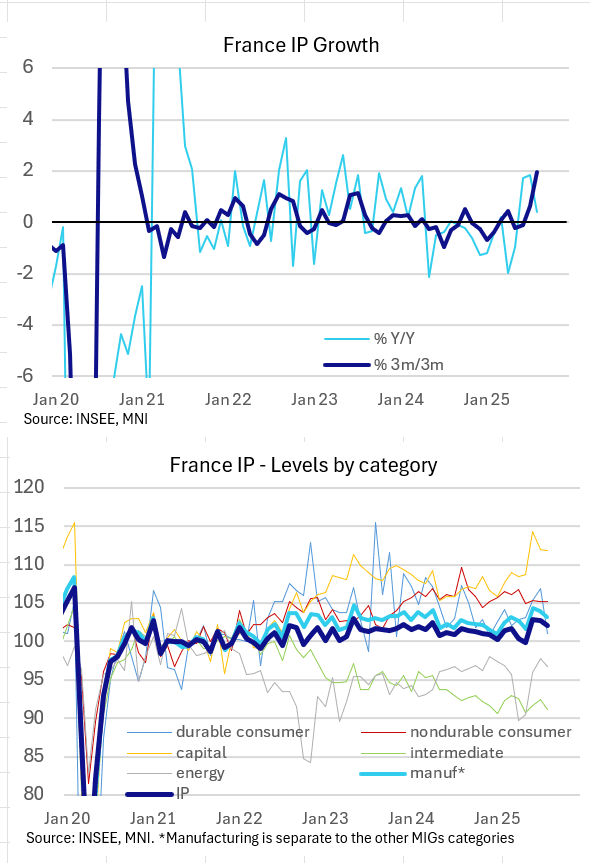

FRANCE DATA: August IP M/M Underlying Categories Mixed; July Upward Revision

August France industrial production was weaker than expected at -0.7% M/M (0.3% consensus). However, this sequential underperformance was mainly due to an July upward revision to -0.1% (from a previous -1.1%; of that 1.0pp revision around 0.6pp was driven by transport with INSEE pointing towards "the integration of late responses in aeronautical and space construction" specifically).

- Underlying manufacturing decreased by 0.7% M/M (0.3% cons consisting of 3 analysts; -0.5% prior, revised from -1.7%). On a 3m/3m comparison, the sector remains strong at 1.9% (0.6% prior). While this is mainly due to the very strong data from June, manufacturing is still up 1.1% versus its average level for the first five months of 2025, INSEE comments.

- Across manufacturing categories, chemicals (-1.9% M/M), metals (-0.9% M/M), and electronics equipment (-6.0%) were weak, while IT equipment (5.0%) and the "other industrials" category (1.8%) offset some of that.

- Production in construction meanwhile accelerated in August (1.2% M/M vs 0.6% in July), while energy production was -1.0% M/M (+1.9% prior).

- On a yearly comparison, IP was 0.4% (0.6% cons, 1.8% prior, revised from 1.3%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ITALY DATA: August Services/Composite PMI: Still Expansionary But Momentum Slows

In a similar fashion to Spain, the Italian August services PMI was somewhat weaker-than-expected, but still expansionary, at 51.5 (vs 52.1 cons, 52,3 prior). The composite reading was above 50 for the seventh consecutive month at 51.7 (vs 51.6 cons, 51.5 prior).

The details of the report point to weakening momentum amongst services producers in August, with growth still supported by domestic markets. Despite a rise in input costs, the report noted limited passthrough into output charges.

Key notes from the release:

- “Where panel members saw growth in output, they attributed this to recent new customer introductions and order inflows. The upturn was reportedly curbed by challenging economic conditions, however.”

- “As has been the case since February, the sustained upturn in new orders remained bolstered by the domestic economy, as export sales fell again in August.”

- “Service providers continued to add to their payroll numbers midway through the third quarter.”…“ The rate of workforce expansion was the least marked in four months”

- “Despite a stronger influx of new orders, prices charged for the provision of Italian services rose to the weakest extent in nine months in August. With only 7% of firms hiking their rates, the overall rate of charge inflation was only modest overall.”

- “In contrast, input costs rose at a sharper pace on the month. The rate of inflation was both rapid and historically elevated, though it was softer than those seen earlier in the year.”

MNI: GERMANY AUG SERV PMI 49.3 (50.1 FLASH, 50.6 JUL)

- MNI: GERMANY AUG SERV PMI 49.3 (50.1 FLASH, 50.6 JUL)

EGB SYNDICATION: Lithuania Long 10 / 20-year LITHUN: Books open

Long 10-year:

- Guidance: MS+105bp area

- Size: EUR benchmark (MNI pencils in E1bln)

- Maturity: 10 March 2036

- Coupon: Short first

- ISIN: XS3175946071

20-year:

- Guidance: MS+145bp area

- Size: EUR benchmark (MNI pencils in E1bln)

- Maturity: 10 September 2045

- ISIN: XS3175947046

For both:

- Bookrunners: Erste Group, HSBC and Societe Generale

- Settlement Date: 10 September 2025 (T+5)

- Timing: Books open, today's business

From market source / MNI colour