MNI US OPEN - Payrolls Release Extremely Unlikely to Go Ahead

EXECUTIVE SUMMARY

- MNI'S GUIDE TO U.S. DATA RELEASES IN FEDERAL SHUTDOWN

- SENIOR GOVERNMENT OFFICIALS PRIVATELY WARN AGAINST FIRINGS DURING SHUTDOWN: WAPO

- DELAYS TO TRUMP’S U.A.E. CHIPS DEAL FRUSTRATE NVIDIA’S JENSEN HUANG: WSJ

- BOJ'S UEDA AVOIDS OCTOBER RATE HIKE SIGNAL

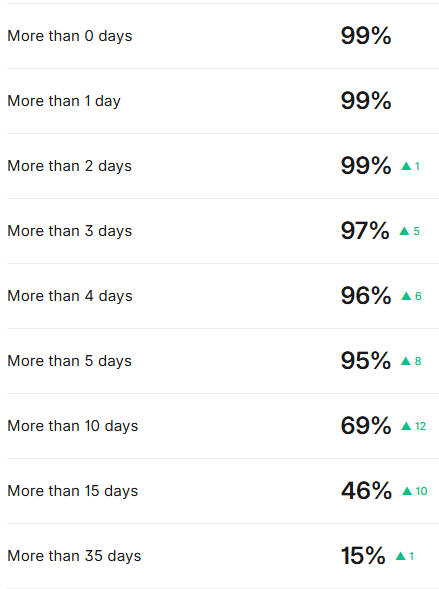

Figure 1: Kalshi odds see bettors favouring a shutdown of more than 10 days

Source: MNI / Kalshi

NEWS

US (Hidden PDF): MNI's Guide to U.S. Data Releases in Federal Shutdown

Today's payrolls print is extremely unlikely to go ahead - the BLS are formally in furlough, with all their 2054 full-time employees not working - this leaves just the acting BLS head in the office as they're presidentially appointed, and don't fall under federal funding. That said, there have been calls for the labor market report to be released regardless - Senator Elizabeth Warren has pressed for a full release despite the shutdown, while a Senate Banking Aide has confirmed the data has been collected for September and is likely ready for release.

US (WaPo): Senior Government Officials Privately Warn Against Firings During Shutdown

Senior federal officials have quietly counseled several agencies against firing employees while the government is shut down — as President Donald Trump has suggested he will — warning that the strategy may violate appropriations law, according to two people familiar with the matter who spoke on the condition of anonymity to discuss sensitive internal deliberations. The officials cautioned that firings — known as RIFs, or reductions in force — could be vulnerable to legal challenges under statutes labor unions cited this week in a lawsuit seeking to block threatened mass layoffs.

US (WSJ): Delays to Trump’s U.A.E. Chips Deal Frustrate Nvidia’s Jensen Huang

A multibillion-dollar deal to send Nvidia’s artificial-intelligence chips to the United Arab Emirates is stuck in neutral nearly five months after it was signed, frustrating Chief Executive Jensen Huang and some senior administration officials. The delays are a setback to Huang and White House AI Czar David Sacks, who hoped to see the deal advance quickly to highlight a new U.S. tech strategy focused on exports, according to people familiar with the matter. They see agreements like the U.A.E. deal as key to the U.S. staying ahead of China in the AI race.

US/MIDEAST (BBG): Hamas Says It Will Respond to Trump’s Gaza Plan ‘Very Soon’

A senior Hamas official said the Palestinian militant group will respond to US President Donald Trump’s plan to end the war in Gaza “very soon.” Deliberations between Hamas and other Palestinian factions as well as with mediators Qatar, Turkey and Egypt are ongoing, Mohammed Nazzal, a member of Hamas’s politburo, said to Qatar-based Al Jazeera TV in comments aired on Friday.

