MNI US OPEN - Trump Says Ukraine Can Retake All Its Land

EXECUTIVE SUMMARY

- TRUMP POST STRIKES POSITIVE TONE, BUT COULD PUT NATO & KYIV ON NOTICE

- TRUMP CANCELS MEETINGS WITH DEMOCRATS, BRINGING SHUTDOWN CLOSER

- TAKAICHI SAYS BOJ SHOULD DECIDE POLICY STEPS, SOFTENING STANCE

- AUSTRALIA MONTHLY CPI TRACKS HIGHER IN AUGUST

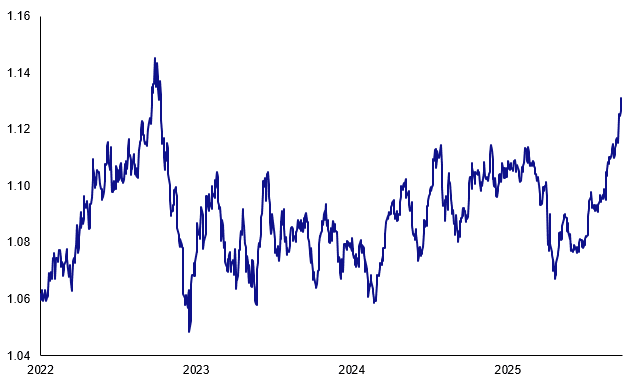

Figure 1: AUD/NZD surges to fresh cycle high following Australia monthly CPI data

Source: MNI/Bloomberg Finance L.P.

NEWS

US/RUSSIA/UKRAINE (MNI): Trump Post Strikes Positive Tone, but Could Put NATO & Kyiv on Notice

There has been significant international focus on the comments from US President Donald Trump made in a Truth Social post regarding the war in Ukraine. Much of the commentary has focused on Trump's disparaging remarks about Russia's inability to win the war swiftly, and his claims that "Putin and Russia are in BIG Economic trouble," as an indication that the president's sometimes lukewarm stance on backing Kyiv has been turned into fulsome US support.

However, the words within the post may in fact indicate Trump's intentions to step back from efforts to support Ukraine and end the war. While appearing boosterish on Kyiv's chances in the war, the post says Ukraine could take back all of its territory "with the support of the European Union," not the US, and that its old borders can be restored "With time, patience, and the financial support of Europe and, in particular, NATO,", again not the US.

US/EU (BBG): EU Makes Fresh Push With US to Revive Talks on Metals Tariffs

The European Union’s trade chief, Maros Sefcovic, will meet with US Trade Representative Jamieson Greer this week to try and restart stalled talks to lower tariffs on steel and aluminum exports. The European Commission, the EU’s executive arm responsible for trade matters, has proposed to eliminate or significantly reduce the duties. But it has not heard back from the US on its offer, EU trade chief Sefcovic said in an interview with Bloomberg.

US (WaPo): Trump Cancels Meetings With Democrats, Bringing Shutdown Closer

President Donald Trump on Tuesday canceled a meeting with Democratic congressional leaders to avoid a shutdown over government funding, arguing it could not "possibly be productive" due to Democratic demands. The reversal leaves the two parties in Washington without a solution to keep the government open past Sept. 30, when the current fiscal year ends and funding runs out. The meeting scheduled for Thursday was intended to negotiate a path forward.

US (BBG): Greer Says US Could Finalize Some Asean Trade Deals in Weeks

The US expects to finalize trade deals with some Southeast Asian countries within weeks as President Donald Trump’s policies prompt a wave of efforts to negotiate for lower tariffs. “President Trump and myself are proud of the work we have done together on these deals and expect to finalize these agreements in the coming months or even weeks for some,” US Trade Representative Jamieson Greer said ahead of meetings with Association of Southeast Asian Nations economic ministers in Kuala Lumpur on Wednesday.

US/ARGENTINA (BBG): Trump Backs Milei, Downplays Need for ‘Bailout’ in Argentina

US President Donald Trump offered broad support for Argentine leader Javier Milei in New York during their first bilateral meeting, but stopped short of providing details about financial aid for the South American government. “He’s done a fantastic job,” Trump said Tuesday sitting next to Milei on the sidelines of the United Nations General Assembly. “We’re going to help them. I don’t think they need a bailout.”

MNI SNB PREVIEW: Avoid Negativity

Markets and analysts see a hold at 0.00% at Thursday’s meeting as most likely, with a cut into negative territory appearing improbable given inflation has remained within the SNB’s defined range of price stability for three months now. The rates outlook is likely to continue to be characterized by a high bar to further cuts into negative territory, a comment on that may or may not make it into the press statement but will anyways be discussed in the subsequent media conference.

ECB (BBG): ECB’s Cipollone Says Risks to Inflation Are ‘Very Balanced’

European Central Bank Executive Board member Piero Cipollone doesn’t see major threats to inflation in either direction, with interest rates currently well positioned. Europe’s economy has been “quite resilient” despite the uncertainty caused primarily by trade, Cipollone told Bloomberg Television. After a slowdown this quarter, growth should resume its earlier pattern, he said.

FRANCE (BBG): Macron Courts Wall Street Leaders, Pitching French Stability

Even as his country still has no government, Emmanuel Macron is making his pitch to Wall Street: Invest in France — every democracy has its ups and downs. The French president, in New York for the United Nations General Assembly, hosted a breakfast Tuesday with some of Wall Street’s biggest names, including Blackstone Inc. Chief Executive Officer Steve Schwarzman, Bank of America Corp. CEO Brian Moynihan and John Zito, co-president of Apollo Global Management Inc.’s asset-management arm.

CHINA (MNI): China WTO Decision Promotes Global Trade Reform - Li

MNI (Beijing) China’s decision to relinquish its special and differential treatment (SDT) at the World Trade Organization (WTO) will invigorate WTO reforms and further accelerate global trade and investment liberalisation, Li Chenggang, China's international trade negotiator and vice minister at the Ministry of Commerce told reporters on Wednesday. Beijing announced that it will no longer seek the advantages afforded by its developing country status within the WTO, the state-run news agency Xinhua reported on Tuesday.

CHINA (BBG): China’s State Banks Shift Dollar-Swap Strategy as Yuan Gains

Chinese state-owned banks are selling the yuan in the spot market and offsetting their trades with swaps, putting the brakes on a recent rise in the currency. The lenders have been ramping up their purchases of spot dollars over the past few months and offering large amounts of dollars for yuan in the currency swap market, according to traders who asked not to be identified as they’re not authorized to speak publicly.

BOJ (MNI EXCLUSIVE): BOJ Sees No Need to Rush Rate Hikes

MNI discusses the BOJ's must-haves for further rate hikes. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

JAPAN (BBG): Takaichi Says BOJ Should Decide Policy Steps, Softening Stance

A top contender vying to lead the ruling Liberal Democratic Party sought to distance herself from dovish remarks made a year ago, saying the Bank of Japan should decide the particulars of monetary policy. “In terms of economic policy, the government is responsible for deciding the direction of fiscal and monetary policy,” Sanae Takaichi said during a debate with the four other contenders Wednesday.

RBNZ (MNI): Riksbank Breman Appointed New RBNZ Governor – Things to Note

The NZ government has appointed Riksbank First Deputy Governor Anna Breman to be the new RBNZ governor. Breman will start the position on December 1 of this year on a 5-year term. She will leave the Riksbank on October 10. Breman is an experienced economist, previously Chief Economist and Global Head of Macro Research at Swedbank before her time at the Riksbank (alongside roles in the Swedish Ministry of Finance and the World Bank). She joined the Riksbank in 2019, becoming the Board's number 2 in 2022.

