GOLD: Gold Steady As Fed Cut Pricing Down & US$ Up, Sept Payrolls Out Later

Gold prices are slightly lower in Thursday’s APAC trading following the October FOMC minutes showing “strongly differing views” as a result pricing for a December rate cut fell substantially and the US dollar rose, both usually negatives for non-yield bearing bullion. The US dollar is slightly higher again today and risk appetite stronger following Nvidia’s results. Gold will be monitoring US data closely, especially today’s September payrolls, as delayed releases are published.

- Our US analysts believe that Q3 GDP and November payrolls & CPI should be released before the 10 December Fed decision.

- Gold is flat at $4077.2 off the intraday low of $4042.1 which followed a peak of $4110.15, above initial resistance at $4106.7, 17 November high.

- Silver is flat at $51.36 after falling to $50.694 following an increase to $51.869 earlier. The bull trigger is at $54.480.

- Equities are rallying with the S&P e-mini up 1.2% and KOSPI +3.0%. Oil prices are slightly higher with WTI +0.2% to $59.55/bbl. Copper is down 0.1%.

- Later the Fed’s Hammack, Barr, Cook, Goolsbee, Miran and Paulson speak as well as BoE’s Mann and Dhingra. US November 15 jobless claims, delayed September payrolls, November Philly & Kansas Fed Indices, October existing home sales and euro area preliminary November consumer confidence print.

- Bloomberg consensus expects the US unemployment rate to be stable at 4.3% in September, payrolls to rise 51k and average earnings to rise 0.3% m/m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Treasuries Trend Sideways in Lacklustre Trading Day

Having finished the overnight US session modestly higher, US Treasury futures failed to follow on with TYZ5 remaining where it opened at 113-19 and USTs moves modest at best.

- The US 2-Yr did very little during the Asian trading day, trending marginally higher to 3.46%

- The US 5-Yr had finished -2bps lower at 3.57% during the US trading day where it remained.

- The US 10-Yr slipped back below the 4.00% overnight, finishing at 3.98% where it has held during the day today with eyes on it overnight to see if it can consolidate below 4.00%.

- The USD 30-Yr was strong overnight rallying 3bps to 4.57%, and continued on in Asia down again to 4.56% The 30-Yr is now back at levels of April.

The key data releases tonight are the Philadelphia Fed Non-Manufacturing Activity, Redbook retail sales and MBA Mortgage Applications.

JGBS: 10Y Climate Transition Note Greeted With Lacklustre Demand

Japan sold ¥300bn of 10-year climate transition notes at a cut-off yield that was lower than expectations, signalling lacklustre investor demand.

- The cut-off yield was 1.680%, compared with 1.695% estimated by traders in a Bloomberg survey.

- The bid-to-cover ratio was 3.56x, compared with 3.31x in October 2024, the last time the government sold the bonds.

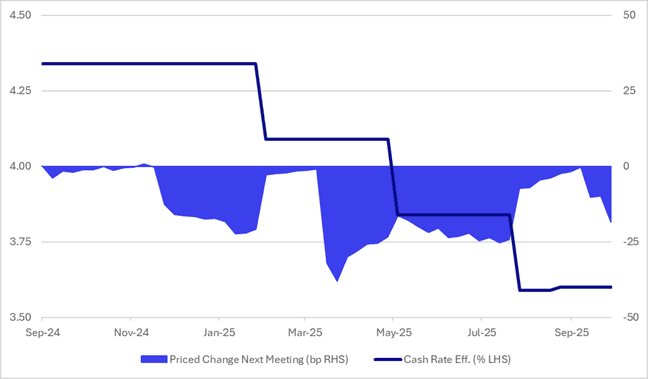

AUSSIE BONDS: Richer But Market Losing Its Conviction About Nov 4 Cut

ACGBs (YM +2.5 & XM +4.0) are stronger and at session highs on another data-light day. The local data calendar remains fairly quiet throughout the week.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session.

- Cash ACGBs are 2bps richer with the AU-US 10-year yield differential at +13bps.

- Today’s ACGB auction of the Jun-54 bond showed strong demand, with the weighted average yield printing 0.92bps through prevailing mids and the cover ratio jumping to 4.0533x from 3.3500x from the previous auction. The strong demand came despite the bond’s outright yield being 20-25bps lower than the previous auction and around 30bps below the peak reached in May.

- The bills strip bull-flattened, with pricing flat to +2.

- Despite firming slightly in recent days, RBA-dated OIS pricing remains 7–13bps softer across meetings compared with pre-jobs data levels last week.

- A 25bp rate cut in November is now assigned a 68% probability (peak 80%, pre-data 38%), with a cumulative 23bps of easing (peak 25bps, pre-data 13bps) priced by year-end.

- Compared with the lead-up to previous cuts in this easing cycle, the market appears less certain than usual about a November 4 move.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI