MNI RBNZ WATCH: Easing Bias Maintained, But 2026 Hold Likely

The Reserve Bank of New Zealand maintained a slight easing bias at its November meeting after a widely-expected 25-basis-point cut, despite the largely hawkish tone of its latest Monetary Policy Statement, with acting Governor Christian Hawkesby noting that the Bank’s updated forecasts show a modest preference for a further rate cut

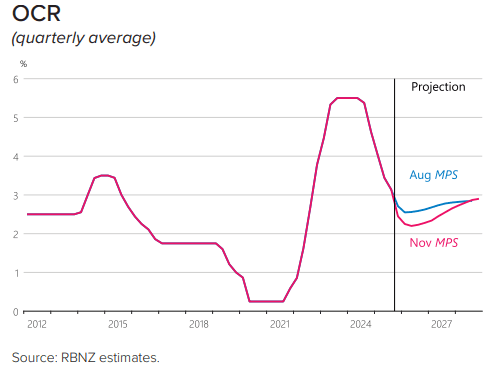

“You'll notice that in the track there's a very slight downward tilt,” Hawkesby said, pointing to the updated OCR path showing a 2.2% rate. “That's just a nod to the likelihood that if the OCR was to change over the next three-to-six months, it might be more likely to go down than up, and then further out in that projection, chances are more likely to go up than down.” (See chart)

Hawkesby spoke at a press conference following the widely expected cut to 2.25%, a decision reached by a five–one vote after a discussion that included holding the rate. (See MNI RBNZ WATCH: RBNZ To Cut 25bp, Signal Path Ahead)

The Bank’s central projection implied holding the OCR through 2026, Hawkesby noted. “We think it puts the committee in a really strong position into next year to have the time to see how the economy evolves … Shocks occur, and so the committee's in a great position to navigate that.” The RBNZ retains "full optionality… every option is always on the table,” he added.

RBNZ overnight index swaps closed 2-11bp stronger across meeting dates following the decision, with a 2.193% rate priced in by May.

RECOVERY EXPECTATIONS

Hawkesby said the large negative Q2 GDP number reflected one-off factors, seasonal quirks and supply constraints, and that activity was not as weak as the headline suggested. High-frequency indicators monitored through the Bank’s GDP gauge now show activity picking up, he said, citing stronger consumer spending, stabilising labour market conditions, rising employment and hours worked. “We're not waiting for a recovery. It's happening right now through Q3 and Q4.”

Chief Economist Paul Conway said labour market dynamics are at a low point but turning. Businesses have been reluctant to lay off workers after post-Covid hiring difficulties, while unemployed workers have struggled to find new jobs. “We think of it as a low-hire, low-fire labour market,” he said. The unemployment rate, at 5.3%, is expected to hold around that level into summer before gradually improving, he added.

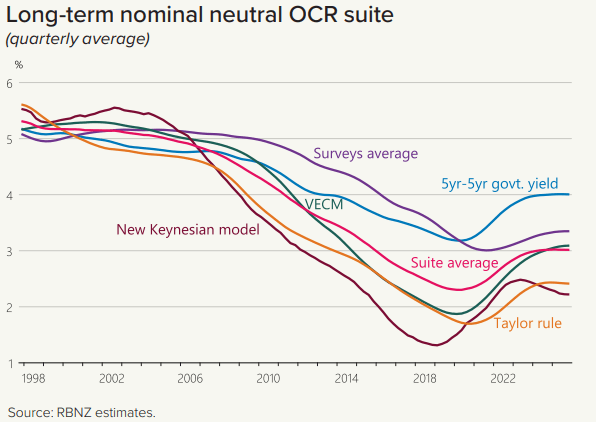

Hawkesby said the neutral interest rate remains between 2.5-3.5%, noting the OCR at 2.25% is “south of that range” and therefore stimulatory.

GLOBAL UNCERTAINTY

Global risks remain balanced, highlighting upside and downside pressures around the domestic outlook, according to Hawkesby. He noted that the effects of the U.S. trade war have been softened by an AI-driven investment boom, but warned that a disappointment in productivity gains would pose risks. He also flagged concerns about global inflation pressures linked to fiscal dynamics and the erosion of central bank independence abroad.

Conway added that policy cannot be set on the basis that a large shock might occur, but as confidence increases that a particular scenario is materialising, it can be incorporated into the central track. “There are real risks out there … but if they happen, we think we’re in a good place to deal with it as it rolls through the New Zealand economy,” he said.

The MPC next meets Feb 18.