EGBS: German 5s30s Curve Taking Cues From Global Peers

Nov-26 10:43

The German 5s30s curve has marginally steepened, seemingly spillover from yesterday/this morning’s moves in US Treasuries and Gilts. Today’s regional calendar is light, with focus on any spillover from the UK budget. Zooming out, details of Germany's 2026 issuance plan could be a catalyst for 5s30s to stage a retest of YTD highs of 111bps, but recent commentary from the debt office suggests long-end term premium will be taken into account when determining the maturity structure of future debt sales. 5s30s is up 1bp today to 103.7b, with the curve twist steepening.

- Results from today’s E3bln 2.60% Aug-35 Bund auction were stronger than the October sale, following on from yesterday’s improved Bobl auction.

- Bund futures are -3 ticks at 129.08. Initial resistance is yesterday’s 129.16 high. Short-term gains in Bund futures appear corrective - for now.

- 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s closing levels. A rise in global equity futures yesterday drove modest tightening across the space.

- The ECB’s Financial Stability Report noted that market concerns about stretched public finances in some advanced economies may create strains in global bond markets which could affect euro area financial stability through shifts in international capital flows and currency swings.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SCHATZ: Block trade

Oct-27 10:42

Schatz Block trade, suggest seller:

- DUZ5 ~10.8k at 107.07.

FOREX: USDJPY Looks to Extend Winning Streak as Fed/BOJ Meetings Near

Oct-27 10:31

- Both higher bond yields and equities initially provided a positive impulse for USDJPY on Monday, taking the pair up to 153.26 highs ahead of the European open. Japan officials noted they were monitoring FX markets for disorderly moves, and although USDJPY has reverted back below the 153.00 handle, the remarks didn't suggest intervention risks had risen for now.

- Notably, the overnight peak came within one pip of 153.27, the Oct 10 high and a bull trigger. Clearance of this hurdle would confirm a resumption of the medium-term uptrend and will be eagerly monitored as we approach this week’s Fed and BOJ meetings. While the bar for a surprise on either rate decision is extremely high, each committee’s rhetoric will be key in shaping the policy outlook in coming months, especially given the dissenting votes both boards have had at prior meetings.

- Markets will be looking for signs of a significant hawkish turn from the BOJ, and if more of the committee join Takata in their view that now is a prime opportunity to raise the policy rate. Takata recently added the BOJ's "tankan" business survey in October and findings from its branch managers suggest improvements in job and income conditions are underpinning consumption.

- SocGen have said the yen is being sold as much because the $/Y correlation with bond yields has broken down. They believe momentum is dominating the price action at the moment and month-end flows may be all that is holding the market back from a push back to 150.

- Market participants will be well aware that the politically driven gap at the start of the month would require a move to 147.47 to be filled. The first important support to watch lies at 150.90, the 20-day EMA.

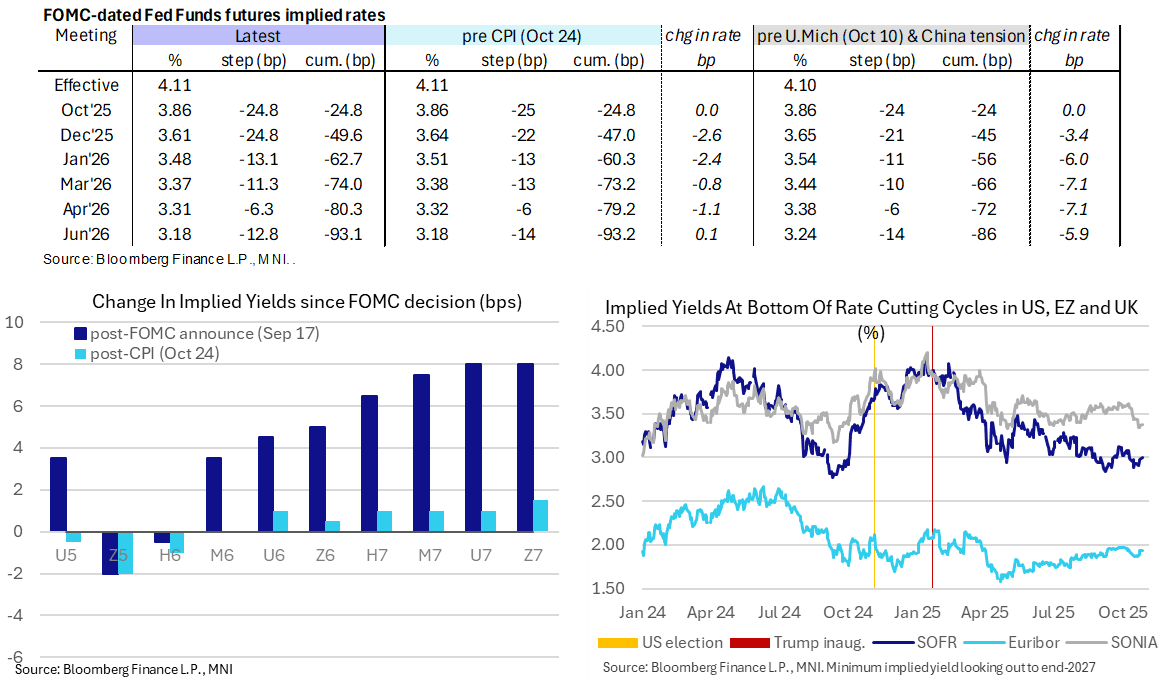

STIR: US-China Trade Deal Optimism Limits Dovish CPI Impact

Oct-27 10:31

- US-China trade deal optimism ahead of Trump-Xi meeting this week sees Fed Funds implied rates 1-2bp higher since Friday’s close, Wednesday’s decision aside where the Fed is still fully priced to cut 25bps.

- It’s seen these nearer term meetings reverse a large part of the dovish reaction to Friday’s CPI miss – see table.

- Cumulative cuts from 4.11% effective: 25bp for Wed, 49.5bp Dec, 62.5bp Jan, 74bp Mar, 80.5bp Apr and 93bp Jun

- Look beyond mid-2026 and SOFR futures are now a little lower than pre-CPI levels, albeit only just with a modest 1.5-2.5 tick decline since Friday’s close looking out to end-2027 contracts.

- The terminal implied yield is currently at 2.995% (SFRZ6) having last closed higher on Oct 9 prior to the initial flare-up in US-China trade tensions.

- MNI Fed Preview here: https://media.marketnews.com/Fed_Prev_Oct2025_6a6731f139.pdf with the analyst update to follow later today.