GLOBAL MACRO: Data Point To Robust Global Export Volumes

Shipping companies reported Q3 volumes were strong in line with CPB data showing higher monthly global export volumes in July and August. There had been fears for global trade following the announcement of US reciprocal tariffs in April but it appears to have been more resilient with it up 3.7% y/y in August. After frontloading of shipments to the US in H1, container rates fell from July but have risen sharply in November to date, possibly a sign of continued solid export volumes.

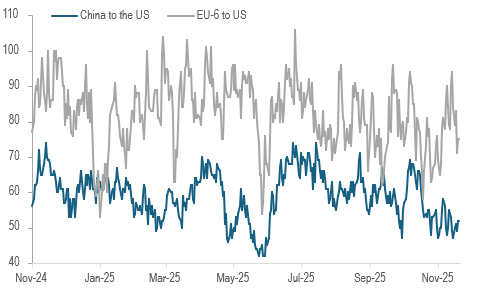

- After rising over H1, departures to the US have normalised over H2 with only those from the EU-6 below the pre-February 2025 average with major Asian shippers all now around their averages, according to Bloomberg’s container ship count.

- Departures from China peaked in July and trended lower thereafter but then took a sharp turn down from mid-October coinciding with the latest US-China trade dispute centred around rare earths. Presidents Trump and Xi met on 31 October and came to an agreement on many issues and as a result ships leaving China for the US tentatively appear to have increased again and are around average.

Bloomberg container ship count

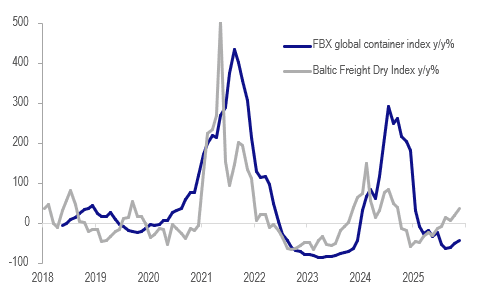

- FBX global container rates fell each month from July but are up 21.3% m/m in November, possibly signalling tighter capacity. They are still down 41.9% y/y but off the 60% y/y decline in September. Rates on the China-East Asia to east coast North America route have also been weak but outperformed the global aggregate and to the Mediterranean.

- There have been reports of tanker shortages pushing up rates for oil and LNG given the current record amount of seaborne crude. Bulk rates are also higher with the Baltic Freight Index up 7.5% m/m in November to be up almost 40% y/y.

Global shipping rates y/y%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Closed Richer, NZ-US 10Y Diff Rich Vs. FV

NZGBs closed at or near session highs, 4bps richer across benchmarks.

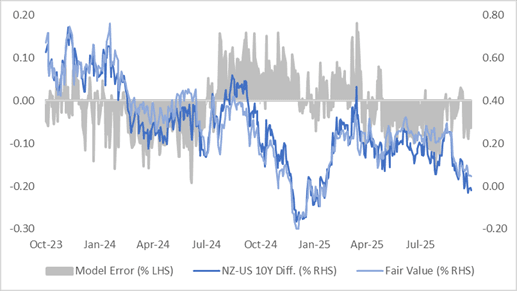

- The NZ-US 10-year yield differential is approximately -2bps. However, a simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the current differential is 6bps too low versus FV. (see chart)

- Export growth is a bright spot in the NZ economy, which was up 19% y/y in September after 21% y/y. The strength is being driven by higher dairy prices but also an increase in milk & cheese export volumes.

- Credit card spending in New Zealand decreased by 2.1% month on month to NZ$4.34 billion in September after a 2% increase in August, while credit card balances fell 0.1% to NZ$6.06 billion in September, following a 0.7% rise in the previous month. - MTN

- RBNZ dated OIS pricing closed little changed across meetings. 26bps of easing is priced for November, with a cumulative 36bps by February 2026.

- The local calendar will be empty until next Tuesday’s release of Filled Jobs data for September.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 5.00% May-54 bond.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

INDONESIA: MNI BI Preview-Oct 2025: More Cuts To Support Growth

- Download Full Report Here

- Bank Indonesia stated in September that its decision to cut rates was "consistent with joint efforts to stimulate economic growth", so another 25bp rate cut to 4.5% on 22 October is expected as activity data have softened over the last month.

- Other factors supporting further monetary easing include USDIDR stabilising below 16600 in October, IDR NEER is higher since the September decision, BI’s pro-growth stance, and Fed cuts expected in October and December.

- Also headline and core CPI inflation remain well contained within BI's 1.5-3.5% target band and it expects it to stay there in 2026. However, upside inflation risks could develop given coordinated easing of fiscal and monetary policies.

FOREX: USD Index Drifts Higher Amid Mixed Cross Asset Signals, Yen Underperforms

The USD is drifting higher against the majors in latest dealings, with yen and NZD underperforming at the margins. Aggregate moves are modest at this stage, with mixed crossed asset trends. The equity backdrop remains supportive, with US equity futures ticking up, while regional Asia Pac markets post strong gains led by the tech side. US Tsy yields are up a touch, but the 10yr is still under 4.00%. Gold is lower, consistent with some USD support.

- The BBDXY index is back up to around 1210, but this is familiar ranges for Oct (earlier highs were just above 1219, while we started the month sub 1200).

- USD/JPY is up a little over 0.20%, to be above 151.10, which is close to Monday intra-session highs (151.20). More meaningful resistance is likely in the 152/153 region, while the bull trigger is at 153.27. Earlier, we had headlines that Satsuki Katayama will be appointed as the new FinMin in Japan, who argued in any interview earlier this year the yen was undervalued. This only provided a modest bounce.

- NZD/USD is lower, but at 0.5730/35, remains within recent ranges, while AUD/USD has softened but remains above 0.6500 at this stage. AUD/JPY is edging back towards recent highs, last 98.35, aiming for an upside 98.50 test. NZD/JPY is near 86.65, just under the 20-day EMA resistance point.

- Earlier data showed from the RBNZ showed Sep credit card spending down 2.1% m/m. We are up modestly in y/y terms, but it continues the patchy path of consumer spending indicators for NZ (with market pricing still biased towards further RBNZ easing as we progress into 2026)

- In the EM Asia space, USD/CNH is back under 7.1200, so outperforming these firmer USD trends, while USD/KRW spot is up 0.25% to 1424, which is in line with yen losses and higher beta FX drifting lower.