MNI US OPEN - UK Budget the Biggest Domestic Risk Event of '25

EXECUTIVE SUMMARY

- MNI UK BUDGET PREVIEW: ROUND 2, WILL THERE BE A KNOCKOUT?

- RBNZ MAINTAIN EASING BIAS, BUT 2026 HOLD LIKELY

- BOJ PREPS MARKETS FOR NEAR-TERM HIKE – RTRS

- AUSTRALIA HEADLINE CPI INFLATION RISES 3.8% Y/Y, ABOVE EXPECTATIONS

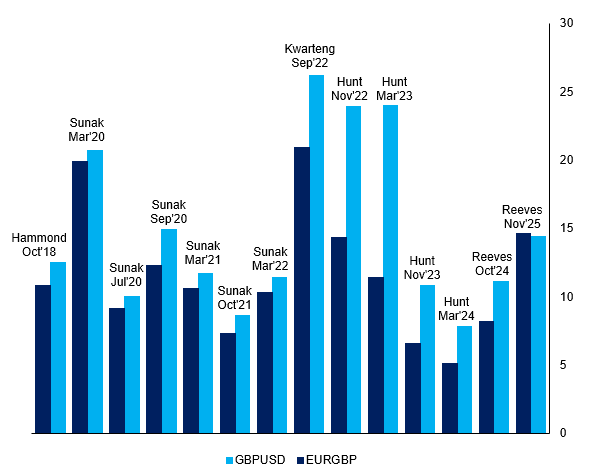

Figure 1: Prevailing implied vols ahead of UK Budget events

Source: MNI, Bloomberg Finance L.P.

NEWS

MNI UK BUDGET PREVIEW: Round 2, Will There Be A Knockout?

It can be stated without hyperbole that the UK Budget could be the biggest domestic event of the year, and indeed could have repercussions for many years to come. There is still a great deal of uncertainty over the measures that will be announced. In this document we answer the main questions of why the Budget is so important for financial markets and political risk, outline potential measures and also set out expectations for the gilt remit revision. Additionally, we look at how at next year's Budget there will be a little more wiggle room, which may impact Reeves' headroom choice for this year.

UK (MNI): Minimum Wage Increase in Line With Expectations (And Sugar Tax)

The National Living Wage (which applies to those aged 21+) was confirmed by the government last night at 18:00GMT and was fully in line with expectations. It will rise from GBP12.21 per hour to GBP12.71 (a 4.1% increase) from April 2026. We think that the wage increases are close enough to expectations to not have had any impact on either MPC members, the probability of cuts or market views. Yesterday also saw reports that the sugar tax would be extended to pre-packaged milk-based drinks (milkshakes, lattees etc) but would not apply to drinks prepared in cafes or coffee shops.

RBNZ (MNI): Easing Bias Maintained, But 2026 Hold Likely

The Reserve Bank of New Zealand maintained a slight easing bias at its November meeting after a widely-expected 25-basis-point cut, despite the largely hawkish tone of its latest Monetary Policy Statement, with acting Governor Christian Hawkesby noting that the Bank’s updated forecasts show a modest preference for a further rate cut. The decision was reached by a five–one vote after a discussion that included holding the rate.

US (BBG): Hassett Says He Would Agree to Be Fed Chair If Asked

National Economic Council director Kevin Hassett will say “yes” if asked to be Fed Chair, he says in an interview on Fox News. “I want to serve my country and I want to serve my president. But you know, we’ll see how it goes. There are a lot of great candidates,” Hassett says.

US (WSJ): U.S. Negotiates Lower Prices for Ozempic and 14 Other Drugs

The U.S. government negotiated lower prices in the federal Medicare program for 15 high-selling medicines including Ozempic, widening an effort to rein in drug costs. The new prices, which will take effect in 2027, shave 38% to 85% off the list prices for drugs for diseases including asthma, cancer and diabetes. The reductions are estimated to save Medicare, the health-insurance program for the elderly, $12 billion.

US/CHINA (BBG): Trump Says Xi ‘Pretty Much’ Agreed to Expand Agricultural Buys

US President Donald Trump said he urged Chinese President Xi Jinping to increase the speed and size of agricultural purchases and said Beijing had “more or less agreed” to do so. “I think he’s going to very much surprise you on the upside,” Trump told reporters aboard Air Force One on Tuesday. “I think he’s going to — I asked him, ‘I’d like you to buy a little faster, I’d like you to buy a little more.’ And he’s more or less agreed to do that.”