MNI BANXICO PREVIEW: 25bp Easing Pace to Continue

After slowing the easing pace in August, the Banxico committee is expected to deliver another 25bp rate reduction, taking the overnight target rate to 7.5%. After dissenting in favour of a rate hold at the two previous meetings, there will be the usual attention on Deputy Governor Heath’s vote, as he continues to focus his rhetoric around the stalling of progress on core disinflation.

DATA

GERMANY DATA (MNI): Broad-Based Deterioration Behind IFO Decline

- GERMANY SEP IFO BUSINESS CLIMATE INDEX 87.7

Contrary to expectations, Germany's IFO Business Climate Index fell in September, bucking its uptrend previously seen this year at 87.7 (89.4 consensus, 88.9 prior, revised from 89.0). Across sectors, services was the main difference to yesterday's flash PMI release, with IFO seeing a negative sectoral balance for the first time since May while the PMI notably outperformed there. Overall, "hopes for economic recovery suffer a setback", IFO comments. The current assessment (85.7 vs 86.6 cons; 86.4 prior) and expectations (89.7 vs 92.0 cons; 91.4 prior, revised from 91.6) readings were both, unexpectedly, lower than before.

UK DATA (MNI): Brightmine Median Pay Deals Still 3.0%, But Uptick in Pay Freezes

- UK JUN-AUG BRIGHTMINE MEDIAN PAY AWARDS +3.0% (VS +3.0% MAY-JUL)

Brightmine median pay awards in the 3 months to August remained at 3.0% for the ninth consecutive rolling quarter, the longest period of stagnation on record. In the bargaining year from September 2024 to August 2025, the median is also 3.0%, down from 4.9% in the bargaining year to August 2024. Persistent inflationary pressures following the August rate cut, slow growth, and uncertainty over tax rises and the Autumn Budget are highlighted as drivers.

SWEDEN DATA (MNI): Sep ETI: Sentiment Picking Up, Inflation Pressures Easing

The Swedish Economic Tendency indicator rose to a year-to-date high of 97.2 in September (vs 96.3 prior). Increases were seen in consumer confidence, alongside the retail, construction and manufacturing sectors. Services sector confidence declined a little. Sentiment remains below the neutral 100 level, but the combination of another Riksbank rate cut and increased Government fiscal spending (with particular emphasis on households) should support further improvements ahead. Key for both institutions is whether this translates to better real consumer spending/economic activity outcomes.

AUSTRALIA DATA (MNI): Aussie Monthly CPI Tracks Higher

- AUSTRALIA MONTHLY AUG CPI 0.1% MM, 3% YY

Australia’s monthly CPI indicator rose 3% y/y in August, up 20 basis points from July, while the trimmed mean measure slowed to 2.6% from 2.8%, the Australian Bureau of Statistics said Wednesday. The headline result was 10 basis points above market expectations. “The 3.0% annual CPI inflation to August was up from 2.8% in July, marking the highest annual rate since July 2024,” said Michelle Marquardt, ABS head of price statistics.

JAPAN DATA (MNI): Japan Aug Trimmed Mean Rises 2.0%; July 2.0%

Japan’s trimmed mean measure of underlying inflation rose 2.0% y/y in August, unchanged from July, staying above 2% for the eighth straight month, Bank of Japan data showed Wednesday. The figure highlights a slowing pace of cost pass-through, driven by higher rice prices and labour costs. The release follows Friday’s data showing annual core CPI rose 2.7% y/y in August, down from 3.1% in July, but above the BOJ’s 2% target for the 41st consecutive month.

JAPAN DATA (MNI): Manufacturing PMI Dips in September, Services Holds Up

Japan's preliminary S&P PMIs for September were below the August outcomes. Manufacturing printed at 48.4, versus 49.7 in August. The services print was 53.0, against a 53.1 prior. The composite fell to 51.1 versus 52.0 in August. The manufacturing print is back to lows from March of this year. We did get close to 47.0 for the index in Q1 of 2024. The detail showed output down to 47.3 from 49.8 in August. New orders were also down in the month. The US manufacturing PMI fell for Sep as well, although remains at much higher outright levels (52.0).

FOREX: USD Outperforming, AUDNZD Surges to Fresh Cycle High Above 1.13

- Over the course of the European morning, the US Dollar is trading with a supportive tone. Despite most major pairs remaining well within the post-Fed ranges, the likes of EUR and GBP have extended session declines to just shy of 0.4% in recent trade. For EURUSD, the solid amount of option expiries between 1.1750/1.18 appears to have capped the overnight price action, with the pair slowly edging back below 1.1775 as we approach the NY crossover.

- GBPUSD has traded through the 50-day EMA and this leaves support at 1.3458 exposed, a trendline drawn from the Aug 1 low. Clearance of this line would strengthen a bearish threat.

- Firmer-than-expected monthly CPI data in Australia is prompting some Aussie outperformance, with AUDUSD currently up 0.15% and bucking the stronger dollar theme. Market participants have been more focussed on AUDNZD, which has extended its impressive rally on Wednesday to trade to a fresh cycle high of 1.1317. Resistance remains scant on the chart until 1.1491, the 2022 high. It is also worth noting that the NZ government has appointed Riksbank First Deputy Governor Anna Breman to be the new RBNZ governor.

- The low yielders have been under pressure this morning, with USDJPY notably rising to within 10 pips of the post Fed highs at 148.38. Uncertainty regarding Japanese politics and the upcoming LDP leadership election may be playing its part here, while moving average studies continue to highlight a dominant uptrend. Furthermore, the impressive grind higher for the likes of EURJPY and CHFJPY bolster the bearish yen theme.

- US new home sales is the main data point later today, before Thursday’s SNB decision and US jobless claims data.

EGBS: Monday's High Contains Upside in Bund Futures Again

- The light early bid in Bund futures faded as the bidding deadline for today’s 7-year Bund auction approached. With supply now in the rear view, Bunds are +10 ticks at 128.28. Monday’s high of 128.41 has contained upside once again, with today’s range just 21 ticks wide.

- Early upside in Bunds may have been driven by renewed concerns around the Russia-Ukraine conflict alongside a weaker-than-expected German September IFO print.

- German yields are up to 1bp lower across the curve, with a light bull flattening bias intact. The 7-year Bund results were much better than last month’s soft outing.

- 10-year EGB spreads to Bunds are up to 1.5bps wider, seemingly a result of the Russia/Ukraine concerns, with BTPs underperforming (spread to Bunds at ~81bps).

GILTS: Off Highs, Curve Flatter

Modest weakness came in the wake of the soft demand metrics witnessed at this morning’s short 5-Year auction, but bulls have already started to counter the downside move.

- A reminder that early gilt strength came in the wake of the late Tuesday bid in Tsys.

- Futures pierced yesterday’s high (91.11) at the open, topping out at 91.28, last ~91.15.

- Bulls now look to the September 11 high (91.82), while initial support of note isn’t seen until the Sep 2/22 lows (90.65/60).

- Yields flat to 1.5bp lower, curve flatter, 2s10s ~5bp off last week’s pullback low, while 5s30s is ~3bp off last week’s base.

- The DMO announced that it will launch a new conventional 31 Jan ’41 gilt via syndication in the week commencing 13 Oct’25, matching our expectations.

- SONIA futures now -0.5 to +2.0, following cues from further out the curve, with BoE-dated OIS still pricing ~6bp of easing through year-end.

- BoE’s Greene will speak on supply shocks and monetary policy this evening (17:30 London).

- Brightmine wage data pointed to another steady 3.0% rise.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Nov-25 | 3.951 | -1.6 |

Dec-25 | 3.908 | -5.9 |

Feb-26 | 3.791 | -17.6 |

Mar-26 | 3.750 | -21.8 |

Apr-26 | 3.665 | -30.2 |

Jun-26 | 3.638 | -32.9 |

EQUITIES: Eurostoxx 50 Futures Remain Close to Bull Trigger at 5525.00

Eurostoxx 50 futures are trading closer to their recent highs. The contract recently cleared resistance around the 20-day EMA - a bullish development - and the subsequent rally reinforces a bullish theme. The move signals potential for a climb towards 5525.00, the Aug 22 high and a bull trigger. On the downside, key support to monitor is 5302.00, the Sep 2 low. Clearance of this level is required to reinstate a bearish theme. A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high on Monday. Price has recently breached the 6700.00 handle and this signals scope for an extension towards 6787.63, a Fibonacci projection point. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Initial support to watch lies at 6625.74, the 20-day EMA.

