MNI CHINA MONEY MARKET INDEX: Rate Cut Expectations Fall

Chinese interbank traders have reduced expectations for further rate cuts in 2025, but believe the central bank will increase bond purchases to meet end-of-year liquidity demand, MNI’s China Money Market Index indicated on Wednesday.

The PBOC seven-day reverse repo rate outlook sub-index fell to 59.0, with 82% of participants expecting a steady policy rate in the coming month. While 18.0% thought the seven-day repo rate for deposit-taking institutions (DR007) will edge up due to seasonal funding demand, the highest reading so far this year, 66.0% expected the rate to remain stable, with the overall sub-index falling to 49.0 from 54.1 in October.

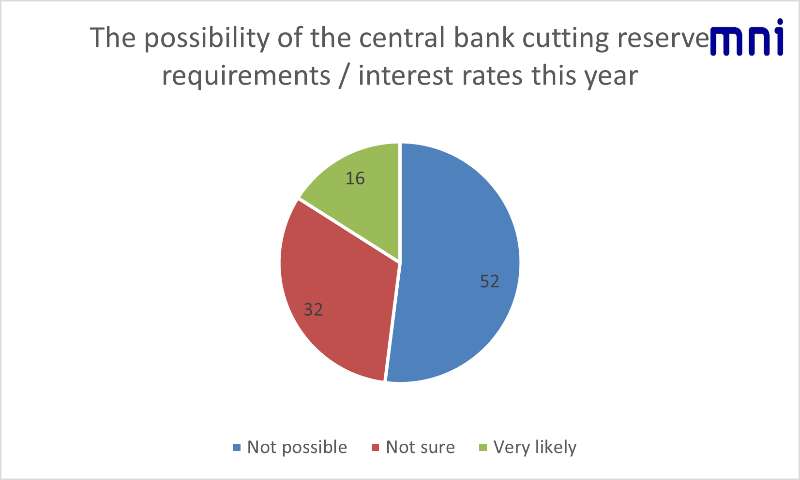

MNI’s special question about the possibility of rate and reserve requirement ratio cuts next month showed reduced easing expectations, with 52% of traders thinking this was “not possible.” (See MNI PBOC WATCH: Rate Cuts Pushed Out, Structural Tools Eyed)

Any additional People’s Bank of China rate cut this year would further squeeze banks’ record-low net interest margins, while the economy already looks on track to achieve the 5% annual growth target, a Jiangsu Province trader said. A Fujian trader predicted a reserve requirement cut before the end of the year to ease pressure on banks.

The current policy bias sub-index rose to 31.0 from 28.6, the highest in 12 months as rate cut expectations faded, with 38.0% of participants foreseeing an easing stance, the lowest since last November. (the lower it reads, the easier the expected policy stance)

The next-six-month policy outlook sub-index indicated the PBOC is expected to remain accommodative, but further easing was predicted by 56.0% of traders, the lowest this year, taking the index to 22.0, the highest this year.

Traders thought more measures are required to buoy the slowing economy. A Shandong trader said October's financial and economic data were both weak, with new loans subdued and real estate-related indicators continuing to decline.

CGB PURCHASES

Another special question showed traders believed the central bank will increase treasury bond buying next month, with 86% of participants anticipating volumes of over CNY100 billion compared with CNY20 billion in October. (See MNI: PBOC To Increase CGB Purchases, Add Longer Tenors)

Major banks continue to hoard bonds, and economic and financing data may continue to decline this quarter, the Fujian trader said. The PBOC could purchase about CNY500 billion in treasury bonds to meet base money supply needs, given maturities, a trader from Hebei told MNI.

An Anhui Province trader predicted the 10-year bond yield would remain stable at 1.80% next month from the previous peak of 1.90% thanks to the restart of PBOC buying.

AMPLE LIQUIDITY

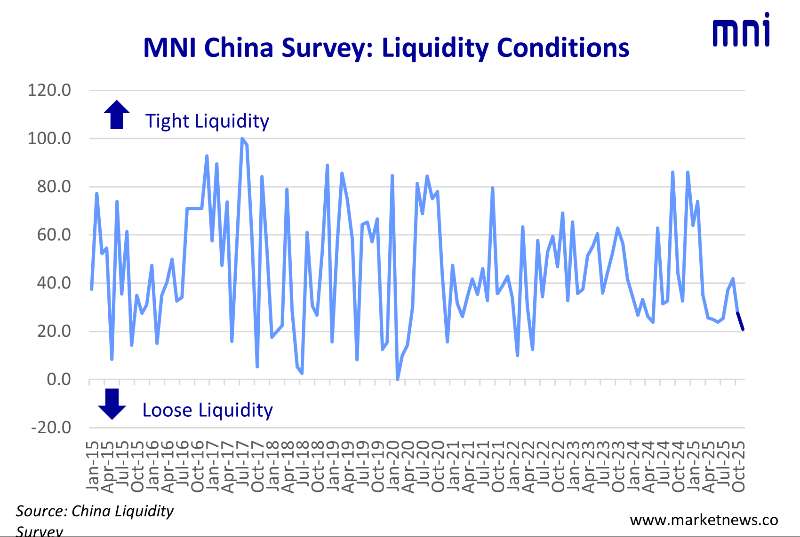

The China liquidity outlook sub-index rose to 51.0 from last month’s 49.0, the highest since May, with 12.0% expecting possible marginal liquidity shortages next month, compared with 10.2% last month. But traders expected the PBOC to ensure comfortable liquidity conditions, taking the overall sub-index for the OMO outlook to 45.0 from 49.0, the lowest this year, with 32% of participants seeing “net injections" next month compared to 26.5% last month.

The PBOC is also expected to increase outright reverse repo operations to inject liquidity. The sub-index edged down to 27.0 from 28.6, with 46% of traders expecting more reverse repos. The Bank has used outright reverse repurchase operations to trade bonds since pausing direct bond trading since January.

The sub-index covering current liquidity fell to 21.0 from 27.6, with 58.0% of participants seeing looser conditions than last month. The sub-index covering the PBOC’s current open market operations showed all participants assessed OMOs as being “in line with demand”.

Liquidity conditions in November have been balanced, with a slight easing, as government bond sales are entering their final phase, and, apart from seasonal factors, no significant fluctuations in funding conditions are expected, said a trader from Henan.

The MNI China Money Market Index (MMI) survey was conducted from Nov 10 to Nov 21, with the participation of 50 traders from both state-owned and joint-venture banks.

Full press report is available here: