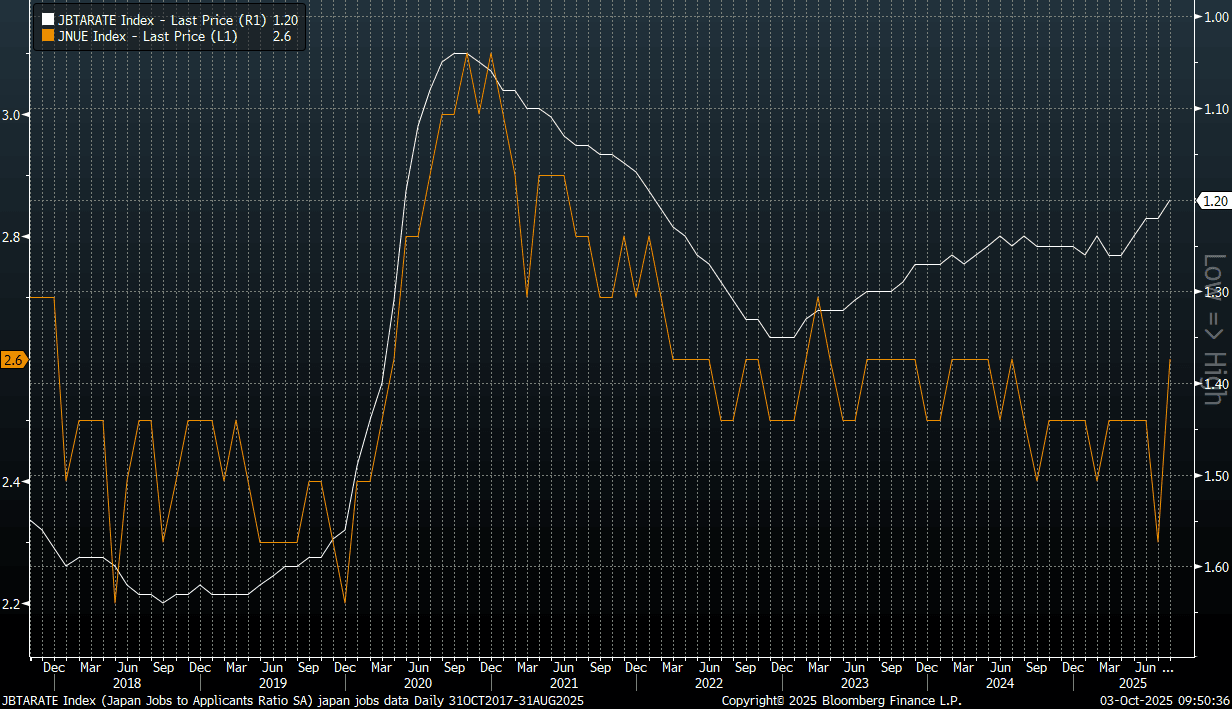

JAPAN DATA: Jobless Rate Pushes Up, Job To Applicant Ratio At Multi Yr Lows

The Japan August jobless rate rose more than forecast. It printed at 2.6% against a 2.4% forecast (while the July outcome was 2.3%). The 0.3ppt rise in m/m terms is notably, although it only takes us back to 2024 highs for the jobless rate. The job to applicant ratio eased to 1.20 form 1.22 in July (the market consensus had been for an unchanged 1.22 outcome).

- The chart below plots the job to applicant ratio (the white line), which is inverted on the chart, against the jobless rate. This is the lowest level for the job to applicant ratio since early 2022. There has been some divergence between the two series, with the job to applicant ratio generally painting a softer labor market picture in recent months. That wedge has now moderated to some degree.

- Job offers were down 3.6% in y/y terms, while new job offers fell by 6.2%y/y. The new jobs to applicant ratio fell to 2.15, just above recent lows.

- The number of people employed fell by 210k in m/m terms.

- The data points to some softening in labor market conditions, which at the margin may temper Oct hawkish BOJ expectations. Still, the jobless rate is low from an historical standpoint and therefore may still continue to support wage gains.

Fig 1: Japan Jobless Rate (Orange Line) & Job To Applicant Ratio (White Line, Inverted)

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Bear Threat Remains, Global & Local Factors Weighing

JGB futures finished up post Tokyo trade at 137.30 on Tuesday, -.22 versus settlement levels. Global back end futures were weaker on Tuesday amid on-going fiscal concerns, while fresh political uncertainty in Japan was another headwind for local futures.

- From a technical standpoint, a bear threat in JGB futures remains present and the contract is trading closer to its recent lows. A resumption of weakness would signal scope for an extension towards 136.57, a Fibonacci projection.

- Late yesterday, via BBG: "Japanese Prime Minister Shigeru Ishiba’s key power broker within the ruling party said he’ll quit if Ishiba approves, weakening Ishiba’s standing within his party and possibly starting a string of resignations at risk of reaching the prime minister himself."

- Fresh fiscal uncertainty will likely bias the JGB curve steeper. The 2/30s curve ended yesterday near +236bps. The outright 10yr JGB yield ended at 1.62% yesterday.

- In the swap space, the 10yr rate was last near 1.445%.

- On the data front today, we just have August final reads for the services and composite PMI prints.

- Note tomorrow sees a 30yr debt sale, another test for sentiment, after yesterday's 10yr sale went smoothly.

GOLD: Gold Holds Gains Above $3500 As Watches Fed Developments

Gold prices rose further on Tuesday helped by weaker risk appetite but despite a stronger US dollar (BBDXY +0.5%) and higher yields. They were up 1.6% to $3533.16/oz after a new record of $3540.04 driven by Fed rate cut expectations and continued concerns over its independence. US manufacturing data printed slightly below expectations adding to the rally. The ruling on the removal of Governor Cook from the FOMC has been delayed to Thursday to allow the Justice Department more time for its submission.

- Gold is currently around $3527.8, just below resistance at $3539.7. The break above key resistance at $3500.1 confirms a resumption of the uptrend.

- Silver was 1.6% stronger at $40.883 off the intraday low of $40.142 and 2.9% higher this week. It is trading now around $40.88. With the trend remaining bullish, resistance to watch is $41.064.

- Equities were weaker with the S&P down 0.7% and Euro stoxx -1.4% but the S&P e-mini has started today up 0.1%. Oil prices were higher with WTI +1.6% to $65.62/bbl. Copper rose 1.1%.

AUSSIE BONDS: Futures Steady, Focus Remains On 10yr Downside, Q2 GDP Later

Aussie bond futures are little changed in the first part of Wednesday dealings. 3yr futures (YM) were last at 96.54, against yesterday's intra-session low of 96.515, which was a fresh low back to early August. 10yr futures (XM) hit fresh lows of 95.575 in earlier trade, but we sit back at 95.61 in latest dealings.

- Given global weakness in back end futures from Tuesday, 10yr futures in Australia may remain the focus point. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

- The US Treasury cash curve bear steepened in the return from the Labor Day weekend Tuesday, taking the lead of global peers and shrugging off soft US data. The early impetus in US Tsy futures this morning is a slightly stronger bias.

- In the cash Aussie government bond space, the early impetus is for a steeper curve, but aggregate moves are modest. The 3yr yield last near 3.44%, while the 10yr was close to 4.36%.

- On the data front, the final August PMI reads for the S&P Global services and composite PMI readings were firmer. Services printed at 55.8 against a 54.1 July read.

- Q2 GDP prints today and Bloomberg consensus is forecasting a 0.5% q/q increase bringing annual growth to 1.6% from Q1's 1.3%, in line with the RBA's August projection. However, almost all estimates were provided before this week's inventory, net export and public demand data. Inventories were close to consensus and net exports were in line.

- Also noted "Reserve Bank of Australia Governor Michele Bullock delivers an economics lecture in Perth." - BBG (which will be at 6pm AEST).