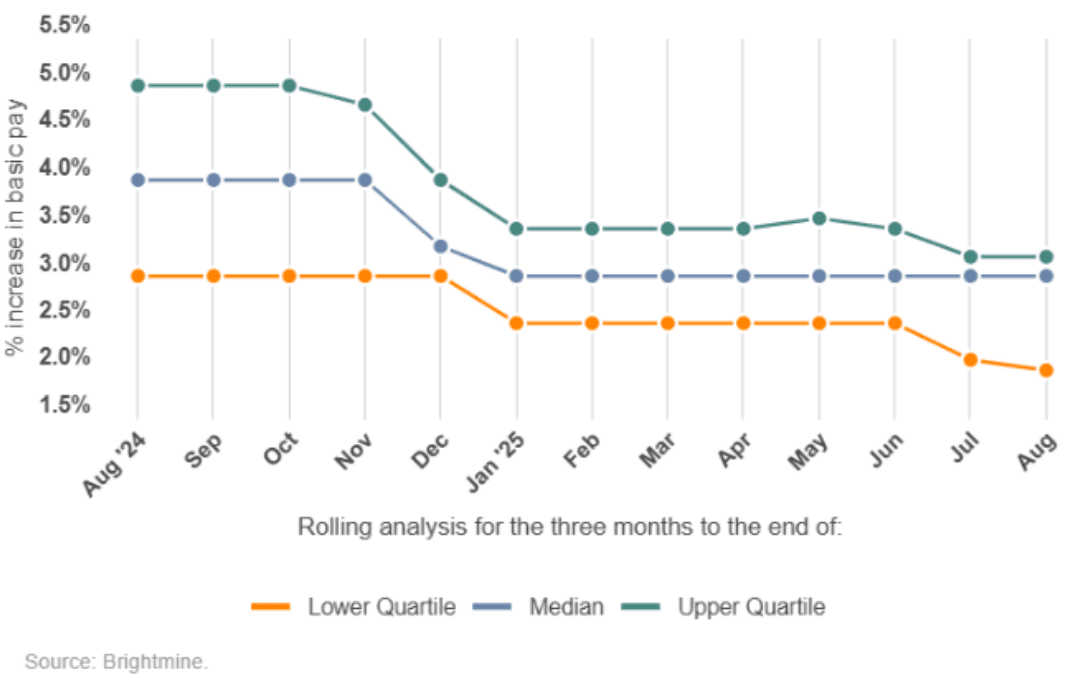

UK DATA: Brightmine Median Pay Deals Still 3.0%, But Uptick In Pay Freezes

Brightmine median pay awards in the 3 months to August remained at 3.0% for the ninth consecutive rolling quarter, the longest period of stagnation on record. In the bargaining year from September 2024 to August 2025, the median is also 3.0%, down from 4.9% in the bargaining year to August 2024. Persistent inflationary pressures following the August rate cut, slow growth, and uncertainty over tax rises and the Autumn Budget are highlighted as drivers.

- Despite the unchanged median and upper quartile pay deals from last month's release (both remaining at cycle lows), the lower quartile fell for the second consecutive month, now below 2.0%, indicating a greater share of pay increases which won't be a concern to the MPC in terms of inflationary pressure from wages.

- Also of note, 10.7% of settlements in the three months to August resulted in a pay freeze, versus no freezes recorded in the previous rolling quarter, supporting the downward trend despite the headline median figure.

- 52.9% of pay deals were lower than those agreed in 2024, 23.5% matched last year, while 14.7% were higher.

- The press release notes that this level of stability in median pay awards "has not been seen since before the pandemic ... However, with inflation still elevated and recruitment slowing, employers remain cautious about their approach to pay."

- The Jun-Aug data was based on pay awards between 1 June and 31 August 2025, covering pay review outcomes for over 600,000 employees.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: USD/JPY - Collapses Back To Support, Was Powell That Dovish ?

The Friday night range was 146.58-148.74, Asia is currently trading around 147.05. USD/JPY collapsed lower with US yields as the markets initial interpretation of Powell’s speech was taken to be quite dovish. Was it that dovish ? That remains to be seen but the price action was again clear, the market is still very quick to sell USD’s. Price is very quickly back to testing its recent support towards 146.00, the demand has been pretty solid back towards here all of August, lets see if it can continue to hold. A sustained break below here would see short-term direction turn lower again. CFTC data shows leveraged accounts again added to JPY shorts so this reaction to Powell would not have been welcome and a break sub 145/146 would add pressure.

- (Bloomberg) -- “JBank of Japan Governor Kazuo Ueda said he expects a tight labor market to keep upward pressure on wages, reflecting his view that stable inflation is set to take hold. “Wage growth is spreading from large enterprises to small and medium enterprises,” Ueda said Saturday.”

- “The leaders of Japan and South Korea met on Saturday and pledged to enhance cooperation between the two countries, saying economic and security challenges require them to step up bilateral relations.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($939m).Upcoming Close Strikes : 148.00($942m Aug 26), 147.95($885m Aug 27), 148.00($793m Aug 27) - BBG.

