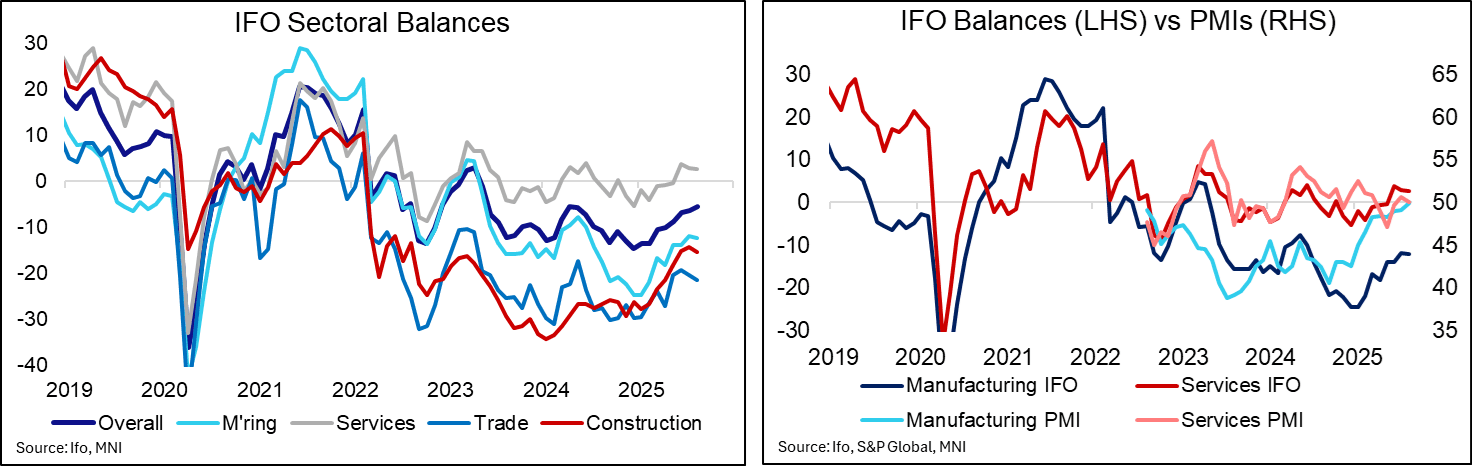

GERMAN DATA: Broad-Based Deterioration Behind IFO Decline

Contrary to expectations, Germany's IFO Business Climate Index fell in September, bucking its uptrend previously seen this year at 87.7 (89.4 consensus, 88.9 prior, revised from 89.0). Across sectors, services was the main difference to yesterday’s flash PMI release, with IFO seeing a negative sectoral balance for the first time since May while the PMI notably outperformed there. Overall, "hopes for economic recovery suffer a setback", IFO comments.

- The current assessment (85.7 vs 86.6 cons; 86.4 prior) and expectations (89.7 vs 92.0 cons; 91.4 prior, revised from 91.6) readings were both, unexpectedly, lower than before.

- Across sectors:

- "In manufacturing, the index declined. Companies assessed their current situation as slightly worse, and expectations became more cautious. New orders experienced another decline. Any glimmers of hope that had emerged among capital goods manufacturers in the previous month have faded."

- "In the service sector, the business climate deteriorated noticeably. Expectations have grown markedly more pessimistic, and the indicator fell to its lowest level since February. Companies also downgraded their assessments of the current situation. Sentiment deteriorated particularly in the transport and logistics sector."

- "In trade, the business climate worsened, driven by more pessimistic expectations. However, companies assessed the current situation somewhat more positively. The business climate index rose in retail but fell in wholesale."

- "In construction, the index increased again following last month’s setback. Companies were slightly more satisfied with current business. Expectations for the coming months continued to brighten."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EU-BOND AUCTION RESULTS: 2.875% Dec-27 / 3.375% Dec-35 / 3.375% Oct-38 EU-bonds

| 2.875% Dec-27 EU-bond | 3.375% Dec-35 EU-bond | 3.375% Oct-38 EU-bond | |

| ISIN | EU000A3K4EW6 | EU000A4D8KD2 | EU000A3K4D74 |

| Amount | E2.12bln | E1.951bln | E1.454bln |

| Previous | E2.392bln | E2.182bln | E1.174bln |

| Avg yield | 2.12% | 3.12% | 3.49% |

| Previous | 2.33% | 3.10% | 3.38% |

| Bid-to-cover | 1.31x | 1.66x | 1.25x |

| Previous | 1.59x | 1.28x | 1.42x |

| Avg Price | 101.66 | 101.52 | 98.81 |

| Low Price | 101.65 | 101.49 | 98.77 |

| Pre-auction mid | 101.636 | 101.422 | 98.682 |

| Prev avg price | 101.45 | 102.46 | 99.93 |

| Prev low price | 101.44 | 102.42 | 99.90 |

| Prev mid-price | 101.416 | 102.374 | 99.852 |

| Previous date | 24-Feb-25 | 23-Jun-25 | 28-Apr-25 |

GERMAN T-BILL AUCTION RESULTS: 3/9-month Bubills

| Type | 3-month Bubill | 9-month Bubill |

| Maturity | Nov 19, 2025 | May 13, 2026 |

| Allotted | E1.595bln | E2.187bln |

| Previous | E1.9bln | E2.495bln |

| Total sold | E2bln | E3bln |

| Target | E2bln | E3bln |

| Avg yield | 1.839% | 1.913% |

| Previous | 1.799% | 1.806% |

| Bid-to-cover | 2.16x | 2.22x |

| Previous | 1.73x | 1.68x |

| Bid-to-offer | 1.72x | 1.62x |

| Previous | 1.64x | 1.39x |

| Previous date | Jul 21, 2025 | Jul 21, 2025 |

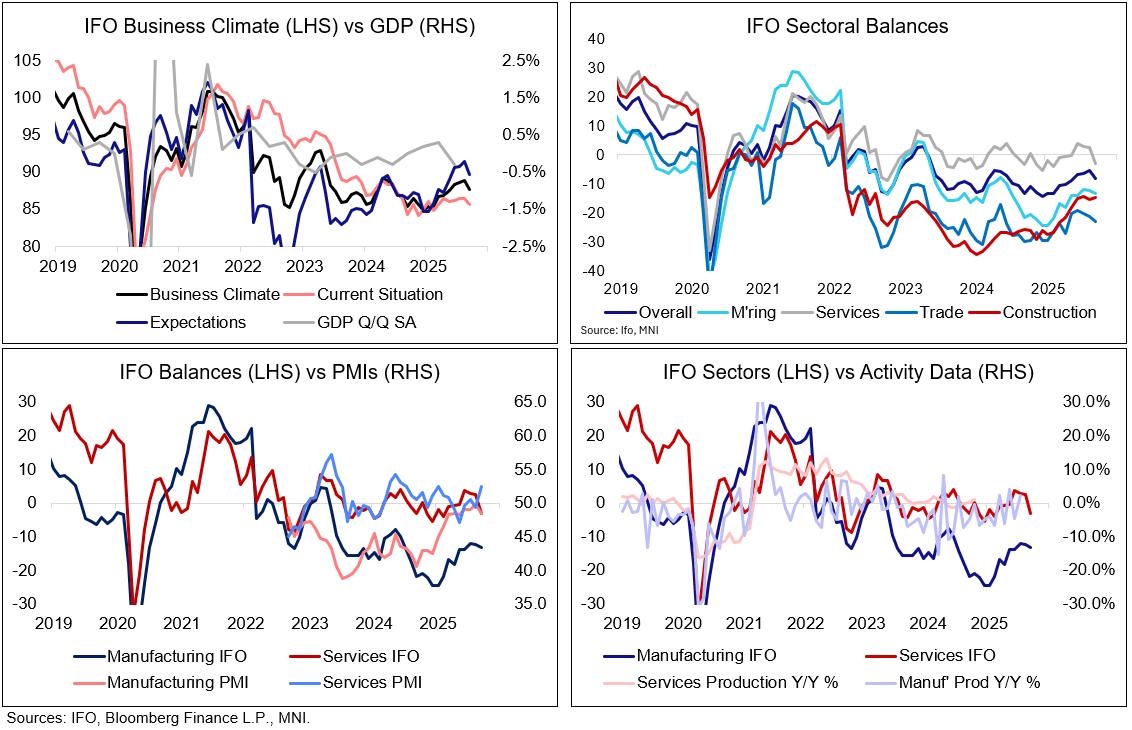

GERMAN DATA: Latest Ifo Improvement On Shaky Ground Looking By Sector

The details of the Ifo business climate by sector didn’t corroborate the minor increase in the overall index, seemingly implying a higher response rate from services-related firms in the August survey. We wonder if that's down to response rates in the holiday season.

- The business climate balance increased from a seasonally adjusted -6.4 to -5.5 (we wrote on the index earlier – GERMAN DATA: A Sixth Consecutive Improvement For Ifo Business Climate – 0935BST) but all four main sectors saw their business climate balance soften.

- Latest sectoral values with highlights from the Ifo press release (link):

- Services inched lower for a second month to 2.6, but remains the only sector in positive territory. “While the current situation was assessed as significantly better, expectations became more cautious. Sentiment, however, improved among architecture and engineering firms.”

- Manufacturing gave back some of its latest increase, dipping to -12.2 from -11.9. “Companies were somewhat less satisfied with current business. Expectations were revised slightly downward, and there are still no indications of growth in order intake. Sentiment among capital goods manufacturers improved noticeably.”

- Construction unwound the latest increase as it fell to -15.3 from -14.3. “The index edged down slightly after many months of stability. Companies expressed less satisfaction with the current situation. However, their outlook for the coming months improved.”

- Trade continues to lag and saw a second monthly decline to -21.4 from -20.3 for its lowest since April. “The index weakened, driven by poorer business performance. However, expectations were slightly less pessimistic.”