JAPAN: Markets Odds Favor Koizumi Victory, Policy Uncertainty Remains Elevated

Japan's LDP leadership election is held tomorrow. Market expectations appeared skewed towards Shinjiro Koizumi (current Agriculture, Forestry and Fisheries Minister) being elected as leader of the party. Per Polymarket, his election odds sit over 80, against those of Sanae Takaichi, the other potential candidate. Her odds have tracked lower from earlier highs (last 12).

- In a recent interview with Nikkei, Shinjiro Koizumi says that "It is important for the government and the Bank of Japan to share the same overall direction", and that "the government's economic policy and the Bank of Japan's monetary policy will work together to realise a virtuous cycle in the economy."

- Koizumi is seen as more of a centralist relative to Takaichi, who is a fiscal/BOJ dove (although has softened her BOJ stance).

- Still, Koizumi will look to pass the supplementary budget for 2025 as soon as possible if he wins the election (per Nikkei). This would be aimed combating inflation for households. Given the LDP doesn't have a majority in either house, coalition partners will be needed.

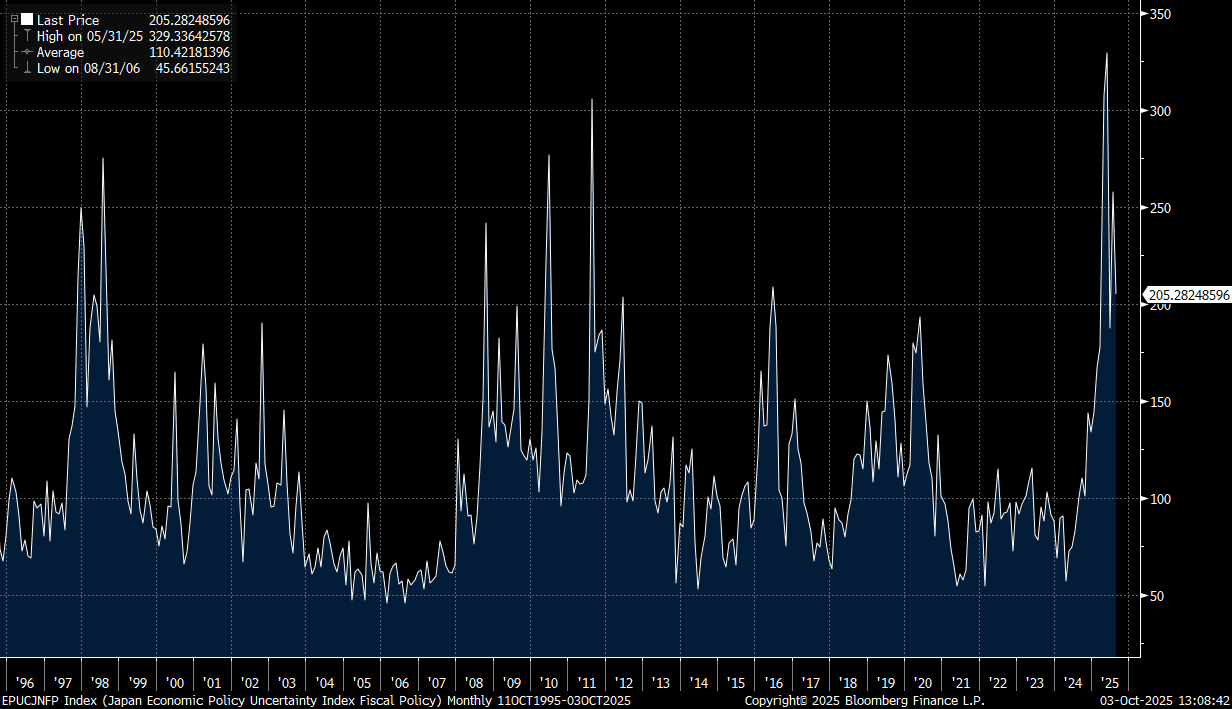

- This is likely to see fiscal policy uncertainty remain elevated to some degree. The chart below plots Japan economic policy uncertainty related to fiscal policy. We are off highs but still quite elevated from an historical standpoint. There is some relationship between such uncertainty and the shape of the JGB yield curve.

- The 2/30s JGB curve is off highs, but remains above +220bps, so still elevated from an historical standpoint. It may be markets are already factoring in a Kozimui victory to some extent.

- On the FX side, similar arguments could be made for USD/JPY, although this pair is up 0.30% so far today, last near 147.75, putting it above its 50-day EMA. Little commitment to an Oct hike by BoJ Governor Ueda earlier today has weighed on yen.

- J.P. Morgan note re the election around yen risks: "That the FX market currently appears to be pricing in little “Takaichi risk” suggests that the possibility of JPY-selling following a Takaichi victory could be relatively large, but...compared to last September, Takaichi is seen as less opposed to the BoJ hikes, which should limit JPY-selling. On net, if Takaichi wins, we think the knee-jerk USD/JPY rally is likely to be similar to or less than the+1% rise seen after the 1st round vote in last September’s presidential election. Since a victory by Koizumi (or Hayashi) seems to be largely expected by market participants, the knee-jerk JPY-buying in this case is likely to be much smaller than when Ishiba unexpectedly reversed the outcome in the 2nd round vote last year. "

Fig 1: Japan Fiscal Policy Uncertainty - Off Highs But Still Elevated

Source: Bloomberg Finance L.P/MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

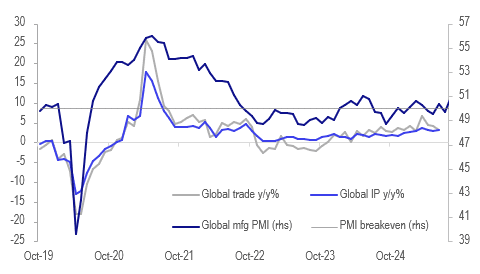

GLOBAL MACRO: Indicators Suggest Global IP Growth Continued In Q3

The August JP Morgan global manufacturing PMI printed at 50.9 up from 49.7 signalling growth in activity in the sector again and at its fastest since May 2024. The pickup was driven particularly by higher output but also domestic orders and a return to hiring but confidence remained below average. The PMI, LME metal prices and the Baltic Freight Index (BFI) are all consistent with global IP and trade growth remaining at current rates or possibly improving.

Global growth

Source: MNI - Market News/LSEG/Bloomberg Finance L.P.

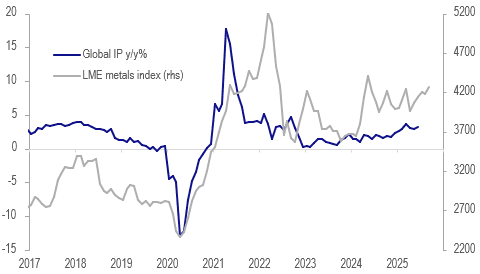

- CPB global IP growth rose 0.4% m/m in June driving a 0.4pp improvement in annual growth to 3.2% y/y, the strongest since March which was boosted by the frontloading of deliveries to the US ahead of tariff deadlines. June global trade rose 3% y/y down from 4.1% y/y.

Global IP y/y% vs LME metals

- August output in the JP Morgan PMI rose to 51.7 from 49.7 helped by orders up 1.1 points to 50.9. All sectors saw growth. However the increase was driven by domestic demand and export orders continued to contract but at a slower rate but tariff worries remained a problem, according to JP Morgan.

- The increase in demand likely drove an improvement in employment with it marginally returning to growth territory at 50.2.

- The resumption of output growth in manufacturing was also across most countries with only 5 continuing to see contraction. India, Thailand, Spain and the US saw strong growth.

- Cost inflation rose to its highest rate since February driving a marginal pickup in selling price inflation with the US reporting the fastest rate.

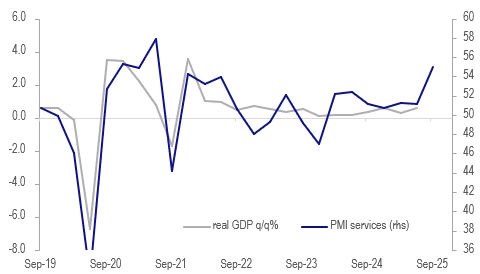

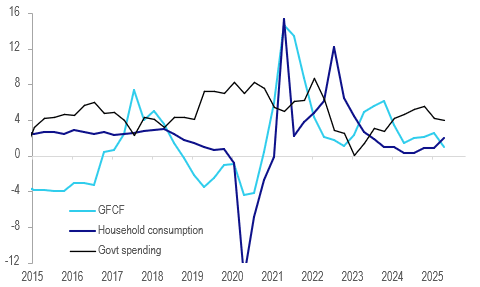

AUSTRALIA DATA: Q2 Boosted By Special Factors, H1 Averaged 0.4% q/q

Q2 GDP was stronger than both the RBA and consensus expected as it rebounded from Q1’s weather-impacted soft result and benefited from holidays. It rose 0.6% q/q to be up 1.8% y/y, the strongest since Q3 2023, after 0.3% q/q & 1.4% y/y in Q1. Growth was driven by private and public consumption with net exports adding 0.1pp while both inventories and investment detracted. Given the RBA’S cautious stance towards easing and recent stronger data, a September rate cut looks unlikely and November will depend on new information and the outlook.

- The S&P Global PMI improvement over Q3 suggests growth may have improved further at the start of H2. The August composite rose to its highest since February 2022.

Australia GDP q/q% vs S&P Global PMI services

- Household consumption contributed 0.45pp to GDP as it rose 0.9% q/q to be up 2% y/y, the highest in 2 years, which was supported by a 1pp fall in the savings rate to 4.2%. Nominal disposable income rose 0.6% q/q.

- The ABS notes that the close proximity of Anzac Day to Easter boosted holiday-related spending. Also end of financial year discounting encouraged discretionary spending which rose 1.4% q/q.

- Government spending contributed 0.2pp to growth as it increased 1.0% q/q to be up 4% y/y driven by a strong increase in benefits paid and health expenditure as well as election and defence spending.

- Investment was lacklustre across the board with it detracting 0.2pp driven by the public sector with private capex neutral.

- Net exports made its strongest contribution to GDP in two years. Exports rose 1.7% q/q to be up 1.5% y/y, while imports increased 1.4% q/q & 1.9% y/y, a sign of improving domestic demand.

- GDP/person rose 0.2% q/q to be up 0.2% y/y, the first annual rise since Q1 2023.

Australia domestic demand y/y%

Source: MNI - Market News/ABS

CHINA PRESS: China To Exempt Taxes For Capital Replenish Social Security Fund

China has transferred part of its state-owned capital to replenish the social security fund, and introduced tax exemption to support the transfer, Yicai.com reported. To avoid additional tax burden during the transfer process, the transferred state-owned equity and cash income will be exempted from value-added tax, corporate income tax and stamp duty, and the implementation date is retroactive to Apr 1, 2024 with taxes paid before to be refunded, according to a document by the Ministry of Finance Tuesday.