MNI US MARKETS ANALYSIS - BoE Imminent; Heavy Fedspeak

Highlights:

- BoE decision imminent, we see 50/50 risks between cut and a hold

- Challenger layoffs data paint poor picture of labor market

- Heavy Fedspeak schedule should take focus Thursday

US TSYS: Challenger Sees Move Off Lows But Key TYA Support Still Exposed

- Treasuries have pared some of yesterday’s sizeable sell-off after a sharp increase in forward-looking Challenger job cut announcements went against yesterday's stronger than expected ADP and ISM Services readings.

- Today sees data focus on further labor indicators, heavy Fedspeak and government shutdown considerations after some recent optimism on a near-term re-opening yesterday.

- There could also be near-term spillover from an undecided BoE decision shortly at 1200ET.

- Cash yields are 1.5-2.8bp lower on the day, led lower by 3s.

- TYZ5 trades at 112-16 (+05+) on solid overnight volumes of over 400k.

- It lifts off yesterday’s low of 112-09+ but a key support remains exposed. It stopped just shy of support at 112-08+ (38.2% retrace of May-Oct upleg) with sights set on a reversal trigger at 112-06 (Sep 25 low and 100-dma).

- Data: Revelio labor statistics (0830ET), Chicago Fed labor indicators (0830ET), Dallas Fed weekly economic index (1130ET), NFIB small business jobs report (1300ET), State-level jobless claims (~1700ET)

- Fedspeak: Goolsbee, Williams, Barr, Hammack, Waller, Paulson and Musalem all speaking today – see our separate guide to it below.

- Bill issuance: US Tsy $110B 4W, $95B 8W bill auctions (1130ET)

- Politics: Trump makes an announcement (1100ET), Trump participates in multilateral meetings with Central Asian Countries (1800ET) before dinner (1900ET)

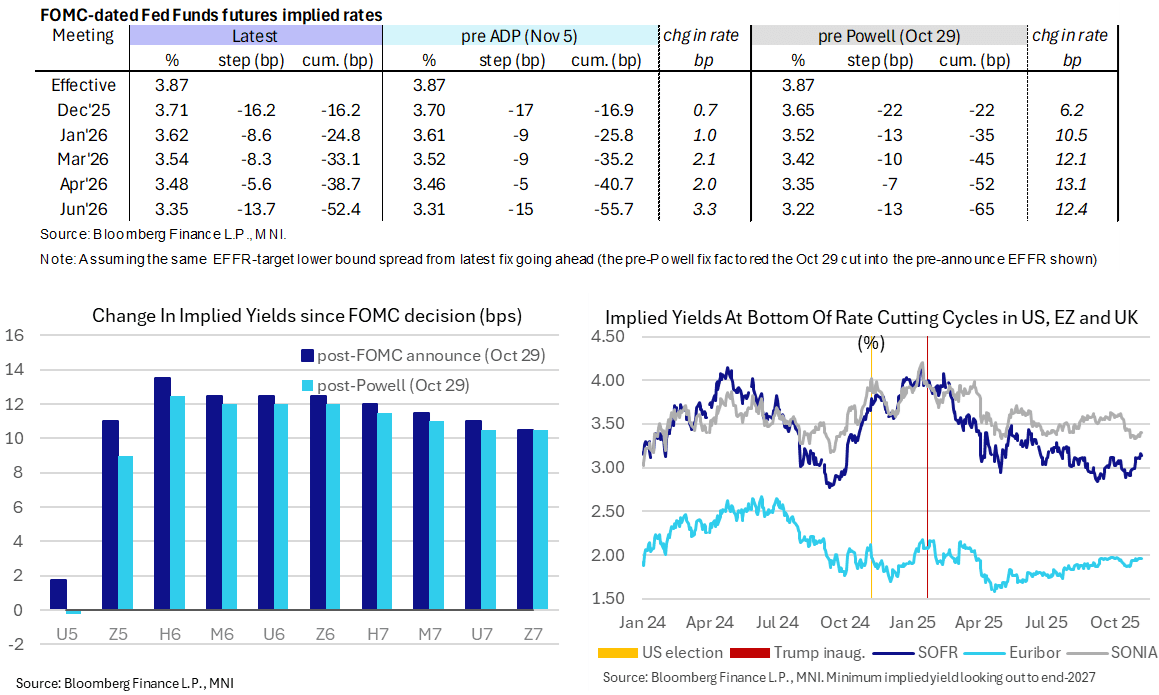

STIR: Challenger Layoff Spike Pares ADP and ISM Services Beats

- Fed Funds implied rates are 1.5-2.5bp lower overnight for meetings out to mid-2026 on the back of an early release of the October Challenger jobs report with its sharp rise in layoffs.

- It chips away at yesterday’s hawkish adjustment on slightly higher than expected ADP print before a clearer beat for ISM services.

- Cumulative cuts from 3.87% effective: 16bp Dec, 25bp Jan, 33bp Mar, 38.5bp Apr and 52.5bp Jun.

- SOFR futures are broadly 2-3 ticks higher looking out to end-27.

- That includes the terminal yield dipping 2.5bp to 3.135% after yesterday’s 6bp climb to 3.16% for its highest close since late July.

- Today sees a heavy Fedspeak schedule (see a guide to it just above) plus labor indicators from Revelio Labs, the Chicago Fed and NFIB before state-level jobless claims later in the afternoon.

- There could also be spillover from the BOE decision at 1200ET where we see a 50/50 likelihood of a 25bp cut or hold.

FED: A Guide To Today’s Fedspeak Deluge

Today sees a particularly heavy schedule for Fedspeak. Williams (leaning dove), Barr (leaning hawk), Paulson and Musalem (hawk) all are set to give their first appearance since last week’s FOMC meeting, perhaps helping flush out a range of views on December rate cut prospects after Powell noted a strongly divided committee. One area we’ll watch for is any softening in stance on the labor market after this morning’s sharp rise in Challenger layoffs, perhaps most notable if it comes from hawks Hammack and (after the close) Musalem.

- 0830ET – Goolsbee (’25, dove) on CNBC (and again on Newsmax at 1620ET). He said on Monday that he sees a higher bar for deciding to cut rates in December than in October. "I'm not decided going into the next meeting. I want to see how things are playing out." But he also points to potential for rates to come down "a fair amount".

- 1100ET – NY Fed Williams (voter) speaks in Frankfurt (text + Q&A). He signalled in a Sep 29 Q&A that he would be supportive of further rate cuts, saying "from my perspective, monetary policy has been and continues to be what we call restrictive." We think he's one of the 9 (of 19) FOMC members who is penciling in a total of 3 cuts by end-2025, including the one delivered last month.

- 1100ET – Gov. Barr (voter) in moderated discussion (no text). His Oct 9 speech appeared to confirm MNI's assumption that he was the most hawkish of the 8 permanent voters on the FOMC as of the September meeting. He’s probably one of the 7 on the 19-member FOMC who don't see further cuts this year, and the only permanent voter in that category. He calls for a "cautious" approach on adjusting rates and unlike many of his colleagues, doesn't suggest that some further easing toward a more neutral stance is warranted.

- 1200ET – Hammack (’26, hawk) speaks at Economic Club of NY (text + Q&A). Speaking on Oct 31, she “would have preferred to have held rates steady at [last week’s] meeting and not to reduce rates […] We're right around my estimate of neutral, and I think we're barely restrictive, if at all. And so I do think we need to maintain some amount of restriction to help bring inflation back down to target."

- 1530ET – Gov. Waller (voter, dove) in panel on central banking and payments (no text). He made clear on Oct 31 that he supports a follow-up rate cut in December. “The fog might tell you to slow down. It doesn't tell you to pull over to the side of the road. You still have to go. You may want to be careful, but it doesn't mean to stop, and ... the right thing to do with policy is to continue cutting."

- 1630ET – Paulson (’26) speaks on consumer finance (text only). She said in her debut speech on Oct 13 that the Fed should move cautiously. With rates " modestly restrictive now", she sees easing through year-end in line with the September SEP median - in other words, two more cuts by year-end.

- 1730ET – Musalem (’25, hawk) in fireside chat on mon pol (no text). He noted on Oct 17 that "I could support a path with an additional reduction in the policy rate if there are further risks to the labor market that emerge," and if the risks for persistent inflation remain contained. "I do think we need to not be on a preset course" and added "right now, I think it's particularly important to go meeting by meeting.

US OUTLOOK/OPINION: Challenger To Boost Sensitivity To Jobless Claims Increases

A sharp rise in layoff announcements in the Challenger report should increase sensitivity to the weekly claims data, which for now see initial claims at healthy levels. We watch for any softening in tone from today's heavy Fedspeak schedule.

- The October Challenger report confirmed the low hiring state of the labor market but will also start to see greater questions on the low firing characterization in place for some time.

- Initial jobless claims data have clearly been evidence of low firing, including most recently with state-level data suggesting nationwide initial claims at just a seasonally adjusted 219k per MNI calculations in latest data to the week to Oct 25. That’s close to the average through 2019 when the unemployment rate had a 3-handle although clearly re-hiring conditions are softer now as evidenced by continuing claims and broader labor data.

- Today’s jump in forward-looking layoff announcements should see greater sensitivity to increases in the weekly claims data, starting with today’s state-level data this afternoon (we believe ~1700ET), something likely needed to drive a stronger market reaction. Indeed, Powell noted as such at last week's press conference (excerpt below).

- It will be interesting to hear whether today’s weak Challenger report is acknowledged in today’s deluge of Fedspeak (in chronological order from Williams, Barr, Hammack, Waller, Paulson and Musalem). Waller is clearly the most dovish of those speakers and has warned on risks to the labor market, but such comments would still be notable as it would go against the topic of central banking and payments. Most impactful though should be any softening in tone from hawks Musalem (’25 voter) and Hammack (‘26).

- Fed Chair Powell when asked about big layoff announcements coming from Amazon and others: "So those are -- those are both things that we're watching very -- very, very carefully. To start with the layoffs, you're right, you see a significant number of companies either announcing that they are not going to be doing much hiring, or actually doing layoffs, and much of the time they're talking about AI and what it can do. So, we're watching that very carefully. And yes, it could absolutely have implications for job creation. We don't really see it in the initial claims data yet. Now, it's not a surprise that we don't, it takes some time for it to get in there, but we're watching that really carefully. But again, don't see it yet in the -- in the initial claims data."

- Some further context on the then lack of a big spike in layoffs from Chicago Fed’s Goolsbee on Monday, a ’25 voter typically at the dovish end of the FOMC spectrum but who has also been recently cautioning on still stubborn inflation. He sees a higher threshold for cutting in Dec than last month: “If you look over the last 12 months, the unemployment rate has not been going up. We haven't seen a big uptick in layoffs, which, if this were the beginning of recession or deterioration of the labor market, that was rapid, you would expect to see higher layoffs or firing and we haven't seen that. There's still concerns on that side. I'm not decided going into the next meeting. I want to see how things are playing out. I do think the public announcements of layoffs you would expect, if that is an immediate business cycle-driven matter that you would start to see an uptick in the official unemployment insurance statistics or the layoff statistics, or you would get WARN Act type data of that form that would give you a little bit of a heads up of what was coming in the job market. I do think the hiring rate is low. That's among the weakest things in the economy at the moment.”

MNI BOE Preview - November 2025: It's All About Bailey

For the full MNI BOE Preview click here

- Thursday's MPC decision is far from certain - indeed we would categorise our own view of the outcome as 50/50 between a 25bp cut and a hold.

- We look at the drivers for each members' vote and the key data since the last meeting / August forecasts.

- In essence, we think a 5-4 vote is the most likely outcome but that it could deliver a cut or a hold. Governor Bailey's vote will be the deciding factor here, in our view.

- We have also summarised over 20 sellside previews.

SOFR: Net Short Setting Dominated In Futures On Wednesday

OI data points to net short setting dominating in SOFR futures on Wednesday, with only 3 rounds of modest net long cover and 1 instance of net long setting (SFRU5) interrupting the trend across the front 16 contracts.

| 05-Nov-25 | 04-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,392,778 | 1,379,596 | +13,182 | Whites | +78,053 |

SFRZ5 | 1,480,843 | 1,470,935 | +9,908 | Reds | +85,587 |

SFRH6 | 1,196,751 | 1,164,251 | +32,500 | Greens | +14,471 |

SFRM6 | 1,103,902 | 1,081,439 | +22,463 | Blues | +16,096 |

SFRU6 | 1,094,119 | 1,081,837 | +12,282 |

|

|

SFRZ6 | 1,207,732 | 1,172,616 | +35,116 |

|

|

SFRH7 | 836,392 | 815,754 | +20,638 |

|

|

SFRM7 | 789,461 | 771,910 | +17,551 |

|

|

SFRU7 | 765,961 | 752,704 | +13,257 |

|

|

SFRZ7 | 792,891 | 793,356 | -465 |

|

|

SFRH8 | 419,328 | 417,446 | +1,882 |

|

|

SFRM8 | 403,663 | 403,866 | -203 |

|

|

SFRU8 | 338,927 | 331,846 | +7,081 |

|

|

SFRZ8 | 332,567 | 323,745 | +8,822 |

|

|

SFRH9 | 204,593 | 203,327 | +1,266 |

|

|

SFRM9 | 186,002 | 187,075 | -1,073 |

|

|

US TSY FUTURES: Mix Of Net Short Setting & Long Cover On Wednesday

OI data points to a mix of net short setting (TU, TY, UXY & WN) and long cover (FV & US) as Tsy futures sold off on Wednesday. Net short setting was slightly more prominent in DV01 equivalent terms.

| 05-Nov-25 | 04-Nov-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,644,390 | 4,603,426 | +40,964 | +1,545,547 |

FV | 6,812,600 | 6,816,604 | -4,004 | -171,849 |

TY | 5,446,791 | 5,434,512 | +12,279 | +819,854 |

UXY | 2,478,056 | 2,470,425 | +7,631 | +683,645 |

US | 1,865,749 | 1,883,042 | -17,293 | -2,193,053 |

WN | 2,153,187 | 2,144,309 | +8,878 | +1,649,926 |

|

| Total | +48,455 | +2,334,069 |

EUROPE ISSUANCE UPDATE:

Spain auction results

- E1.815bln of the 3.00% Jan-33 Obli. Avg yield 2.848% (bid-to-cover 2.06x).

- E1.208bln of the 1.85% Jul-35 Obli. Avg yield 3.111% (bid-to-cover 2.63x).

- E1.48bln of the 3.50% Jan-41 Obli. Avg yield 3.616% (bid-to-cover 2.05x).

- E534mln of the 1.15% Nov-36 Obli-Ei. Avg yield 1.392% (bid-to-cover 2.38x).

France auction results

- E7.2bln of the 3.50% Nov-35 OAT. Avg yield 3.43% (bid-to-cover 2.15x).

- E2.257bln of the 3.60% May-42 OAT. Avg yield 3.92% (bid-to-cover 2.92x).

- E1.526bln of the 3.00% Jun-49 Green OAT. Avg yield 4.12% (bid-to-cover 3.20x).

FOREX: USD Rally Loses Momentum, Reversal Lower Assisted by Weak US Data

- The broader dollar rally that has been playing out following the FOMC is showing signs of fatigue. Stabilisation for the major equity indices and the USD index reaching its initial objective at the August highs (~100.25) have contributed to the reversal lower on Thursday, with an early release of weak US Challenger job cuts data stoking additional pressure on the greenback.

- The USD index has slipped back below the 100 mark, allowing most G10 currencies to grind away from recent cycle lows. This has prompted EURUSD to rise back above 1.15, while GBPUSD is steadily moving back towards 1.31 ahead of today’s BOE rate decision. Note that the cable downtrend is in oversold territory and a recovery would allow this condition to unwind. Initial resistance is at 1.3142, the Aug 1 low.

- In similar vein, USDJPY has once again found resistance above the 154.00 mark, with a cluster of four daily highs between 154.36-48 provide potential signs of a bearish short-term signal. First important support to watch lies at 152.39, the 20-day EMA.

- Higher-than-expected preliminary October CPI data in Sweden has provided a moderate bullish impulse for the Swedish Krona, with USDSEK declines slightly outpacing that of the dollar index. The print shouldn’t have a major impact on the near-term Riksbank rate path, especially after the steady signals at yesterday’s decision.

- Higher oil prices have had more of an impact on the rallying Norwegian Krone, with an on hold Norges Bank and unchanged accompanying guidance doing little to move the NOK needle.

- Elsewhere, AUDNZD is attempting to establish itself above the 1.15 handle, having breached the key 1.1491 high earlier in the week. The cross is currently operating at the highest levels since 2013.

GBP: Optionality in Focus on Any Dovish BoE Response

Headed into today's BoE decision, GBP is off recent lows and among G10's best intraday performers, but the modest bounce is clearly consolidative at these levels and will have helped alleviate the oversold position. That said, prices are still 75 pips off the weekly high.

- Optionality in the wake of the decision is worth noting: £2.2bln in option notional is set to roll-off at 1.29 at today's 10am cut - which could prove influential in any dovish reaction to the decision, particularly as the notional comprises of £2.07bln in puts and just £115mln calls.

- Despite the more constructive GBP session, EURGBP has been consolidating its position around 0.8800, with dips remaining well supported following recent bullish developments.

- The breach of significant resistance at 0.8769 has bolstered the momentum for the cross, and this week’s retest of the breakout and subsequent bounce maintain the optimistic short-term view as both the BOE decision and budget approach. Topside targets for the broader rally include 0.8835 (held Wednesday) and 0.8875, the April 2023 high.

- Beyond today's decision, the Budget is quite clearly a focus, but we see GBP remaining structurally volatile even beyond that point: https://www.mnimarkets.com/articles/vol-markets-see-more-interest-in-eurgbp-over-gbpusd-into-boe-1762341301404

OPTIONS: Expiries for Nov6 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E1.5bln), $1.1450(E560mln), $1.1500(E1.6bln), $1.1525(E604mln), $1.1550(E1.8bln), $1.1600(E1.6bln), $1.1715(E1.5bln)

- GBP/USD: $1.2900(Gbp2.0bln), $1.3100(Gbp1.0bln), $1.3350(Gbp770mln)

- USD/JPY: Y152.00($1.0bln), Y153.00-05($1.2bln), Y154.00-05($1.1bln), Y154.50-55($1.1bln), Y155.00($1.9bln), Y155.35($1.2bln)

- EUR/GBP: Gbp0.8800-10(E1.1bln)

- EUR/JPY: Y177.00-05(E561mln)

- AUD/USD: $0.6480-90(A$650mln)

EQUITIES: Recent Short-Term Weakness for E-Mini S&P Considered Corrective

- Recent weakness in Eurostoxx 50 futures appears to have been corrective. The contract has found support at the 50-day EMA, at 5571.29. Support below the EMA lies at 5560.50, the base of a bull channel drawn from the Aug 1 low. A breach of this level and the 50-day EMA, is required to highlight a stronger reversal. Sights are on resistance and the bull trigger at 5742.00, the Oct 29 high.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and short-term weakness appears corrective. Support at the 20-day EMA, at 6805.85, has been breached. A clear break of this average signals scope for a deeper retracement and exposes the 50-day EMA at 6706.92 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

COMMODITIES: Gold Extends Recovery Off Tuesday's Lows

- WTI futures are trading below recent highs, however, a short-term corrective bull cycle remains in play. Price has recently traded through resistance at the 50-day EMA, currently at $60.97. The breach of this EMA signals scope for a stronger recovery. Note too that a resistance at $62.34, the Oct 8 high, has also been pierced. A clear move through it would expose key resistance at $65.77, Sep 26 high. The bear trigger is unchanged at $55.96, Oct 20 low.

- A fresh cycle low recently in Gold highlights an extension of the bear cycle that started Oct 20. The move down since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3871.7 - a key pivot support. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

| Date | GMT/Local | Impact | Country | Event |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1230/1230 | BOE Press Conference | ||

| 06/11/2025 | 1400/1400 | Decision Maker Panel Data | ||

| 06/11/2025 | 1500/1000 | * | Ivey PMI | |

| 06/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 06/11/2025 | 1530/1030 | BOC Governor Macklem testifies at Senate. | ||

| 06/11/2025 | 1600/1100 | NY Fed's John Williams | ||

| 06/11/2025 | 1600/1100 | Fed Governor Michael Barr | ||

| 06/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 06/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 06/11/2025 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 06/11/2025 | 1830/1930 | ECB Lane At IMF Conference | ||

| 06/11/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 06/11/2025 | 2030/1530 | Fed Governor Christopher Waller | ||

| 06/11/2025 | 2130/1630 | Philly Fed's Anna Paulson | ||

| 06/11/2025 | 2230/1730 | St. Louis Fed's Alberto Musalem | ||

| 07/11/2025 | 2330/0830 | ** | Household spending | |

| 07/11/2025 | 0700/0800 | ** | Trade Balance | |

| 07/11/2025 | 0745/0845 | * | Foreign Trade | |

| 07/11/2025 | 0800/0300 | New York Fed's John Williams | ||

| 07/11/2025 | 1110/1110 | BOE Saporta At ECB Money Market Conference | ||

| 07/11/2025 | 1200/0700 | Fed Vice Chair Philip Jefferson | ||

| 07/11/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 07/11/2025 | - | *** | Trade | |

| 07/11/2025 | - | BOE MPG Agenda Published | ||

| 07/11/2025 | 1330/0830 | *** | Labour Force Survey | |

| 07/11/2025 | 1330/1430 | ECB Elderson At Bundesbank Event | ||

| 07/11/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 07/11/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 07/11/2025 | 1515/1515 | BOE Pill At National Agency Briefing | ||

| 07/11/2025 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 07/11/2025 | 2000/1500 | Fed Governor Stephen Miran |