FRANCE (MNI): PM Renounces Article 49.3 in Gamble to Avoid Censure & Get Budget Approved

PM Sebastien Lecornu has renounced the use of Article 49.3 of the French Constitution in an effort to avoid an early censure motion and get a debate underway in the National Assembly on his 2026 draft budget law (PLF). Lecornu claims that "Since the government can no longer be in a position to interrupt the debates, there is therefore no longer any excuse for these debates not to start next week." Art 49.3 allows for the gov't to force through bills without a parliamentary vote, and indeed, recent Prime Ministers Elisabeth Borne, Michel Barnier, and Francois Bayrou have all utilised the provision over the past three years. Invoking Art. 49.3 brings the immediate risk of a censure vote against the minority gov't

ECB (BBG): Lagarde Says Knot Would Make a Good ECB President, ANP Reports

European Central Bank President Christine Lagarde said Klaas Knot would be a suitable successor, Dutch newswire ANP reported, citing a podcast episode of “College Leaders in Finance,” which will be released on Sunday. “I’ve known him for at least six years. He has the intellect, the stamina, and the ability to engage others,” Lagarde was cited as saying. Lagarde’s non-renewable term as ECB chief ends in October 2027. The task of an ECB president often involves aligning the members of the Governing Council, which comprises the heads of the euro area’s national central banks, Lagarde was cited as saying.

BOJ (MNI): BOJ's Ueda Avoids October Rate Hike Signal

Bank of Japan Governor Kazuo Ueda said Friday the central bank will raise its policy interest rate if the outlook for economic activity and prices materialises as expected, while stopping short of signaling an imminent move. “To determine whether economic activity and prices are improving, the Bank will, for the time being, monitor factors such as the points I mentioned -- namely, developments in the global economy, especially the U.S. economy; the impact of U.S. tariff policies on Japanese firms' profits and wage- and price-setting behavior; and price developments, including food prices,” Ueda told business leaders in Osaka.

BOJ (MNI): BOJ's Ueda Sees Small Behind-The-Curve Risk

The risk of the Bank of Japan falling behind the curve is limited, even as consumer prices remain elevated, Governor Kazuo Ueda told reporters in Osaka Friday. “We see as the baseline scenario that the drop in food prices caused by supply factors will continue. But if the pace of slowing food prices is more moderate, it could boost inflation expectations. We cannot rule out the risk, but the possibility isn’t high,” Ueda said.

BOJ (MNI INTERVIEW): Dec or Jan Hike More Likely - Ex-BOJ's Kameda

The BOJ's former chief economist shares his policy rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

JAPAN (MNI): Markets Odds Favor Koizumi Victory, Policy Uncertainty Remains Elevated

Japan's LDP leadership election is held tomorrow. Market expectations appeared skewed towards Shinjiro Koizumi (current Agriculture, Forestry and Fisheries Minister) being elected as leader of the party. Per Polymarket, his election odds sit over 80, against those of Sanae Takaichi, the other potential candidate. Her odds have tracked lower from earlier highs (last 12). In a recent interview with Nikkei, Shinjiro Koizumi says that "It is important for the government and the Bank of Japan to share the same overall direction", and that "the government's economic policy and the Bank of Japan's monetary policy will work together to realise a virtuous cycle in the economy."

RBA (MNI INTERVIEW): Stronger Q3 Inflation to Limit RBA Easing

The RBA's former head of international financial markets shares his cash rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

MNI POLITICAL RISK ANALYSIS: Czechia Election Preview

MNI's Political Risk team has published its latest Election Preview ahead of Czechia's legislative election on 3-4 October, with Prime Minister Petr Fiala’s centre-right governing coalition facing a major challenge amid a rise in support for nationalist and populist parties. In this preview, we offer a background briefing on the state of play in Czech politics, explanations on the electoral system for the Chamber of Deputies and the main parties and coalitions contesting the vote, election scenario analysis with assigned probabilities, analyst views, and a chart pack of opinion polling and betting market odds.

DATA

EUROZONE AUG PPI -0.3% M/M, -0.6% Y/Y (VS +0.3% M/M, +0.2% Y/Y JUL) (MNI)

EUROZONE DATA (MNI): September Services/Composite PMI: Flash Essentially Confirmed

- EUROZONE SEP FINAL SERV PMI 51.3 (51.4 FLASH, 50.5 AUG)

- GERMANY SEP FINAL SERV PMI 51.5 (52.5 FLASH, 49.3 AUG)

- FRANCE SEP FINAL SERV PMI 48.5 (48.9 FLASH, 49.8 AUG)

Cross-country development in the September services PMIs were broadly offsetting, meaning the Eurozone-wide release was only a shade lower than the flash at 51.3 (vs 51.4 flash, 50.5 prior). It's still the joint highest reading this year. We estimate the Germany/France services PMI at 50.2 (vs 49.5 prior), the first expansionary reading in eight months. Meanwhile, the ex-Germany/France index rebounded to 53.1 (vs 52.2 in August, 53.2 in July).

SPAIN DATA (MNI): Positive Domestic Demand Signals in September Services PMI

- SPAIN SEP SERVICES PMI 54.3 (53.3 FCAST, 53.2 AUG)

In contrast to Wednesday's weaker-than-expected September manufacturing PMI, the services PMI beat expectations. Services printed at 54.3 (vs 53.3 cons, 53.2 prior). This helped the composite reading beat expectations at 53.8 (vs 53.3 cons, 53.7 prior). There were positive signals for domestic demand in the services print, with an uptick in new orders coming despite reports of soft tourism demand (which could be a seasonal dynamic).

ITALY DATA (MNI): Services PMI Stronger Than Expected, Similar Themes to Spain

- ITALY SEP SERVICES PMI 52.5 (51.5 FCAST, 51.5 AUG)

In a similar fashion to Spain, the Italian September services PMI was stronger-than-expected, rising to 52.5 from 51.5 cons and prior. This helped the composite PMI remain steady at 51.7 after the manufacturing component disappointed on Wednesday. There were other similarities to the Spanish reading: Export new orders were weaker than domestic orders, while wage costs contributed to a rise in input (and thus output) prices.

FRANCE DATA (MNI): August IP M/M Underlying Categories Mixed; July Upward Revision

- FRANCE AUG IND PROD -0.7% M/M, +0.4% Y/Y (VS -0.1% M/M, +1.8% Y/Y JUL)

August France industrial production was weaker than expected at -0.7% M/M (0.3% consensus). However, this sequential underperformance was mainly due to an July upward revision to -0.1% (from a previous -1.1%; of that 1.0pp revision around 0.6pp was driven by transport with INSEE pointing towards "the integration of late responses in aeronautical and space construction" specifically).

SWEDEN DATA (MNI): Economic Activity Signals Are Improving After PMI Bounces

The Swedish composite PMI jumped to 57.1 in September, with August's reading also revised up to 54.2. This was driven by the services component, which rose to a 3-year high of 57.7 (vs 53.8 in August, 49.3 in July). There are good reasons to have expected an uptick in sentiment in September: The Government has presented an expansionary fiscal package focused on stimulating household consumption, while the Riksbank delivered another 25bp rate cut to bring the policy rate down to 1.75%.

NORWAY DATA (MNI): No Clear Signs of Labour Market Slack Building

Latest developments in the Norwegian labour market suggests Norges Bank's latest hawkish guidance remains intact. The SA registered unemployment rate from NAV was in line with consensus and Norges Bank projections at 2.1% in September (vs 2.1% prior). Whereas the volatile LFS unemployment rate has been rising through this year, the registered unemployment series has been very steady.

JAPAN DATA (MNI): Jobless Rate Pushes Up, Job to Applicant Ratio at Multi Year Lows

The Japan August jobless rate rose more than forecast. It printed at 2.6% against a 2.4% forecast (while the July outcome was 2.3%). The 0.3ppt rise in m/m terms is notably, although it only takes us back to 2024 highs for the jobless rate. The job to applicant ratio eased to 1.20 form 1.22 in July (the market consensus had been for an unchanged 1.22 outcome).

TURKEY DATA (MNI): Significant Jump in Monthly Inflation Threatens CBRT Easing Plans

- TURKEY SEP CPI +3.23% M/M

Consumer prices rose 3.23% m/m in September, well above expectations of a more moderate +2.58% rise (Prior: +2.04). That translates to a +33.29% year-on-year print, above last month’s +32.95% reading and expectations of a moderation to +32.45%. Among the CPI subcategories, ‘Education’ prices recorded the highest annual increase, rising 66.10% y/y, followed by ‘Housing’ prices at 51.36% y/y. Given the start of the school season in September, strong price increases across education and transport prices had been anticipated - the +17.90% m/m increase in education stands out in September (clothing and transport prices rose 3.92% and 2.81%, respectively, on a monthly basis). Meanwhile, adverse weather conditions were also expected to keep food prices elevated.

RATINGS: Updates on the EU & Slovenia Due After the Close

Potential rating reviews of note scheduled for after hours on Friday include:

- Fitch on Slovenia (current rating: A; Outlook Positive)

- Moody’s on the European Union (current rating: Aaa; outlook stable)

FOREX: USD/JPY Firms Off Support as Ueda Not Swayed on Hike Pressures

- The USD Index trades on the back foot early Friday, fading against all others in G10 outside of the JPY. The BoJ Chair Ueda pressured the currency by stopping short of endorsing an imminent rate hike in Japan, instead reiterating the bank's guidance from their most recent meeting, despite the solid Tankan manufacturing survey data from earlier this week. Instead, Ueda affirmed the Bank would be observing and monitoring incoming datapoints to assess the October decision, for which markets see a roughly 50/50 chance of a 25bps rate hike.

- USDJPY has recovered from Wednesday's low. Recent weakness resulted in a clear breach of the 50-day EMA. This continues to signal scope for a deeper retracement and exposes the key short-term pivot support at 145.49, the Sep 17 low.

- A bull cycle in USDCAD remains intact and yesterday's break above the late September's high, firms the bullish theme. This move higher also maintains the

bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend.

Sights are on 1.4019, a Fibonacci retracement point. - Today's payrolls print is extremely unlikely to go ahead - the BLS are formally in furlough - leaving focus on alternative economic data and it remains possible that proxies for initial jobless claims can be compiled using state-by-state data - but these will likely be patchy and come heavily caveated. ISM services index data today will go ahead as usual and could be a more market-moving event as a result.

EGBS: Bund Futures Trading in a Tight Range With US Shutdown Dampening Vol

Bund futures are little changed at 128.65, trading in a very tight 13 tick range on lighter-than-usual volumes. The ongoing US Government shutdown, which is very likely to prevent today’s scheduled NFP release from going ahead, is continuing to dampen rates vol. Meanwhile, regional data and political/fiscal headline flow hasn’t done much to change the outlook or move markets.

- German yields are up to 1bp higher, with the curve lightly bear flattening. 10-year yields remain comfortably within the 2.60-2.80% range that has contained price action since the start of summer. Meanwhile, 5s30s is down another 1.6bps at 96bps.

- The EUR 10s30s swap curve is little changed at 25bp after steepening over the past couple of sessions in the wake of headlines surrounding the Dutch pension fund transition towards a defined contribution system. Cycle closing highs at 28.2bp remain unchallenged.

- 10-year EGB spreads to Bunds are up to 1bp narrower on the session, with no material outperformance for any one semi-core/peripheral country's bonds.

- Cross-country development in the September services PMIs were broadly offsetting, meaning the Eurozone-wide release was only a shade lower than the flash at 51.3 (vs 51.4 flash, 50.5 prior). Meanwhile, Eurozone August PPI was a little weaker than expected at -0.3% M/M (vs -0.1% cons, 0.3% prior).

- Further details of the Italian fiscal outlook are filtering through, with Q2 fiscal data having also been released this morning. Meanwhile, French PM Lecornu has renounced the use of Article 49.3 in trying to get a budget passed through the National Assembly.

GILTS: Off Lows After Services PMIs, Q4 Rate Cut Odds Still Look Too Low

Gilts have recovered from session lows since a mark lower in the final services PMI data, but moves were modest. Futures last at session highs, +16 at 90.95, just off fresh session highs.