US/RUSSIA (MNI): Putin Aide Ushakov Talks on Peace Plan After Leak of Witkoff Call

Russian state-run Tass reports comments from Assistant to the President for Foreign Policy Yuri Ushakov. Says that "representatives of the Russian and Ukrainian intelligence services are discussing sensitive issues in the UAE", but that "The US peace plan for Ukraine was not discussed in Abu Dhabi". Says Russia has not officially received the US peace plan, and has not yet discussed the details with anyone. However, Russia has "unofficially received several versions" of the peace plan and is in contact with the US on the issue. Ushakov says, "Russia views some aspects of the US peace plan positively."

EU/RUSSIA (MNI): FMs Hold Call on Peace Deal; Merz Says Use Frozen Russian Assets

European Commission President Ursula von der Leyen has been addressing the European Parliament on the draft Ukraine peace deals being negotiated. Says that the EU welcomes Trump's efforts to seek peace. Says "much more effort is needed, but we have a starting point". VdL: "Any agreement should deliver a just and lasting peace, and it should ensure real security for Ukraine and Europe." VdL: "If today we legitimise and formalise the undermining of borders, we open the doors for more wars tomorrow."

EUROZONE (MNI): EZ Banks Resilient, Multiple Risks Linger - ECB

Banks across the eurozone remain resilient, with strong profitability and ample capital and liquidity buffers, but remaining uncertainties around trade agreements and the longer-term economic and financial effects of tariffs "continue to shape the financial stability landscape," according to the European Central Bank's November Financial Stability Review published on Wednesday. “Measures of trade policy uncertainty have eased notably from their April highs, but uncertainty continues to linger, with potential for renewed spikes,” ECB Vice-President Luis de Guindos said in the introduction.

GERMANY (BBG): Germany Risks Growth Undershoot Without Reforms, IMF Warns

Germany is in danger of underperforming on growth and faces a longer-term struggle to achieve meaningful expansion unless it pursues “bold” reforms, according to the International Monetary Fund. The Washington-based fund, in its annual Article IV report on the country released on Wednesday, predicted gross domestic product will rise 1% next year — up slightly from its World Economic Outlook in October — and forecast an acceleration to 1.5% in 2027. But it warned that “risks to the outlook are tilted to the downside.”

BOJ (RTRS): BOJ Preps Markets for Near-Term Hike as Weak Yen Overshadows Politics

The Bank of Japan is preparing markets for a possible interest rate hike as soon as next month, sources say, reviving previous hawkish language as worries about sharp yen declines return and political pressure for the bank to keep rates low fades. A change in BOJ messaging over the past week has shifted focus back to inflationary risks of a weak yen from earlier worries about the U.S. economy, comments aimed at reminding markets a December rate hike was still a prospect, two people familiar with the bank's thinking told Reuters.

BOJ (MNI INTERVIEW): Yen to Drive BOJ's Dec Hike Decision - Momma

A former BOJ chief economist shares his policy rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

BOJ (MNI): BOJ’s JGB Unrealized Loss Rises to JPY32.8 Tlrn

The Bank of Japan posted JPY32.8 trillion in unrealized losses on Japanese government bonds (JGBs) at the end of September, up from JPY28.6 trillion at the end of March, following the rise in JGB yields, according to the BOJ’s half-year earnings report released Wednesday. The BOJ’s exchange-traded fund (ETF) holdings remained unchanged at JPY37.1 trillion from March, with unrealized profits rising to JPY46.0 trillion from JPY32.9 trillion in the same period.

JAPAN (MNI): Japan Govt Keeps Economic View; Lowers Imports

Japan’s government left its overall economic assessment unchanged for the third consecutive month but lowered its view on imports for the first time since February 2025, the Cabinet Office said on Wednesday. Assessments of other components, including exports, capital investment, production, and private consumption, remained unchanged. The government also adjusted its view on corporate goods prices without specifying an upward or downward revision.

S.KOREA (BBG): South Korea Closely Monitoring Speculative, One-Sided Won Moves

South Korea’s finance minister said authorities are closely monitoring any speculative, one-sided currency moves, underscoring the country’s readiness to act as the won trades near a seven-month low. Fresh off a plane back from the G20 summit in South Africa, Finance Minister Koo Yun Cheol on Wednesday said officials will “sternly respond if foreign-exchange volatility excessively widens,” without elaborating on the measures.

