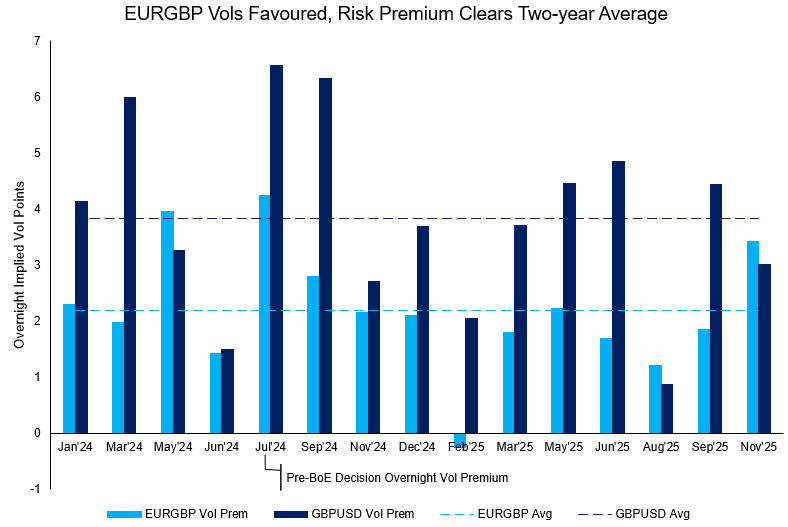

GBP: Vol Markets See More Interest in EURGBP Over GBPUSD into BoE

Markets are buying overnight GBP vol into tomorrow's BoE decision - which we see as a closer to 50/50 chance of cut vs. a hold - and therefore much more finely balanced than the ~7bps of cuts currently priced. Much of the buying interest has been via EURGBP rather than GBPUSD, with the cross a more popular expression for GBP weakness among the sell-side since the summer.

EURGBP markets added close to 3.5 points in overnight vol premium this morning, not far off double the pre-BoE decision average posted over the past two years. This doubles the break-even on an overnight straddle in the cross to +/- 35pips. In contrast, overnight GBPUSD vols have added 3.0 points - well shy of average and bucking the trend of 2025 so far.

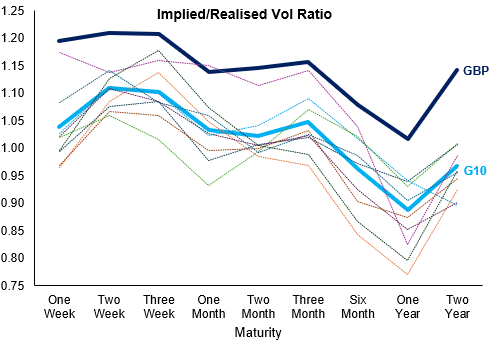

We noted yesterday that even beyond the Budget, markets see GBP remaining structurally volatile into 2026 - in excess of all other currencies in G10: For several months, implied vol contracts capturing the November 26th Budget have been trading at a premium relative to the rest of the curve. However, the ratio between implied/realised vol for maturities covering the end of the year and well into 2026 is well elevated relative to G10 peers, suggesting a persistent and sizeable GBP risk premium even beyond Reeves' next fiscal event:

Note: Dark blue line denotes GBP implied/realised vol ratio across all maturities out to two years. Light blue line is the G10 mean average, while pale dotted lines are respective G10 currencies.

Source: MNI/Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB FUNDING UPDATE: AFT may publish France's 2026 issuance plans at any time

- With the 13 October deadline to submit the Budget to parliament almost certain to be missed we look at when the AFT has published its year-ahead funding plans in recent years.

- France's AFT (Agence France Tresor) normally publishes its year-ahead "funding situation" which includes an outline for issuance volumes in September. For reference between 2016-2023 it was published between 22-28 September.

- Last year, despite the political uncertainty, the government did still present a budget to parliament on 9 October - meeting the 70 day timeline required for parliament to deliberate.

- The AFT then published its 2025 provisional plans on 10 October - the day after the budget was submitted to parliament.

- In the absence of anything else, the AFT may choose to use broadly unchanged numbers from 2025 for the deficit size. Together with an extra E10-11bln of MT/IL debt due to mature in 2026, we think that expectations will be for the 2026 gross issuance plan to be around E310-315bln. This follows E300bln in 2025, E285bln in 2024, E270bln in 2023 and E260bln in 2022.

- The AFT may chose to publish this initial estimate at any time - it may decide that the political turmoil won't lead to a definitive outcome any time soon so publish imminently, or may leave until later this year. There is no real precedent here.

- Note that the more detailed update has been published later in the last couple of years: on 19 December in 2024, 13 December in 2023, 7 December in 2022, 10 December in 2021 and 9 December in 2020.

OUTLOOK: Price Signal Summary - Gold Bulls Still In The Driver's Seat

- On the commodity front, a bull cycle in Gold remains in play and today’s fresh cycle high, reinforces current conditions. This maintains the bullish price sequence of higher highs and higher lows and note too that corrections, when they do occur, are shallow. Furthermore, momentum studies highlight a condition known as momentum drag - where momentum studies remain in overbought territory and move sideways. This condition reinforces the current trend direction. Sights are on $3987.3 next, a 2.236 projection of the May 15 - Jun 16 - 30 price swing. Support to watch lies at $3715.0, the 20-day EMA.

- In the oil space, WTI futures remain in a bear-mode condition. Last week’s sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens a bearish theme and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal.

US TSYS: Curve Steeper On Japanese & French Cues, Shutdown Continues

TY futures trade back towards London morning lows after bulls failed to close the opening gap lower during a relief rally, last -0-06+ at 112-15.

- Immediate support at the 50-day EMA (112-12+) protects retracement support (112-01). Conversely, bulls look to break the Sep 24 top (113-00).

- Spill over from Japan (where a new LDP Party leader & PM promoted twist steepening) and France (with another PM resignation seen) provides bear steepening pressure, yields 0.5-5.0bp higher.

- 2s10s at 57.2bp, 5s30s at 102.9bp, consolidating within multi-week ranges. 2s10s ~7bp off cycle closing highs, 5s30s ~20bp off cycle closing top, after some modest steepening last week.

- The government remains in shutdown. ~75% of Polymarket bettors believe the shutdown will last until October 15 at the earliest.

- Markets remain focused on the timing of delayed data releases, most notably the September Employment report.

- This week’s supply (including 3-, 10- & 30-Year Tsy auctions) will go ahead as scheduled.

- Fed pricing little changed to start the week, OIS near enough fully discounts a 25bp cut at this month’s meeting and prices ~47bp of easing through year-end.

- Just over 100bp of cuts priced between now and the end of the September ’26 FOMC, while SOFR-implied terminal rate pricing sits at 3.065% (vs. ~2.80% at one point in September).

- Kansas City Fed President Schmid well speak on the economic outlook and monetary policy later today (17:00 NY/22:00 London).