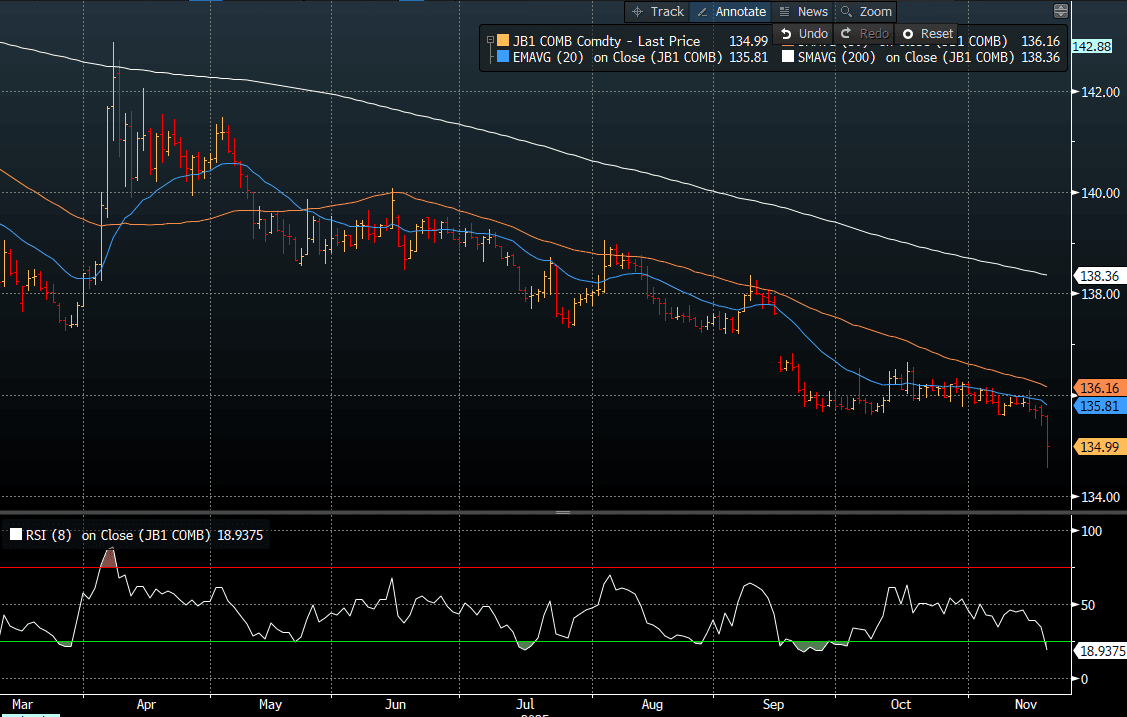

JGBS: Yields Explode Higher As Fiscal Fears Drive Positioning Change

JGB futures are trading sharply weaker at 134.99, -62 compared to settlement levels, albeit well above the session low of 134.56. (see chart)

- MNI’s technical analysts had viewed fresh cycle lows as confirmation of the downtrend that had dominated prices since mid-September. Their Fibonacci projection of 134.69 was hit today.

- “The Japanese government is making final arrangements to compile an economic stimulus package of ~21.3t yen, public broadcaster NHK reports, citing an unidentified person.” - BBG

- "Major investors, including domestic banks, insurers, and overseas accounts, collectively pared net purchases of 10-year JGBs to the lowest since October 2023, according to the latest Japan Securities Dealers Association data. In contrast, demand remained firm for 2- to 5-year notes, while super-long bonds also continued to see modest net buying." – BBG

- BoJ Koeda's speech appeared to be in line with recent rhetoric from key BoJ board members. There were some hawkish undertones, although she didn't give any hints on rate hike timing.

- Cash JGBs are off worst levels but remain 2-7bps cheaper across benchmarks. The 10-year yield is currently at 1.813% versus a session high of 1.845%.

- Tomorrow’s local calendar will see National CPI, Trade Balance and S&P Global PMI(P) data alongside an Enhanced Liquidity Auction for 1-5-year JGBs.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURUSD TECHS: Trading Above Last Week’s Low

- RES 4: 1.1919 High Sep 17 and a bull trigger

- RES 3: 1.1820 High Sep 23

- RES 2: 1.1775 61.8% retracement of the Sep 17 - Oct 9 bear leg

- RES 1: 1.1730 50.0% retracement of the Sep 17 - Oct 9 bear leg

- PRICE: 1.1635 @ 06:01 BST Oct 21

- SUP 1: 1.1602/1542 Low Oct 9 and the bear trigger

- SUP 2: 1.1516 76.4% retracement of the Aug 1 - Sep 17 bull leg

- SUP 3: 1.1392 Low Aug 1 and bear trigger

- SUP 4: 1.1313 Low May 30

The latest recovery in EURUSD signals a potential reversal and undermines a recent bearish theme, suggesting the corrective cycle between Sep 17 - Oct 9, may be over. Note that moving average studies are in a bull-mode position - for now - highlighting a dominant medium-term uptrend. A resumption of gains would open 1.1775 next, a Fibonacci retracement. Key support and the bear trigger lies at 1.1542, the Oct 9 low.

BUND TECHS: (Z5) Corrective Pullback

- RES 4: 130.99 76.4% retracement of Jun 13 - Sep 25 bear leg (cont)

- RES 3: 130.80 High Jun 13 and key resistance

- RES 2: 130.63 1.500 proj of the Sep 3 - 10 - 25 price swing

- RES 1: 130.59 High Oct 17

- PRICE: 130.00 @ 05:39 BST Oct 21

- SUP 1: 129.68/129.44 Low Oct 15 / High Sep 10

- SUP 2: 129.20 20-day EMA

- SUP 3: 128.86 50-day EMA

- SUP 4: 128.25 Low Oct 7

Bund futures continue to trade below last week’s high, however, a bull cycle remains intact. The impulsive nature of the latest rally and a fresh cycle high on Friday, paves the way for a test of the next key resistance 130.80, the Jun 13 high. Clearance of this level would strengthen the bullish condition. Note that the contract is overbought, a deeper pullback would allow this condition to unwind. Initial key support is 129.20, the 20-day EMA.

GOLD: Gold & Silver Fall As Equities & US Dollar Strengthen, Focus Remains On US

Gold has stabilised today during the APAC session after rising 2.5% on Monday. Prices rose to $4375.38/oz and then fell to $4332.95 and are now down 0.4% to $4340.5. Equities are rallying and the US dollar is slightly stronger (BBDXY +0.1%) but the factors bullion ignored yesterday may have also contributed to the pause in the rally. It is in overbought territory, 2025 Fed easing is already priced in, there is talk that the US government shutdown could end this week and US-China trade tensions appear to have eased.

- Both gold and silver continue to hold well above initial support levels of $4140.8, 15 October low, and $48.736, 20-day EMA, respectively.

- The 1 November deadline for a US-China trade deal remains but President Trump said that the US will “be fine” with China. Economic Council Director Hassett also gave indications that the government shutdown could conclude this week.

- Silver is down 1.1% to $51.87 after falling to $51.607. It is a smaller market than gold and so moves tend to be amplified. It is also signalling that it is overbought.

- Equities are stronger across the region with the Hang Seng up 1.7% and ASX +0.7% but the S&P e-mini is flat. Oil prices are lower with WTI -0.3% to $56.84/bbl. Copper is 0.2% higher.

- Later US October Philly Fed non-manufacturing and September Canadian CPI print. ECB President Lagarde and Board member Lane speak.