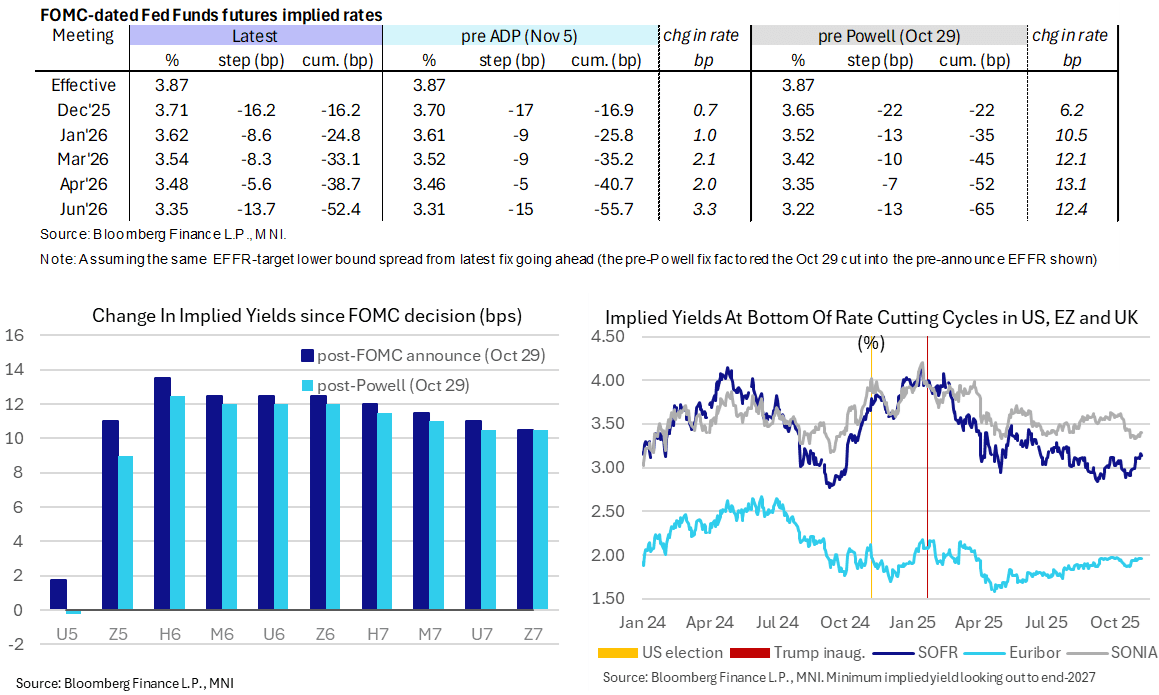

STIR: Challenger Layoff Spike Pares ADP and ISM Services Beats

- Fed Funds implied rates are 1.5-2.5bp lower overnight for meetings out to mid-2026 on the back of an early release of the October Challenger jobs report with its sharp rise in layoffs.

- It chips away at yesterday’s hawkish adjustment on slightly higher than expected ADP print before a clearer beat for ISM services.

- Cumulative cuts from 3.87% effective: 16bp Dec, 25bp Jan, 33bp Mar, 38.5bp Apr and 52.5bp Jun.

- SOFR futures are broadly 2-3 ticks higher looking out to end-27.

- That includes the terminal yield dipping 2.5bp to 3.135% after yesterday’s 6bp climb to 3.16% for its highest close since late July.

- Today sees a heavy Fedspeak schedule (see a guide to it just above) plus labor indicators from Revelio Labs, the Chicago Fed and NFIB before state-level jobless claims later in the afternoon.

- There could also be spillover from the BOE decision at 1200ET where we see a 50/50 likelihood of a 25bp cut or hold.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Roundup: Bank of England 5Y on Tap

- Date $MM Issuer (Priced *, Launch #)

- 10/07 $Benchmark Bank of England 5Y +8a

- 10/07 $Benchmark CPPIB 3Y SOFR+39

- 10/07 $Benchmark Angola +5Y 9.75%a, 10Y 10.5%a

- 10/07 $Benchmark Türkiye Garanti Bankası 10.5NC5.5

- 10/07 $Benchmark JDC Dev Bank Kazakhstan +5Y, KZT 3Y investor calls

- Expected Wednesday

- 10/08 $1B Kommunalbanken Norway WNG 3Y SOFR+37

- $9.9B Priced Monday

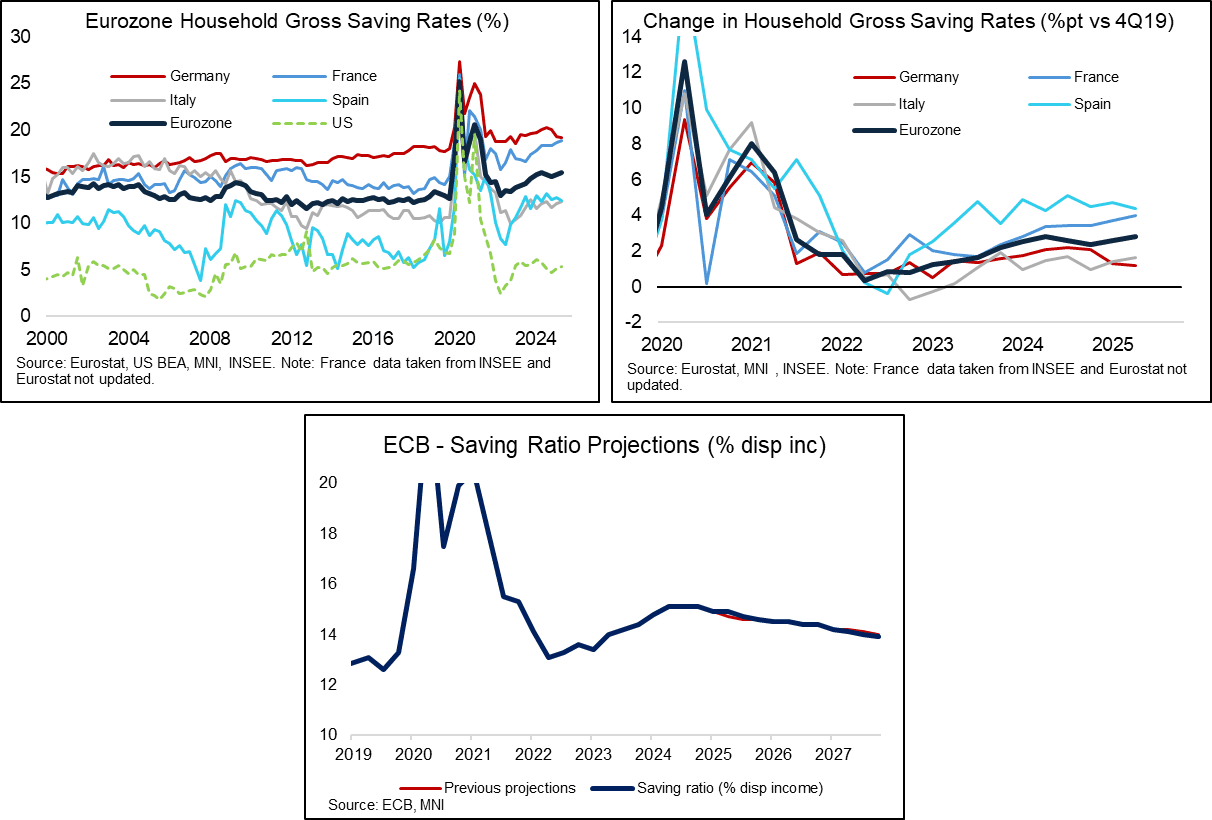

EUROZONE DATA: Q2 Savings Rate Exceeds ECB Projections; France Drifting Higher

The ECB expects higher real disposable incomes and a gradually declining savings ratio to strengthen private consumption in the coming years. In Q2, the household savings rate was estimated at 15.4%, above the ECB’s 14.9% projection and up from 15.2% in Q1. While a slow-moving train, a persistently elevated savings ratio is a dovish input for the ECB’s reaction function, both cyclically (i.e. via lower household consumption outturns) and structurally (i.e. via a lower neutral rate). In the near-term, the case for another rate cut to 1.75% will probably need to be motivated by higher frequency data (e.g. PMIs, inflation), but developments in the savings rate may push against early expectations for a rate hike over the next few years (against a backdrop of higher German fiscal spending).

- Across countries, the savings ratio ticked lower in Germany (19.2% vs 19.3% in Q1, 20.1% in Q4 and 20.2% in Q3) and Spain (12.4% vs 12.8% in Q1). Meanwhile, increases were seen in Italy (12.3% vs 12.1% in Q1) and France (18.9% vs 18.6% prior).

- France has displayed the clearest upward drift in the savings rate in recent quarters, an unsurprising development given ongoing political and fiscal uncertainty. With ex-PM Lecornu’s resignation keeping these risks elevated, and more fiscal consolidation required as part of any budget compromise, it’s hard to envisage a meaningful reversal in this trend anytime soon.

- For comparison, the US savings rate of ~5% remains significantly below that of the Eurozone. That’s in fitting with historical precedent, but Eurozone consumers have had plenty of reasons to remain cautious post-covid (e.g. proximity of the Russia/Ukraine conflict and the related spike in energy prices).

- We wrote more on Eurozone consumption, the savings ratio and related ECBspeak a few weeks ago.

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Oct08 $1.1700(E1.1bln), $1.1770-80(E1.2bln), $1.1800(E1.4bln), $1.1850-60(E1.0bln); Oct10 $1.1600(E1.3bln), $1.1650(E1.7bln), $1.1700(E1.6bln), $1.1740-50(E2.5bln), $1.1780-00(E2.8bln)

- USD/JPY: Oct08 Y146.50($1.2bln), Y147.00($1.5bln); Oct09 Y150.00-15($1.9bln)