RBA: RBA Researching Why Inflation & Housing Stronger Than It Expected

Assistant Governor (Economic) Hunter spoke today on RBA research in areas where the transmission of monetary policy may have changed. She said it is looking at if businesses have changed price-setting after Covid, how to estimate capacity and full employment, and if monetary policy transmission channels have changed, given the larger than expected housing response to 2025’s 75bp of easing. The research appears to reflect where the economy has been stronger than the RBA expected, including inflation. This may be another indication that its current pause could be prolonged.

- Q3 CPI printed above the RBA’s August forecasts and Hunter reiterated that the bank was “materially surprised by the latest data” but won’t respond to one month’s outcome. So, it is looking at whether businesses are now faster to pass on cost increases and how their margins change with activity.

- Research is particularly focussed on measuring labour market capacity and Hunter said “we think the labour market is currently a bit tight”, which is not sustainable with the inflation target. This could be a reason for the pickup in core CPI. The October unemployment rate returned to 4.3%.

- They are also looking at the uptrend in women and older people joining the labour force, if people are working less now inflation is lower and if there’s a skills mismatch.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Advisors Share Their Monetary Policy Outlook Ahead Of 5yr Plan

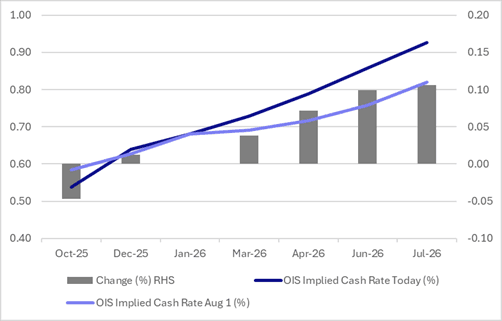

STIR: BoJ Market Pricing: Wait-And-See Approach On Oct 30

BoJ-dated OIS pricing is little changed across 2025 meetings compared to early August levels. Pricing is, however, firmer for 2026 meetings out to July.

- As far as the October 30 meeting is concerned, markets are positioned for a cautious, wait-and-see approach from the BoJ.

- Current OIS pricing implies just a 24% probability of a 25bp hike in October, rising to 65% by December and 82% by January.

- A full 25bp hike is not fully priced until March 2026.

Figure 1: BoJ-Dated OIS – Today Vs. August 1

Source: Bloomberg Finance LP / MNI

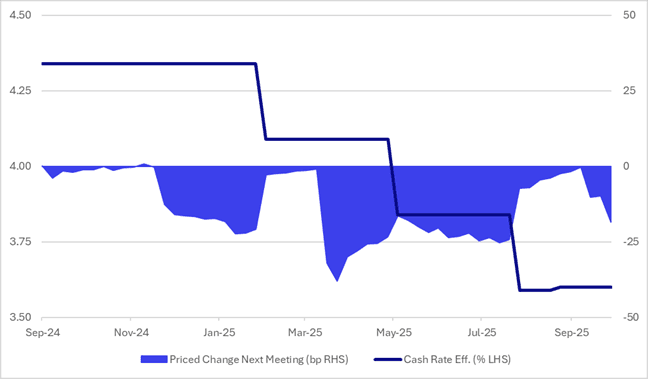

STIR: Market Less Certain Than Normal About Nov 4 Cut By RBA

Despite firming slightly in recent days, RBA-dated OIS pricing remains 7–13bps softer across meetings compared with pre-jobs data levels last week.

- A 25bp rate cut in November is now assigned a 68% probability (peak 80%, pre-data 38%), with a cumulative 23bps of easing (peak 25bps, pre-data 13bps) priced by year-end.

- Compared with the lead-up to previous cuts in this easing cycle, the market appears less certain than usual about a November 4 move.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI