AUSSIE BONDS: Modest Rally But AU-US 10Y Diff At Highest Level Since Late 2022

ACGBs (YM +2.0 & XM +1.0) are marginally stronger but well off session highs.

- Cash US tsys are flat to 1bp cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's risk-off induced rally.

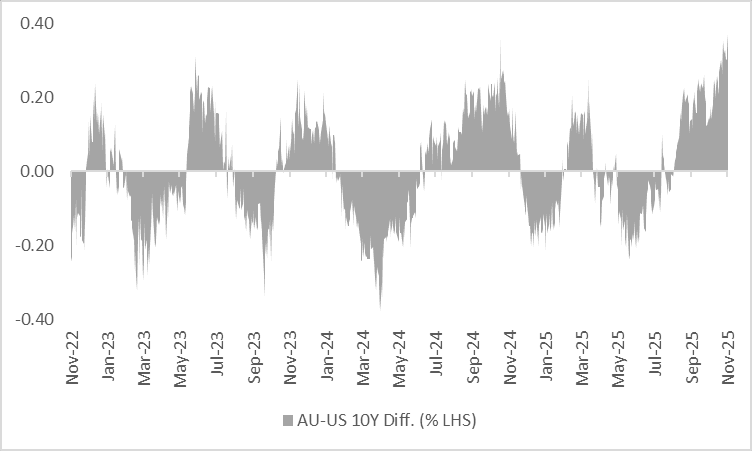

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +37bps, the highest since late 2022. (see chart)

- However, a simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is +7bps to fair value.

- The latest ACGB May-32 supply achieved a weighted average yield that printed 0.44bp through prevailing mids (per Yieldbroker). Moreover, the cover ratio increased, rising to 3.5171x from 3.3850x.

- The bills strip is little changed.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 11bps of easing priced by mid-2026.

- The local calendar will be empty until Wednesday’s October CPI data.

- Next week, the AOFM plans to sell A$400mn of the 4.25% 21 June 2034 bond on Tuesday, A$700mn of the 2.75% 21 November 2029 bond on Wednesday and A$900mn of the 3.75% 21 April 2037 bond on Friday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Report US-India Deal Close Drives Oil Higher, EIA US Stock Data Out Later

Oil has found support today from data showing a US inventory drawdown and news that the US and India are close to a deal to gradually reduce India’s Russian oil imports and US tariffs. Less Indian consumption of Russian crude would increase its demand for other sources boosting prices. WTI is up 1.7% to $58.23/bbl following a high of $58.38, remaining below the 50-day EMA at $61.76. Brent is 1.5% higher at $62.26/bbl after reaching $62.47 (50-day EMA $65.35).

- A US-India trade deal is apparently close to completion which would allow the current 50% US duties to be reduced to around 15%, according to Bloomberg citing Mint. US President Trump has said recently that Indian PM Modi had agreed to ending imports of Russian oil. Mint is saying that the agreement could be announced at the 26-28 October ASEAN meeting.

- Oil has also found support from Tuesday’s announcement that a million barrels with delivery in December and January will be purchased for the US’ SPR, which reached a low in July 2023 and was only 17% higher last week.

- After rising the previous week, Bloomberg reported US oil inventories fell 3mn barrels last week, according to people familiar with the API data. Product stocks were also lower with gasoline down 0.2k and distillate 1mn. The official EIA data is out Wednesday.

- Later UK September CPI data print and ECB President Lagarde and Board members Buch and de Guindos speak.

JGBS: Slightly Richer As Market Digests Fiscal Policy News

JGB futures are slightly stronger, +2 compared to the settlement levels, but well off session lows.

- Headlines have crossed from Japan's Growth Strategy Minister Minoru Kiuchi. Kiuchi stated that the focus now is compiling an economic stimulus package, albeit with one eye still on fiscal discipline (DJ) (and diverse funding sources). Various ministers are being consulted, with a focus on helping tariff impacted sectors. Kiuchi stated that no timeline is set for when the economic package will be compiled. Early focus for markets for the new Takaichi regime is fiscal stimulus, in terms of size and how it will be funded (particularly with parallels drawn with the Abenomics-like policy set).

- Cash US tsys are slightly richer in today's Asia-Pac session.