CHINA (MNI EXCLUSIVE): China to Front Load CNY2 Trillion of 2026 Bonds

Advisors share their outlook for China bond issuance into 2026. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

CHINA (MNI EXCLUSIVE): China's Private Investment Support Faces Local Challenges

Advisors share their outlook for private investment in China. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

DATA

GERMANY DATA (MNI): IFO Employment Barometer Suggests Further Labour Market Softness

The IFO employment barometer fell in November, to 92.5 points, matching September's lowest level since June 2020. "Many companies are continuing to cut jobs [...] Due to the stuttering economy, the labor market trend remains weak", IFO comments. The deterioration was quite broad based this time, with industry, trade and services sectors all down. The industry reading sits at -20.9, slightly above the -22.0 cycle low seen at the beginning of this year.

NORWAY DATA (MNI): Weaker Than Expected Q3 Mainland GDP Will Feed Into Dec Rate Path

Norwegian Q3 mainland GDP was weaker than expected. All else equal, this will have a dovish impact on the domestic demand component of the December MPR rate path. A cut in December still seems unlikely, particularly after the higher-than-expected October inflation report, but the pace and magnitude of easing next year remains uncertain. Upcoming labour market data, the November inflation report and the Q4 Regional Network Survey are the last key inputs to monitor before the December 18 decision.

NORWAY DATA (MNI): Pay Pressures Are Decelerating, But Possibly Not Fast Enough

Whole economy pay metrics eased in Q3, but 4Q/4Q measures of wages and salaries and compensation of employees remain above Norges Bank's 4.7% September MPR projection. Firm wage growth has contributed to sticky inflationary pressures, and Norges Bank are sensitive to upside surprises. The annual earnings growth series will be available alongside the Q4 national accounts in February, which will allow the cleanest comparison with Norges Bank projections - other metrics we track aren't perfect substitutes for this data.

MNI CHINA MONEY MARKET INDEX: Rate Cut Expectations Fall

- MNI CHINA MMI NOV CURRENT LQDTY CONDITIONS 21.0 VS OCT 27.6

- MNI CHINA MONEY MKT INDEX NOV LQDTY OUTLOOK 51.0 VS OCT 49.0

- MNI CHINA MMI ECONOMIC CONDITIONS NOV 28.0 VS OCT 30.6

MNI (Beijing) Chinese interbank traders have reduced expectations for further rate cuts in 2025, but believe the central bank will increase bond purchases to meet end-of-year liquidity demand, MNI’s China Money Market Index indicated on Wednesday. The PBOC seven-day reverse repo rate outlook sub-index fell to 59.0, with 82% of participants expecting a steady policy rate in the coming month.

JAPAN DATA (MNI): Japan Oct Trimmed Mean Rises 10bp to 2.2%

Japan’s trimmed mean measure of underlying inflation rose 2.2% y/y in October, up from 2.1% in September, remaining above the Bank of Japan’s 2% target for a 10th consecutive month, BOJ data showed Tuesday. The increase signals continued pass-through of cost pressures stemming from elevated labour costs. The release follows Friday’s CPI report showing core inflation at 3.0% y/y in October, accelerating from 2.9% in September and exceeding the 2% target for the 43rd straight month. The mode of the inflation distribution rose to 1.5% from 1.4%.

JAPAN DATA (MNI): Japan Oct Services PPI Rises 2.7% vs. Sept +3.1%

- JAPAN OCT SERVICES PPI +2.7% Y/Y; SEPT REV +3.1%

- JAPAN OCT SERVICES PPI +0.6% M/M: SEPT UNREV +0.1%

Japan’s services producer price index rose 2.7% y/y in October, slowing from a revised 3.1% in September, indicating that corporate pass-through of cost increases continued but at a moderating pace, preliminary Bank of Japan data showed Wednesday. The October reading was weighed down by transportation and postal services (2.0% vs 3.6%) and advertising services (-0.4% vs 2.7%), while gains in other categories, including hotels (18.1% vs 11.1%), provided support. On a monthly basis, the SPPI rose 0.6% in October after a 0.1% increase in September.

AUSTRALIA DATA (MNI): Aussie Oct CPI at 3.8%, Trimmed 3.3%

Headline inflation rose 3.8% y/y in October, 20bp above expectations, while trimmed mean inflation increased by 30bp more than anticipated to 3.3% y/y, according to the first release of the complete Monthly Consumer Price Index by the Australian Bureau of Statistics. Housing remained the largest contributor to annual inflation, rising 5.9%. This was followed by food and non-alcoholic beverages, and recreation, and culture, both up 3.2%.

