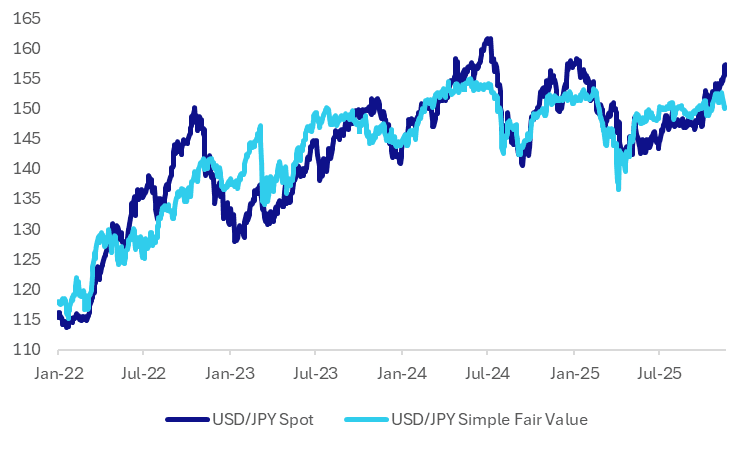

JPY: USD/JPY High Relative To Simple Fair Value, But Short Of Recent Extremes

We saw further jawboning around FX from Japan's Chief Cabinet Minister earlier. Kihara expressed concern around the recent sharp one-sided movements in the exchange rate and noted FX markets should reflect fundamentals. Kihara's comments echo those of other Japan officials recently, which point to increased concern around FX moves, but appear to stop short of warning of imminent intervention (of course for intervention to be successful the authorities arguably wouldn't give strong pre-warning). A simple short term fair value model of USD/JPY suggests current spot levels are getting stretched relative to fair value, but we remain within extremes seen in recent years.

- The chart below plots USD/JPY against the simple fair value estimate, which has two inputs, the US-JP 2yr swap rate differential and global equities. For the past few years this has an R^2 of just over 81%.

- At present the fair value estimate is closer to 150.00 and is diverging in terms of directional trends in spot, as US-JP yield differentials haven't tracked higher, while global equities also saw risk off recently (although that trend is likely to improve post the Nvidia results from this morning.

Fig 1: USD/JPY Spot Versus Simple Fair Value

Source: Bloomberg Finance L.P./MNI

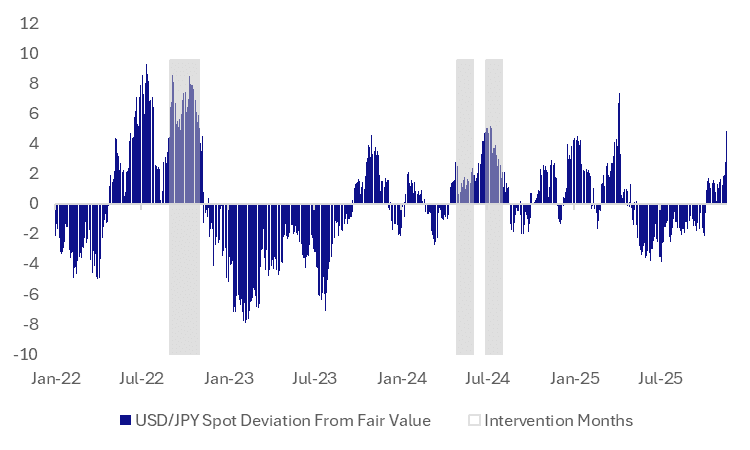

- The second chart below plots deviations in spot and this fair value estimate in percentage terms. The shaded areas indicate intervention months. Positive readings indicate USD/JPY spot is above fair value and vice versa for negative readings. We are currently around 4.8% above fair value. This is elevated but we have seen more extreme episodes in recent years.

- As the shaded areas on the chart indicate, intervention periods are associated with a positive valuation gap, but the thresholds have varied. This makes sense from the perspective that other factors are also in play, such as USD/JPY levels and also rate of change in the pair.

- On the rate of change front, the 1 month USD/JPY gain is around 3.15%, 3 month at 6.75%. Again we are getting more stretched relative to history but remain short of extremes seen in recent years.

- Still if divergences grow with fair value further, particularly if we approach the 160.00 area, market fears around intervention are only likely to become more heightened.

Fig 2: USD/JPY Deviation From Simple Fair Value & Intervention Episodes

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Treasuries Trend Sideways in Lacklustre Trading Day

Having finished the overnight US session modestly higher, US Treasury futures failed to follow on with TYZ5 remaining where it opened at 113-19 and USTs moves modest at best.

- The US 2-Yr did very little during the Asian trading day, trending marginally higher to 3.46%

- The US 5-Yr had finished -2bps lower at 3.57% during the US trading day where it remained.

- The US 10-Yr slipped back below the 4.00% overnight, finishing at 3.98% where it has held during the day today with eyes on it overnight to see if it can consolidate below 4.00%.

- The USD 30-Yr was strong overnight rallying 3bps to 4.57%, and continued on in Asia down again to 4.56% The 30-Yr is now back at levels of April.

The key data releases tonight are the Philadelphia Fed Non-Manufacturing Activity, Redbook retail sales and MBA Mortgage Applications.

JGBS: 10Y Climate Transition Note Greeted With Lacklustre Demand

Japan sold ¥300bn of 10-year climate transition notes at a cut-off yield that was lower than expectations, signalling lacklustre investor demand.

- The cut-off yield was 1.680%, compared with 1.695% estimated by traders in a Bloomberg survey.

- The bid-to-cover ratio was 3.56x, compared with 3.31x in October 2024, the last time the government sold the bonds.

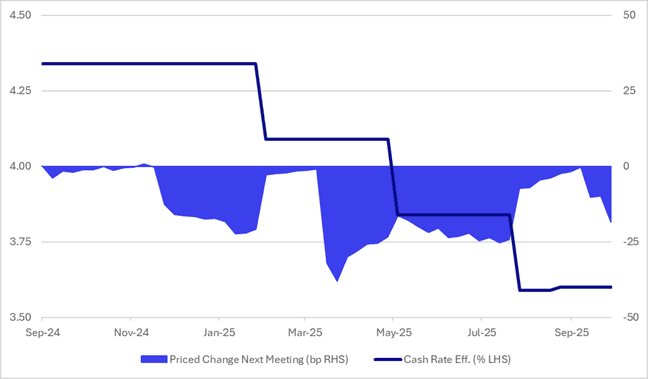

AUSSIE BONDS: Richer But Market Losing Its Conviction About Nov 4 Cut

ACGBs (YM +2.5 & XM +4.0) are stronger and at session highs on another data-light day. The local data calendar remains fairly quiet throughout the week.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session.

- Cash ACGBs are 2bps richer with the AU-US 10-year yield differential at +13bps.

- Today’s ACGB auction of the Jun-54 bond showed strong demand, with the weighted average yield printing 0.92bps through prevailing mids and the cover ratio jumping to 4.0533x from 3.3500x from the previous auction. The strong demand came despite the bond’s outright yield being 20-25bps lower than the previous auction and around 30bps below the peak reached in May.

- The bills strip bull-flattened, with pricing flat to +2.

- Despite firming slightly in recent days, RBA-dated OIS pricing remains 7–13bps softer across meetings compared with pre-jobs data levels last week.

- A 25bp rate cut in November is now assigned a 68% probability (peak 80%, pre-data 38%), with a cumulative 23bps of easing (peak 25bps, pre-data 13bps) priced by year-end.

- Compared with the lead-up to previous cuts in this easing cycle, the market appears less certain than usual about a November 4 move.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI