SOUTH KOREA: 2s10s Curve May Steepen on Issuance Risks

Nov-20 03:24

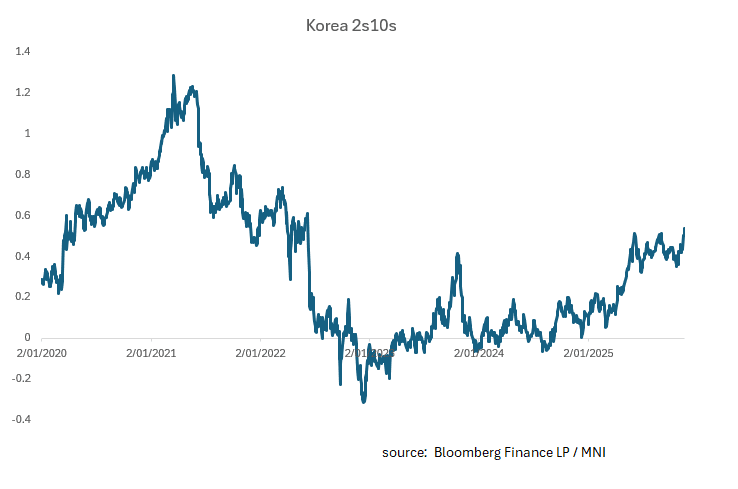

- The steepening of the curve had taken a breather leading up to the October BOK meeting having oscillated around +48 for some time.

- Rates are predominantly on hold due to concerns about the real estate sector, particularly property prices in Seoul. The outlook for growth in Korea is improving given easing trade tensions, but from a low base and may require more support. The projected fiscal deficit of -2.3% of GDP may have some upside risks given the inability to support the economy via rate cuts.

- Current forecasts suggest a mere +1.0% GDP growth for 2025 (rising to 1.9% in 2026) as South Korea’s new government plans a significant increase of its annual budget to revive an economy under pressure from US tariffs, rising welfare costs and an aging population.

- The proposed budget for 2026 is an +8.1% increase and the government plans to issue a record amount of bonds to fund the government spending and will target technology-driven growth, stronger small businesses and more balanced regional development.

- The government has shown a willingness to issue in the 10-Yr part of the curve, to meet the demand from insurance companies.

- In 2020 the COVID impacted budget resulted in a deficit of -2.7% and GDP growth the following year of 4.6%. The deficit for 2024 was -3.3% with a skew towards the back end of the year.

- This suggests there is room for further fiscal expansion and now that the trade deal is finalized, could be a focus for the Lee government.

- Looking back at the post 2020 environment, curves peaked in early 2021 at 1.2% following the impact of various COVID related policies.

- This could suggest potential steepening to occur in KTBs as issuance and growth assumptions are recalibrated.

- Swap markets indicate the BOK on hold for all or most of 2026 suggesting that the bond market may take its guidance from elsewhere meaning an uptick in issuance could see longer bond yields higher whilst the front end remains anchored.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

INDONESIA: MNI BI Preview-Oct 2025: More Cuts To Support Growth

Oct-21 03:11

- Download Full Report Here

- Bank Indonesia stated in September that its decision to cut rates was "consistent with joint efforts to stimulate economic growth", so another 25bp rate cut to 4.5% on 22 October is expected as activity data have softened over the last month.

- Other factors supporting further monetary easing include USDIDR stabilising below 16600 in October, IDR NEER is higher since the September decision, BI’s pro-growth stance, and Fed cuts expected in October and December.

- Also headline and core CPI inflation remain well contained within BI's 1.5-3.5% target band and it expects it to stay there in 2026. However, upside inflation risks could develop given coordinated easing of fiscal and monetary policies.

FOREX: USD Index Drifts Higher Amid Mixed Cross Asset Signals, Yen Underperforms

Oct-21 03:07

The USD is drifting higher against the majors in latest dealings, with yen and NZD underperforming at the margins. Aggregate moves are modest at this stage, with mixed crossed asset trends. The equity backdrop remains supportive, with US equity futures ticking up, while regional Asia Pac markets post strong gains led by the tech side. US Tsy yields are up a touch, but the 10yr is still under 4.00%. Gold is lower, consistent with some USD support.

- The BBDXY index is back up to around 1210, but this is familiar ranges for Oct (earlier highs were just above 1219, while we started the month sub 1200).

- USD/JPY is up a little over 0.20%, to be above 151.10, which is close to Monday intra-session highs (151.20). More meaningful resistance is likely in the 152/153 region, while the bull trigger is at 153.27. Earlier, we had headlines that Satsuki Katayama will be appointed as the new FinMin in Japan, who argued in any interview earlier this year the yen was undervalued. This only provided a modest bounce.

- NZD/USD is lower, but at 0.5730/35, remains within recent ranges, while AUD/USD has softened but remains above 0.6500 at this stage. AUD/JPY is edging back towards recent highs, last 98.35, aiming for an upside 98.50 test. NZD/JPY is near 86.65, just under the 20-day EMA resistance point.

- Earlier data showed from the RBNZ showed Sep credit card spending down 2.1% m/m. We are up modestly in y/y terms, but it continues the patchy path of consumer spending indicators for NZ (with market pricing still biased towards further RBNZ easing as we progress into 2026)

- In the EM Asia space, USD/CNH is back under 7.1200, so outperforming these firmer USD trends, while USD/KRW spot is up 0.25% to 1424, which is in line with yen losses and higher beta FX drifting lower.

JGBS AUCTION: POLL: 10Y CLIMATE BOND

Oct-21 03:05

*JAPAN 10Y CLIMATE BOND SALE MAY HAVE CUT-OFF YIELD 1.695%:POLL - Bloomberg