SWEDEN: Sep ETI: Sentiment Picking Up, Inflation Pressures Easing

Sep-24 08:07

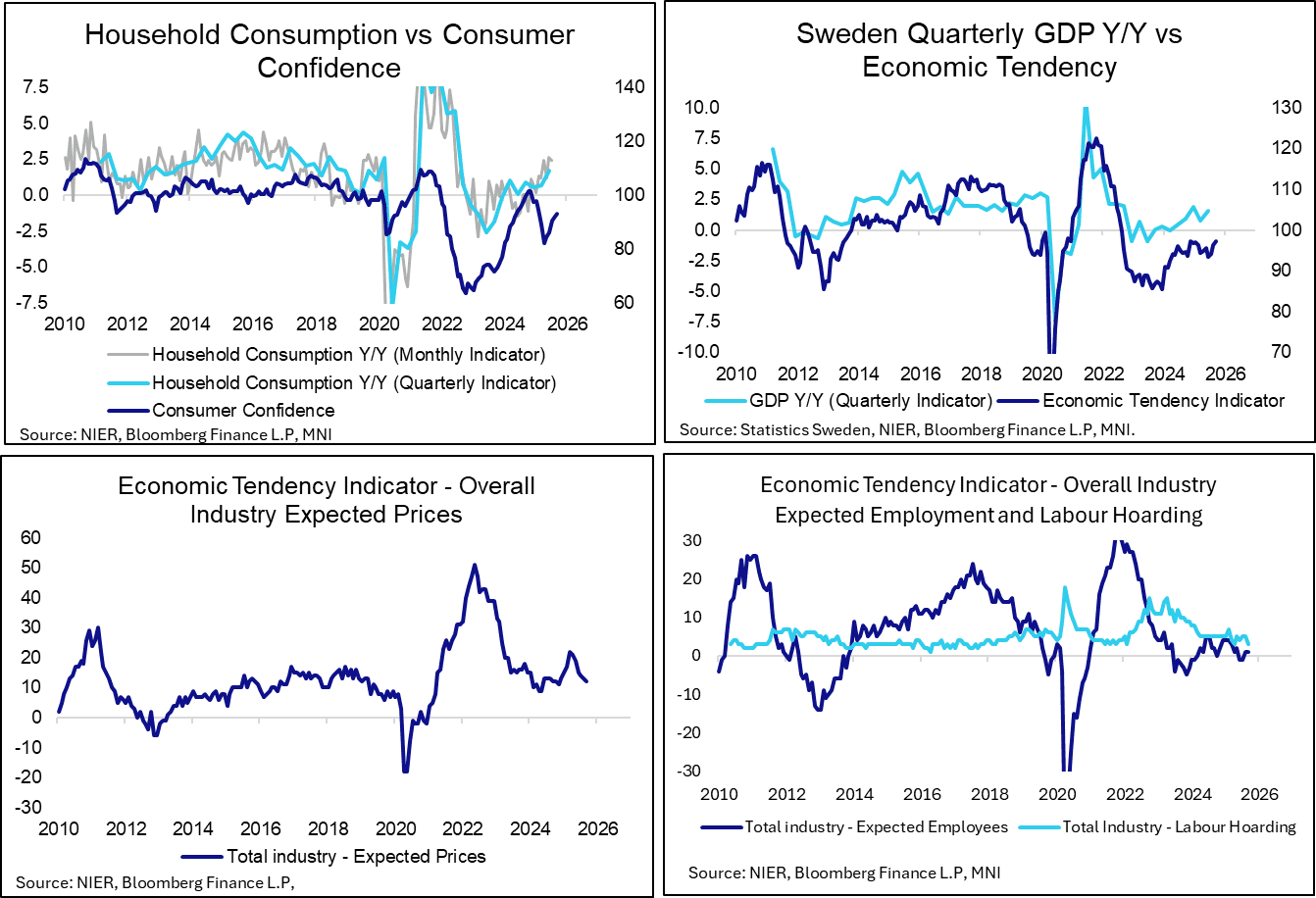

The Swedish Economic Tendency indicator rose to a year-to-date high of 97.2 in September (vs 96.3 prior). Increases were seen in consumer confidence, alongside the retail, construction and manufacturing sectors. Services sector confidence declined a little.

- Sentiment remains below the neutral 100 level, but the combination of another Riksbank rate cut and increased Government fiscal spending (with particular emphasis on households) should support further improvements ahead. Key for both institutions is whether this translates to better real consumer spending/economic activity outcomes.

- Barring an unexpected shock. the Riksbank’s easing cycle is likely over after yesterday’s 25bp cut to 1.75%.

- Consumer confidence rose for a fifth consecutive month to 93.2, up from a year-to-date low of 82.2 in April. Relative to August, the “Macro” index (consumer’s perceptions of general economic activity) rose to 97.6 (vs 94.8 prior) while the “Micro” index (consumer’s perceptions of their personal economic situations) rose to 90.5 (vs 89.0 prior).

- Business sentiment is strongest in the retail sector (106.5 vs 105.8 prior), after a brief dip below 100 in June. Other sectors remain below neutral.

- Expected prices continued to decline (diffusion index of 12 vs 13 prior and a YTD high of 22 in March), supporting the Riksbank’s assessment that the summer inflation rise was likely to be temporary.

- The expected employment diffusion index was steady at 1, while the labour hoarding index eased to 3 (vs 5 prior).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: GERMANY AUG IFO BUSINESS CLIMATE INDEX 89

Aug-25 08:00

- MNI: GERMANY AUG IFO BUSINESS CLIMATE INDEX 89

MNI EXCLUSIVE: China's equity market and economic impacts

Aug-25 07:54

- Advisors and analysts share their outlook on China's equity market and its economic impact.

- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

FOREX: Limited moves in G10 FX ahead of the IFO

Aug-25 07:48

- There is still very limited movement on this UK bank holiday Monday with the biggest mover in the G10 space AUDJPY (versus the USD the all G10 currencies are within 0.3% of Friday's close).

- The main scheduled event of the day will be the release of the German IFO survey at 9:00BST while we will hear from the Fed's Logan but not until 20:15BST (and it is unclear whether she will speak on monetary policy).

- It will be the second half of the week that we will see the main economic releases of the week with the second estimate of US Q2 GDP due Thursday. Friday will be a very busy data day with Tokyo CPI and flash HICP releases from France, Spain, Italy and Germany as well as July PCE from the US and Q2 GDP from Canada.

- Outside of G10 FX, USDCNH has seen more notable moves with the USDCNY fixing at the lowest level since early November and our Asia team noting that CNH was also helped by China property related equities have been buoyed on headlines of easing Shanghai home buying curbs. See our technical analysts' views above as the cross approaches key support.