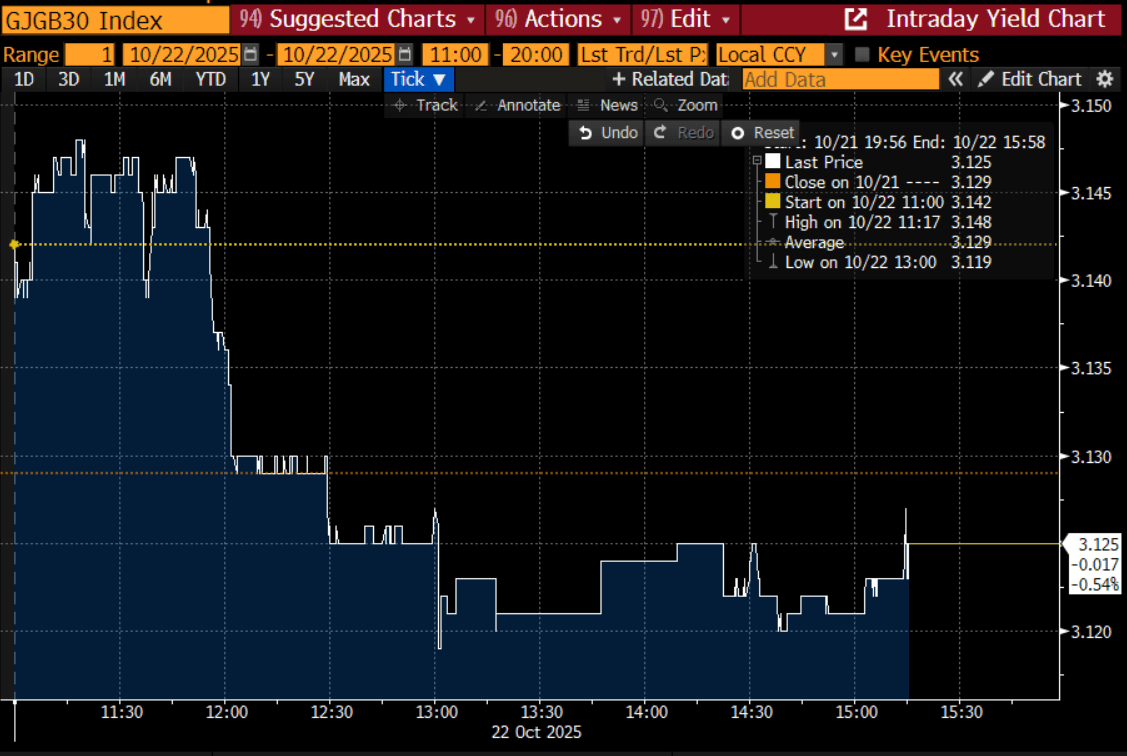

- Cash JGBs are flat to 1bps richer across benchmarks, but significantly better than early session yield highs, as the market digested today’s news on the fiscal policy.

- The benchmark 30-year yield is 0.6bp lower at 3.125% versus the session high of 3.148%. (see chart) Notably, the current yield is more than 20bps below the cycle high of 3.351%, hit shortly after Takaichi was announced as the LDP leader.

- Swap rates are little changed.

- Tomorrow, the local calendar will see Weekly International Investment Flow data alongside Auction for Enhanced-Liquidity 15.5-39 YR.

Bloomberg Finance LP

US TSYS: Modest Declines in Yields Again Today

Bond futures finished -01 lower today for TYZ5 on low volumes, looking for a catalyst for the next move .

- The US 2-Yr did very little all morning before rising modestly to 3.465 in the afternoon trading session.

- The US 5-Yr ground was flat at 3.56%

- The 10-Yr has consolidated below 4.00%, rallying again modestly by -0.5bps to reach 3.96% in line with October 24 yield levels.

- The 30-Yr continues to outperform rallying -0.5bps overnight to reach 4.53%. Likely next inflection point could be the April lows of 4.40%.

- Yield moves are appearing disjointed relative to current interest rate pricing as the government shutdown continues as bond traders agonize over the potential impact on the economy. New ranges are being defined and as markets await the release of the September CPI, markets appeared skewed towards lower yields for now.

- There is limited Tier 1 data releases for markets to follow tonight, only MBG mortgage applications. Equity weakness in Asia will be watched for any follow through particularly as many bourses reach new highs.