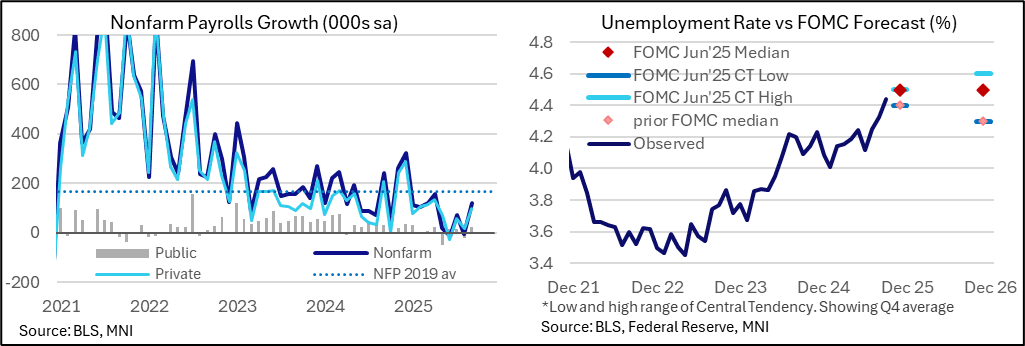

- The long-postponed September Employment Situation report delivered a largely solid if slightly stale snapshot of the US labor market, with an unexpectedly large uptick in the unemployment rate to a 4-year high appearing to outweigh consensus-beating payrolls growth to deliver a slightly dovish market reaction.

- NY Fed’s Williams however had the largest impact of the week on Friday, in an uncharacteristic steer from a core member of the FOMC towards a further adjustment in the “near term”. We end the week with 16bp of cuts priced for Dec (vs 6bp pre-payrolls), 25bp for Jan and 58bp for June.

- The minutes for the Oct 28-29 FOMC meeting were hawkish, at the time suggesting that it may only be a minority of the Committee that is pushing for a follow-up cut in December. And most other Fedspeak erred on the hawkish or at least cautious about a December cut side, with various speakers most sounding concerned about the latest increase in the unemployment rate in September.

- But Williams reinforced our view that FOMC voters are leaning to deliver a “hawkish cut” in December, with Williams part of a core bloc including Chair Powell in support.

- The latest BLS reschedulings mean the Fed won't get October or November nonfarm payrolls or CPI reports ahead of its Dec 10 decision, and the October data will be heavily truncated.

- As such the assessment of the current state of play will largely come down to interpreting alternative data points. Again, activity data is showing little sign of relenting, “alternative” measures of labor market health show conditions certainly haven’t improved since September but neither is it likely that the bottom is falling out; and unfortunately the lack of reliable inflation data stands out and is likely to keep hawks cautious.

- The Fed speaker schedule next week – the last before the pre-FOMC meeting blackout period begins – is barren as usual for Thanksgiving. In previous years we’ve had only one or two regional Fed presidents make television appearances, but there are no speeches scheduled (merely underlining how important Williams’s appearance was as a potential steer from Fed leadership on their pre-meeting rate preference).

- That will keep attention on the Beige Book release, an especially important edition given Fed policymakers’ increased reliance on anecdotal information from contracts.

- We also get delayed retail sales and PPI reports for September, while jobless claims will be watched particularly closely, both for latest initial claims for signs of layoffs and a notable update for continuing claims. The latter covers the payrolls reference period for November and will be an important reference point for FOMC members trying to get a sense of latest unemployment rate clues.