- Bears remain in technical control, initial support and resistance still located at 90.26 & 91.28.

- Yields ~1.5bp lower across the curve, steepening technical trends remain intact.

- 10s trade in the middle of the 4.60-4.80% closing range in play since mid-August.

- Fiscal headlines continue to reaffirm already known risks surrounding productivity forecast downgrades triggering further UK fiscal deterioration. There isn’t much in the way of fresh meaningful details within the stories.

- A reminder that NIESR director Aikman told us that the government needs to not only start running budget surpluses to keep debt-to-GDP steady but must come up with a credible strategy to get it on a downward trajectory, adding that markets will be disappointed if this is lacking from the upcoming budget.

- GBP STIRs a touch more dovish since the PMIs, SONIA futures last flat to +3.0.

- BoE-dated OIS still shows under 5bp of easing through year-end, with the next 25bp move not fully discounted until the end of the April MPC.

- We still think that the market underappreciates the odds of a Q4 cut.

- BoE Governor Bailey will discuss “Macro-financial stability in a fragmenting world” from 14:20 London today.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Nov-25 | 3.960 | -0.7 |

Dec-25 | 3.921 | -4.7 |

Feb-26 | 3.812 | -15.5 |

Mar-26 | 3.778 | -18.9 |

Apr-26 | 3.696 | -27.1 |

Jun-26 | 3.669 | -29.8 |

Jul-26 | 3.617 | -35.0 |

Sep-26 | 3.601 | -36.6 |

EQUITIES: Eurostoxx 50 Remain Bullish After Recent Break of Key Resistance

Eurostoxx 50 futures maintain a bullish theme. This week’s gains have resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Initial firm support is 5525.00, the Aug 22 high. A bull cycle in S&P E-Minis remains intact. The contract has traded to a fresh cycle high this week to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6787.63, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6675.82. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6558.72.

- Japan's NIKKEI closed higher by 832.77 pts or +1.85% at 45769.5 and the TOPIX ended 41.77 pts higher or +1.35% at 3129.17.

- Across Europe, Germany's DAX trades higher by 35.12 pts or +0.14% at 24455.94, FTSE 100 higher by 47.37 pts or +0.5% at 9475.29, CAC 40 up 23.98 pts or +0.3% at 8079.92 and Euro Stoxx 50 up 8.42 pts or +0.15% at 5654.05.

- Dow Jones mini up 99 pts or +0.21% at 46902, S&P 500 mini up 17.5 pts or +0.26% at 6784, NASDAQ mini up 69.5 pts or +0.28% at 25180.25.

Time: 10:00 BST

COMMODITIES: WTI Futures Breach Bear Trigger and Key Support

WTI futures have pulled back from their recent highs. Yesterday's sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens a bearish theme and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. A break of this level would highlight a reversal. A bull cycle in Gold remains in play. The yellow metal has traded to a fresh cycle high this week, confirming a resumption of the primary uptrend. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3909.4, a Fibonacci projection. On the downside, support to watch lies at $3715.0, the 20-day EMA. A pullback would be considered corrective.

- WTI Crude up $0.84 or +1.39% at $61.29

- Natural Gas down $0.02 or -0.7% at $3.417

- Gold spot up $8.53 or +0.22% at $3865.26

- Copper up $5.9 or +1.19% at $500.75

- Silver up $0.43 or +0.92% at $47.431

- Platinum up $9.08 or +0.58% at $1585.82

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 03/10/2025 | 1000/0600 | NY Fed's John Williams | ||

| 03/10/2025 | 1230/0830 | *** | Employment Report | |

| 03/10/2025 | 1320/1420 | BOE Bailey Keynote At Knot Farewell Symposium | ||

| 03/10/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/10/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/10/2025 | 1350/1550 | ECB Schnabel In Panel At Knot Farewell Symposium | ||

| 03/10/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/10/2025 | 1740/1340 | Fed Vice Chair Philip Jefferson |

Note: Due to U.S. government shutdown, some data may be unavailable.