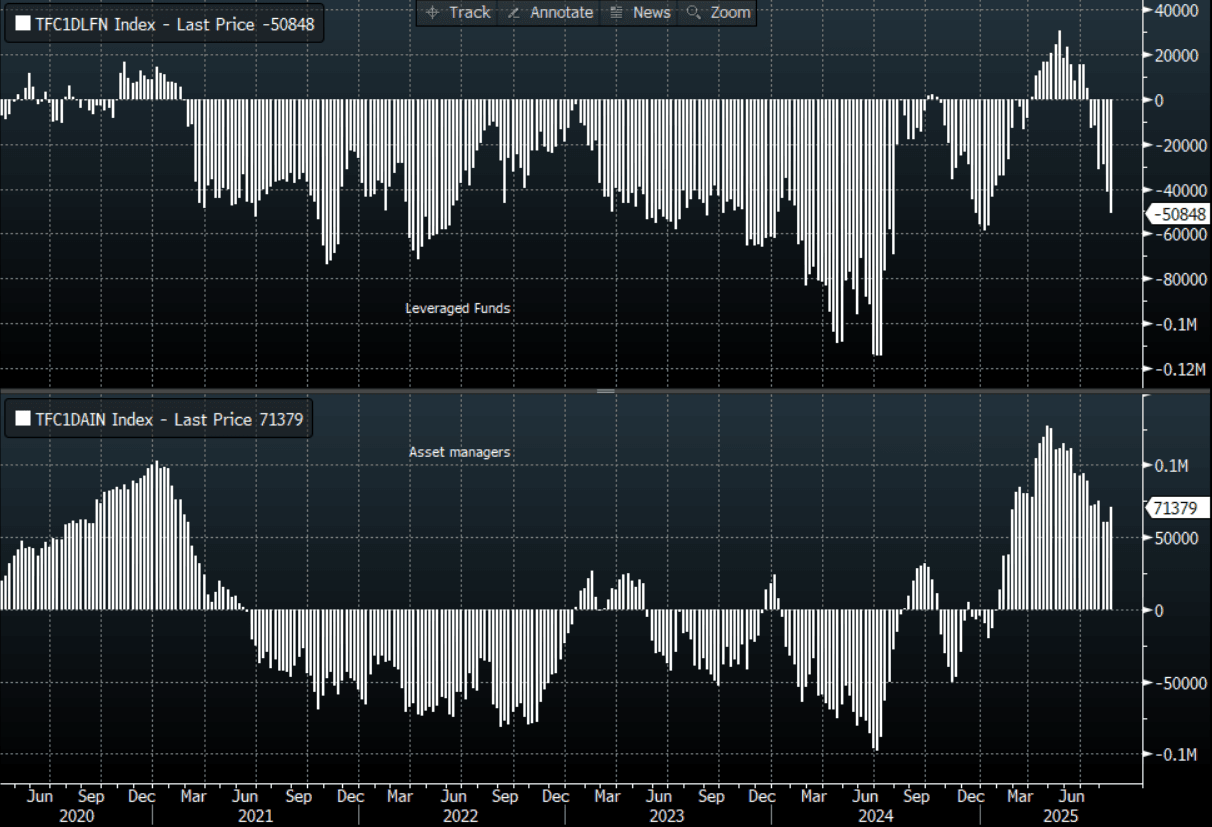

- CFTC data shows last week asset managers have begun to add to their JPY longs after a consistent period of reduction +71379( Last +60866), leveraged funds though again used the dip to add to their newly built short JPY position -50848(Last -41257).

- Data/Event : Leading Index, Dept. Store Sales

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD: NZD/USD - The Support Around 0.5800 Holds, Look For Sellers Towards 0.5900

The NZD/USD had a range Friday night of 0.5800 - 0.5876, Asia is trading around 0.5865. US equities roared higher and the USD reverted back to type and got hammered lower on the market's interpretation that Powell’s speech was dovish. I have read some differing views and not sure the speech was as clear cut as the market would like it to be, as we know the market is clearly more comfortable selling USD’s but lets see if this move can follow through this week. The NZD has bounced off its support around 0.5800 but I would still expect sellers to be lining up to fade any move back towards 0.5900/0.5950 initially. US Futures have opened slightly lower this morning, E-minis -0.05%, NQU5 -0.08%. CFTC Data looks at odds with price action after a dovish surprise last week from the RBZ.

- (Bloomberg) -- “The Reserve Bank of New Zealand's Governor Christian Hawkesby forecast further easing, warning of a "material possibility" that inflation could climb beyond 3%, the upper limit of the RBNZ's target range. The deeper the RBNZ cuts, the more likely that hikes — when the time comes — will be very aggressive, according to Stephen Toplis, head of research at BNZ Markets in Wellington.”