FOREX: NZD Outperforms Post RBNZ, Two-Sided Risks for GBP Into Budget

- NZD is the outperformer today after RBNZ guidance amid their 25bp cut signals a likely hold through H1 next year. This led NZDUSD to see session highs of 0.5697, breaking above its 20-day EMA. This signals scope for a stronger recovery to 0.5725, which represents both the 50-day and prior trendline support turned resistance. 0.5800 remains a key medium-term pivot.

- AUDNZD meanwhile saw downside following the RBNZ meeting, despite the new monthly Australian CPI coming in firmer than expected. The cross overnight saw its lowest levels this month at 1.1407, with the 50-day EMA providing initial support at 1.1391.

- Dollar weakness and further hawkish BOJ reports prompted USDJPY to print a 155.65 pullback low overnight. With dips remaining very well supported, the pair has firmed since, recovering to 156.40 at typing. A break above the 157.89 November 20 high would signal scope for an extension of the current uptrend.

- GBPUSD still sees notable two-way risk headed into today's Budget - despite trickling details of policy measures across the UK press this morning. This week's spot recovery works against the bearish trend theme, which would resume on a break below 1.3010, the Nov 4 / 5 low, but we also see positioning dynamics possibly creating room for a GBP squeeze, raising the risk of a stronger recovery given the amount of Budget scrutiny the currency has been under this month.

- We still see scope for market surprises, with key uncertainties remaining over headline changes in tax, disinflationary measures, fiscal headroom and scope for Gilt sales. Key resistance meanwhile stands at 1.3261, the 50-day EMA. A clear break of this hurdle would highlight a potential reversal.

- Aside from the UK budget, US MBA mortgage applications, weekly claims, September durable goods orders, MNI Chicago PMI, and the Fed Beige Book are on the calendar.

EGBS: German 5s30s Curve Taking Cues From Global Peers

The German 5s30s curve has marginally steepened, seemingly spillover from yesterday/this morning’s moves in US Treasuries and Gilts. Today’s regional calendar is light, with focus on any spillover from the UK budget. Zooming out, details of Germany's 2026 issuance plan could be a catalyst for 5s30s to stage a retest of YTD highs of 111bps, but recent commentary from the debt office suggests long-end term premium will be taken into account when determining the maturity structure of future debt sales. 5s30s is up 1bp today to 103.7b, with the curve twist steepening.

- Results from today’s E3bln 2.60% Aug-35 Bund auction were stronger than the October sale, following on from yesterday’s improved Bobl auction.

- Bund futures are -3 ticks at 129.08. Initial resistance is yesterday’s 129.16 high. Short-term gains in Bund futures appear corrective - for now.

- 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s closing levels. A rise in global equity futures yesterday drove modest tightening across the space.

- The ECB’s Financial Stability Report noted that market concerns about stretched public finances in some advanced economies may create strains in global bond markets which could affect euro area financial stability through shifts in international capital flows and currency swings.

GILTS: Off Lows on Cross-Asset Moves, Budget Set to Dominate

Gilts have recovered from early session lows, with a pullback from session highs in equities providing some stability for bonds.

- Improved risk sentiment, in the wake of the latest speculation surrounding the next Fed Chair and an impending visit of U.S. envoy Witkoff to Russia, provided the initial pressure for gilts. Decreased liquidity ahead of the Budget may have also factored in.

- Chancellor Reeves will deliver the Budget around ~12:30 London.

- H6 futures -13 at 91.08 vs. lows of 90.79. Initial support and resistance 90.53 and 91.26. Yesterday’s rally undermined the recent bearish move.

- Yields ~1bp lower to ~2bp higher, curve steeper.

- 2s10s ~74bp after the recent pullback from 80bp.

- 5s30s ~141bp after the spread failed to close above 145bp last week.

- Gilt/Bunds little changed at 182bp, comfortably within the recent ~170-190bp range.

- 30-Year swap spreads have retraced 4bp of the 6bp of narrowing triggered by increases in fiscal and political risk premia over the past couple of weeks.

- As noted in recent bullets, we believe that under-delivery at today’s Budget presents the greatest risk to current market pricing.

- Questions surrounding fiscal credibility following the event would risk fresh curve steepening, swap spread narrowing and gilt widening vs. Bunds.

- Our full Budget preview can be found here.

- While our latest Gilt Week Ahead outlines the key metrics that we are looking at ahead of the event.

