GILTS: Off Lows On Cross-Asset Moves, Budget Set To Dominate

Nov-26 10:39

{GB} GILTS: Gilts have recovered from early session lows, with a pullback from session highs in equities providing some stability for bonds.

- Improved risk sentiment, in the wake of the latest speculation surrounding the next Fed Chair and an impending visit of U.S. envoy Witkoff to Russia, provided the initial pressure for gilts. Decreased liquidity ahead of the Budget may have also factored in.

- Chancellor Reeves will deliver the Budget around ~12:30 London.

- H6 futures -13 at 91.08 vs. lows of 90.79. Initial support and resistance 90.53 and 91.26. Yesterday’s rally undermined the recent bearish move.

- Yields ~1bp lower to ~2bp higher, curve steeper.

- 2s10s ~74bp after the recent pullback from 80bp.

- 5s30s ~141bp after the spread failed to close above 145bp last week.

- Gilt/Bunds little changed at 182bp, comfortably within the recent ~170-190bp range.

- 30-Year swap spreads have retraced 4bp of the 6bp of narrowing triggered by increases in fiscal and political risk premia over the past couple of weeks.

- As noted in recent bullets, we believe that under-delivery at today’s Budget presents the greatest risk to current market pricing.

- Questions surrounding fiscal credibility following the event would risk fresh curve steepening, swap spread narrowing and gilt widening vs. Bunds.

- Our full Budget preview can be found here.

- While our latest Gilt Week Ahead outlines the key metrics that we are looking at ahead of the event.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: USDJPY Looks to Extend Winning Streak as Fed/BOJ Meetings Near

Oct-27 10:31

- Both higher bond yields and equities initially provided a positive impulse for USDJPY on Monday, taking the pair up to 153.26 highs ahead of the European open. Japan officials noted they were monitoring FX markets for disorderly moves, and although USDJPY has reverted back below the 153.00 handle, the remarks didn't suggest intervention risks had risen for now.

- Notably, the overnight peak came within one pip of 153.27, the Oct 10 high and a bull trigger. Clearance of this hurdle would confirm a resumption of the medium-term uptrend and will be eagerly monitored as we approach this week’s Fed and BOJ meetings. While the bar for a surprise on either rate decision is extremely high, each committee’s rhetoric will be key in shaping the policy outlook in coming months, especially given the dissenting votes both boards have had at prior meetings.

- Markets will be looking for signs of a significant hawkish turn from the BOJ, and if more of the committee join Takata in their view that now is a prime opportunity to raise the policy rate. Takata recently added the BOJ's "tankan" business survey in October and findings from its branch managers suggest improvements in job and income conditions are underpinning consumption.

- SocGen have said the yen is being sold as much because the $/Y correlation with bond yields has broken down. They believe momentum is dominating the price action at the moment and month-end flows may be all that is holding the market back from a push back to 150.

- Market participants will be well aware that the politically driven gap at the start of the month would require a move to 147.47 to be filled. The first important support to watch lies at 150.90, the 20-day EMA.

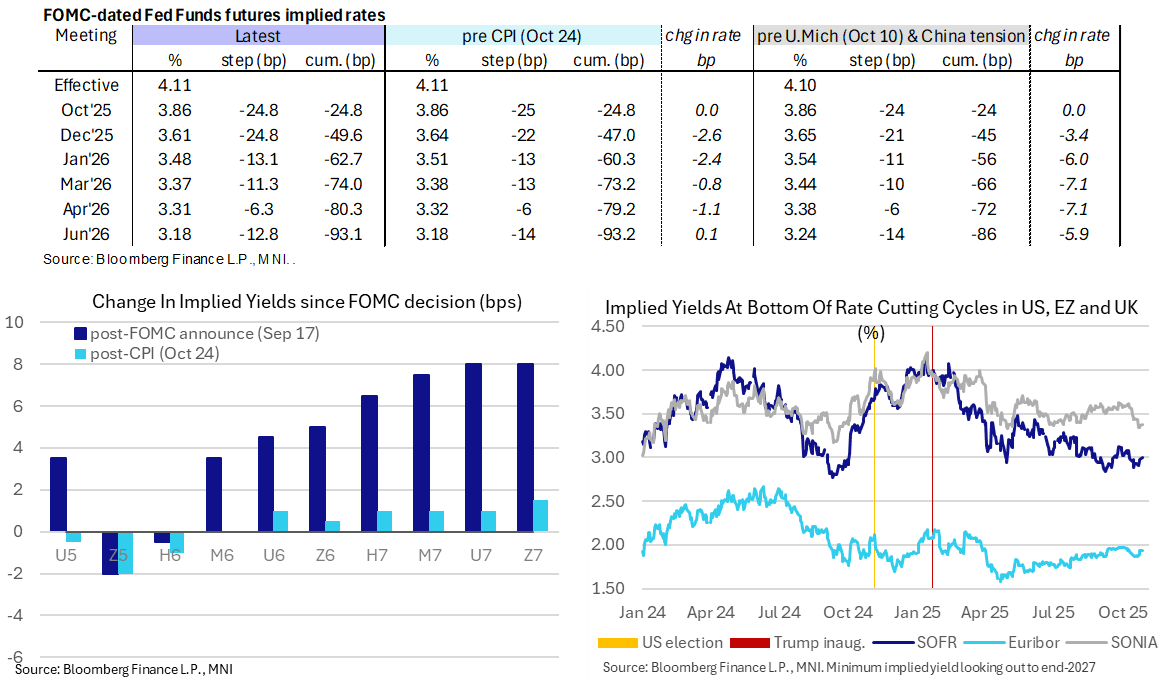

STIR: US-China Trade Deal Optimism Limits Dovish CPI Impact

Oct-27 10:31

- US-China trade deal optimism ahead of Trump-Xi meeting this week sees Fed Funds implied rates 1-2bp higher since Friday’s close, Wednesday’s decision aside where the Fed is still fully priced to cut 25bps.

- It’s seen these nearer term meetings reverse a large part of the dovish reaction to Friday’s CPI miss – see table.

- Cumulative cuts from 4.11% effective: 25bp for Wed, 49.5bp Dec, 62.5bp Jan, 74bp Mar, 80.5bp Apr and 93bp Jun

- Look beyond mid-2026 and SOFR futures are now a little lower than pre-CPI levels, albeit only just with a modest 1.5-2.5 tick decline since Friday’s close looking out to end-2027 contracts.

- The terminal implied yield is currently at 2.995% (SFRZ6) having last closed higher on Oct 9 prior to the initial flare-up in US-China trade tensions.

- MNI Fed Preview here: https://media.marketnews.com/Fed_Prev_Oct2025_6a6731f139.pdf with the analyst update to follow later today.

JAPAN: Moody's Affirm Japan at A1; Outlook Stable

Oct-27 10:29

"*MOODY'S RATINGS AFFIRMS JAPAN'S A1 RATINGS, MAINTAINS STABLE" - bbg

- "JAPAN RATING ACTION REFLECTS TRACTION ON REFLATION & FISCAL POLICY GEARED TOWARDS CONSOLIDATION

- DO NOT EXPECT RECENT LEADERSHIP TRANSITION TO SIGNIFICANTLY REVERSE JAPAN'S GAINS IN FISCAL CONSOLIDATION" - Reuters