- “New Zealand retail sales likely fell last quarter as shoppers pulled back, raising the risk of another GDP slip.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6200(NZD355m Aug 27) - BBG

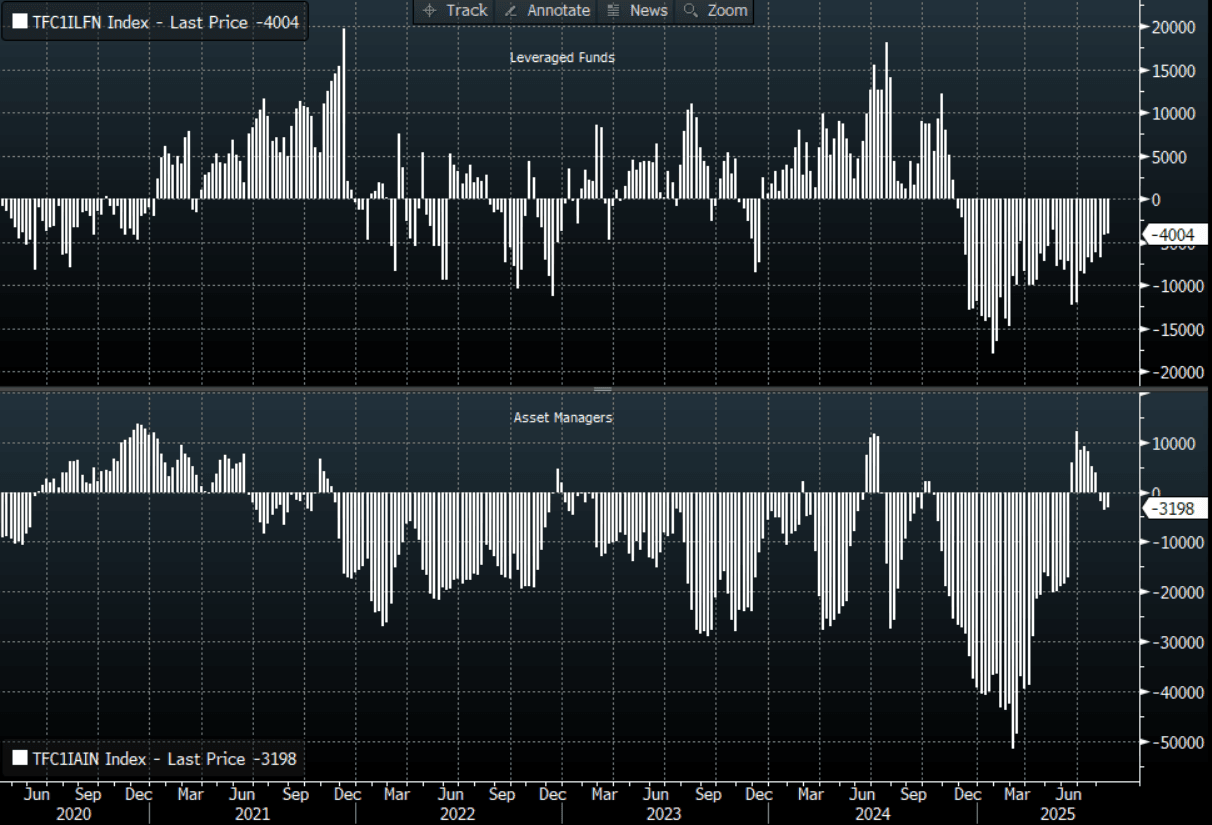

- CFTC Data of last week shows Asset Managers slightly reduced their new short position in the NZD -3198(Last -3679), the Leveraged community also reduced their own shorts slightly -4004(Last -4190).

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: Leveraged Investors Sold JPY, EUR, GBP, Asset Managers Bought - Per CFTC

In the week ending August 19th (last Tuesday), leveraged investors were net sellers of JPY, EUR and GBP, while asset managers were net buyers of these three currencies, see the table below.

- The trend for broader USD indices was a touch firmer to Aug 19 last week, although aggregate change versus prior week levels (Aug 12) were little changed.

- Friday's sharp move lower in the USD, as Fed Chair Powell struck a dovish tone, may have reflected leveraged investors selling the USD against the majors.

- In terms of outright positions in this space, EUR and GBP remain net long, while JPY is still a decent net short.

- On the asset manager side, contrasting trends played out, with these majors all bought against the USD in the week to Aug 19. JPY longs were the biggest addition, with outright longs for asset managers back above 71k.

- Elsewhere, shifts weren't dramatic. AUD shorts were added to by asset managers, but cut back marginally by leveraged investors. For CAD, net positioning didn't change much with leveraged investor sales offset by asset manager buying.

Table 1: CFTC Positioning Change & Outright Position By Major Currency

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -9591 | -50848 | 10513 | 71379 |

| EUR | -4704 | 9711 | 6081 | 397897 |

| GBP | -5783 | 25672 | 5408 | -67375 |

| AUD | 2303 | -7818 | -5455 | -72904 |

| NZD | 186 | -4004 | 481 | -3198 |

| CAD | -4036 | -35834 | 4577 | -65777 |

| CHF | 1985 | 262 | -1619 | -38699 |

| MXN | 5093 | 21791 | -7757 | 31034 |

Source: CFTC/Bloomberg Finance L.P./MNI