EQUITIES: E-Mini S&P Extends Recovery From Nov 21 Low

A bearish theme in Eurostoxx 50 futures remains present following recent weakness. However, the contract has traded above the 50-day EMA, at 5595.08, and pierced the 20-day EMA, at 5620.85. A clear break of both averages would highlight a possible reversal and signal scope for a stronger recovery. This would open 5691.30, a Fibonacci retracement point. Key short-term support and the bear trigger is at 5475.00, the Nov 21 low. S&P E-Minis are trading higher as the contract extends the recovery from the Nov 21 low. The climb has resulted in a breach of the 20- and 50- day EMAs. This highlights a bullish development and the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would signal scope for a climb towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support has been defined at 6525.00, the Nov 21 low.

- Japan's NIKKEI closed higher by 899.55 pts or +1.85% at 49559.07 and the TOPIX ended 64.61 pts higher or +1.96% at 3355.5.

- Elsewhere, in China the SHANGHAI closed lower by 5.839 pts or -0.15% at 3864.184 and the HANG SENG ended 33.53 pts higher or +0.13% at 25928.08.

- Across Europe, Germany's DAX trades higher by 54.12 pts or +0.23% at 23519.67, FTSE 100 higher by 20.6 pts or +0.21% at 9630.75, CAC 40 up 26.1 pts or +0.33% at 8051.9 and Euro Stoxx 50 up 28.58 pts or +0.51% at 5602.49.

- Dow Jones mini up 105 pts or +0.22% at 47287, S&P 500 mini up 17.25 pts or +0.25% at 6799, NASDAQ mini up 77.5 pts or +0.31% at 25163.25.

Time: 10:00 GMT

COMMODITIES: WTI Futures Bear Trigger in Focus Following Recent Weakness

Recent weakness in WTI futures highlights a bearish theme. A stronger resumption of the bear leg would pave the way for a move towards key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction. The trend condition in Gold remains bullish and the bear phase between Oct 20 and 28 appears to have been a correction. This allowed a recent overbought condition to unwind. Key support to watch lies at the 50-day EMA, at $3966.8. Clearance of this EMA would signal scope for a deeper retracement. The first short-term bull trigger has been defined at $4245.23, the Nov 13 high.

- WTI Crude up $0.05 or +0.09% at $58.01

- Natural Gas up $0.04 or +0.96% at $4.525

- Gold spot up $31.17 or +0.75% at $4160.9

- Copper up $7.95 or +1.56% at $516.6

- Silver up $0.82 or +1.6% at $52.2788

- Platinum up $12.61 or +0.81% at $1565.36

Time: 10:00 GMT

| Date | GMT/Local | Impact | Country | Event |

| 26/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 26/11/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 26/11/2025 | 1230/1230 | Chancellor Reeves to deliver UK Budget | ||

| 26/11/2025 | 1330/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 26/11/2025 | 1442/0942 | *** | MNI Chicago PMI | |

| 26/11/2025 | 1500/1000 | * | US Bill 08 Week Treasury Auction Result | |

| 26/11/2025 | 1500/1000 | ** | US Bill 04 Week Treasury Auction Result | |

| 26/11/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 26/11/2025 | 1530/1530 | DMO to publish consultation agenda | ||

| 26/11/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 26/11/2025 | 1605/1705 | ECB Lane Fireside Chat on Macro Outlook | ||

| 26/11/2025 | 1630/1130 | ** | US Treasury Auction Result for 7 Year Note | |

| 26/11/2025 | 1700/1200 | ** | Natural Gas Stocks | |

| 26/11/2025 | 1700/1800 | ECB Lagarde Acceptance Speech | ||

| 26/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/11/2025 | 1900/1400 | Fed Beige Book | ||

| 27/11/2025 | 0030/1130 | * | Private New Capex and Expected Expenditure | |

| 27/11/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 27/11/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 27/11/2025 | 0830/0930 | ECB Cipollone Remarks at Euro Cyber Resilience Board | ||

| 27/11/2025 | 0900/1000 | ** | M3 | |

| 27/11/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 27/11/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 27/11/2025 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 27/11/2025 | 1100/1200 | ECB de Guindos Remarks at CEDE Congress of Executives | ||

| 27/11/2025 | 1330/0830 | * | Current Account | |

| 27/11/2025 | 1330/0830 | * | Payroll Employment | |

| 27/11/2025 | 1630/1630 | BOE Greene Speech at Goodbody Conference | ||

| 28/11/2025 | 2330/0830 | ** | Tokyo CPI | |

| 28/11/2025 | 2330/0830 | * | Labor Force Survey | |

| 28/11/2025 | 2350/0850 | * | Retail Sales (p) | |

| 28/11/2025 | 2350/0850 | ** | Industrial Production |