- Japan's NIKKEI closed higher by 136.65 pts or +0.3% at 45630.31 and the TOPIX ended 7.28 pts higher or +0.23% at 3170.45.

- Elsewhere, in China the SHANGHAI closed higher by 31.809 pts or +0.83% at 3853.642 and the HANG SENG ended 359.53 pts higher or +1.37% at 26518.65.

- Across Europe, Germany's DAX trades lower by 15.08 pts or -0.06% at 23596.25, FTSE 100 lower by 16.82 pts or -0.18% at 9206.49, CAC 40 down 9.72 pts or -0.12% at 7862.3 and Euro Stoxx 50 down 2.79 pts or -0.05% at 5469.6.

- Dow Jones mini down 0 pts or 0% at 46637, S&P 500 mini up 8.25 pts or +0.12% at 6723.25, NASDAQ mini up 62.25 pts or +0.25% at 24890.5.

Time: 10:00 BST

COMMODITIES: Next Objective for Gold is $3800 Handle

The trend condition in WTI futures is unchanged - a bear cycle remains intact and short-term gains are considered corrective. The pullback from the Sep 2 high highlights a possible reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $65.43, the Sep 2 high. Key short-term resistance has been defined at $68.43, the Jul 30 high. A stronger resumption of weakness would open $57.50, the May 30 low. Gold is in a clear bull cycle and shallow short-term pullbacks remain corrective. A fresh all-time high once again, yesterday, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is the $3800.0 handle. Initial firm support lies at $3610.2, the 20-day EMA. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend.

- WTI Crude down $0.12 or -0.19% at $63.28

- Natural Gas down $0.02 or -0.81% at $2.83

- Gold spot up $6.72 or +0.18% at $3770.47

- Copper down $1.75 or -0.38% at $462.7

- Silver up $0.12 or +0.27% at $44.1487

- Platinum down $5.16 or -0.35% at $1472

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 24/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 24/09/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/09/2025 | 1400/1000 | *** | New Home Sales | |

| 24/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 24/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 24/09/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 24/09/2025 | 1630/1730 | BOE Greene On Supply Shocks and MonPol | ||

| 24/09/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 24/09/2025 | 2010/1610 | San Francisco Fed's Mary Daly | ||

| 25/09/2025 | - | Swiss National Bank Meeting | ||

| 25/09/2025 | 0600/0800 | ** | PPI | |

| 25/09/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 25/09/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/09/2025 | 0730/0930 | *** | SNB Interest Rate Decision | |

| 25/09/2025 | 0800/1000 | ** | M3 | |

| 25/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/09/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 25/09/2025 | 1220/0820 | Chicago Fed's Austan Goolsbee | ||

| 25/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 25/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 25/09/2025 | 1230/0830 | * | Payroll employment | |

| 25/09/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/09/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 25/09/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 25/09/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/09/2025 | 1300/0900 | New York Fed's John Williams | ||

| 25/09/2025 | 1300/0900 | KC Fed's Jeff Schmid | ||

| 25/09/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 25/09/2025 | 1400/1000 | *** | NAR existing home sales | |

| 25/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 25/09/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 25/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 25/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 25/09/2025 | 1700/1300 | Fed Governor Michael Barr | ||

| 25/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 25/09/2025 | 1740/1340 | Dallas Fed's Lorie Logan | ||

| 25/09/2025 | 1900/1500 | *** | Mexico Interest Rate | |

| 25/09/2025 | 1930/1530 | San Francisco Fed's Mary Daly |