FOREX: USD Rally Loses Momentum, Reversal Lower Assisted by Weak US Data

Nov-06 10:31

- The broader dollar rally that has been playing out following the FOMC is showing signs of fatigue. Stabilisation for the major equity indices and the USD index reaching its initial objective at the August highs (~100.25) have contributed to the reversal lower on Thursday, with an early release of weak US Challenger job cuts data stoking additional pressure on the greenback.

- The USD index has slipped back below the 100 mark, allowing most G10 currencies to grind away from recent cycle lows. This has prompted EURUSD to rise back above 1.15, while GBPUSD is steadily moving back towards 1.31 ahead of today’s BOE rate decision. Note that the cable downtrend is in oversold territory and a recovery would allow this condition to unwind. Initial resistance is at 1.3142, the Aug 1 low.

- In similar vein, USDJPY has once again found resistance above the 154.00 mark, with a cluster of four daily highs between 154.36-48 provide potential signs of a bearish short-term signal. First important support to watch lies at 152.39, the 20-day EMA.

- Higher-than-expected preliminary October CPI data in Sweden has provided a moderate bullish impulse for the Swedish Krona, with USDSEK declines slightly outpacing that of the dollar index. The print shouldn’t have a major impact on the near-term Riksbank rate path, especially after the steady signals at yesterday’s decision.

- Higher oil prices have had more of an impact on the rallying Norwegian Krone, with an on hold Norges Bank and unchanged accompanying guidance doing little to move the NOK needle.

- Elsewhere, AUDNZD is attempting to establish itself above the 1.15 handle, having breached the key 1.1491 high earlier in the week. The cross is currently operating at the highest levels since 2013.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NORGES BANK: Bache Reiterates September Guidance, Rest of Speech On Climate Chg

Oct-07 10:29

Policy signal from Norges Bank Governor Wolden Bache is consistent with the September monetary policy decision: "The job of tackling high inflation has not been fully completed. From our current standpoint, we do not envisage a large decline in the policy rate ahead."

No material impact on NOK markets as a result.

The rest of the speech focuses on climate change.

- "the transition and climate change can affect consumer prices. A larger share of renewable energy in electricity production may lead to more variable electricity prices, while more frequent extreme weather events may give rise to higher volatility in other prices, particularly for food. "

- "While the need for both higher investment to cut emissions and a larger supply of renewable energy will increase demand, lower petroleum investment will have a gradual dampening effect."

- "Both the phasing out of fossil-based productive capital and climate-related damage can dampen potential output. Moreover, potential output is determined by productivity growth, which depends on whether climate-related investment generates more economic productivity than other investment."

- "Climate change may lead to more frequent individual climate events that push up prices. If the central bank chooses to look through each individual event, average inflation over time could exceed the target. If firms and households begin to expect this and assume higher inflation when setting prices and wages, inflation may become entrenched. This may make it more costly to bring inflation down to target".

- "How climate change and the transition will affect the normal interest rate is uncertain."

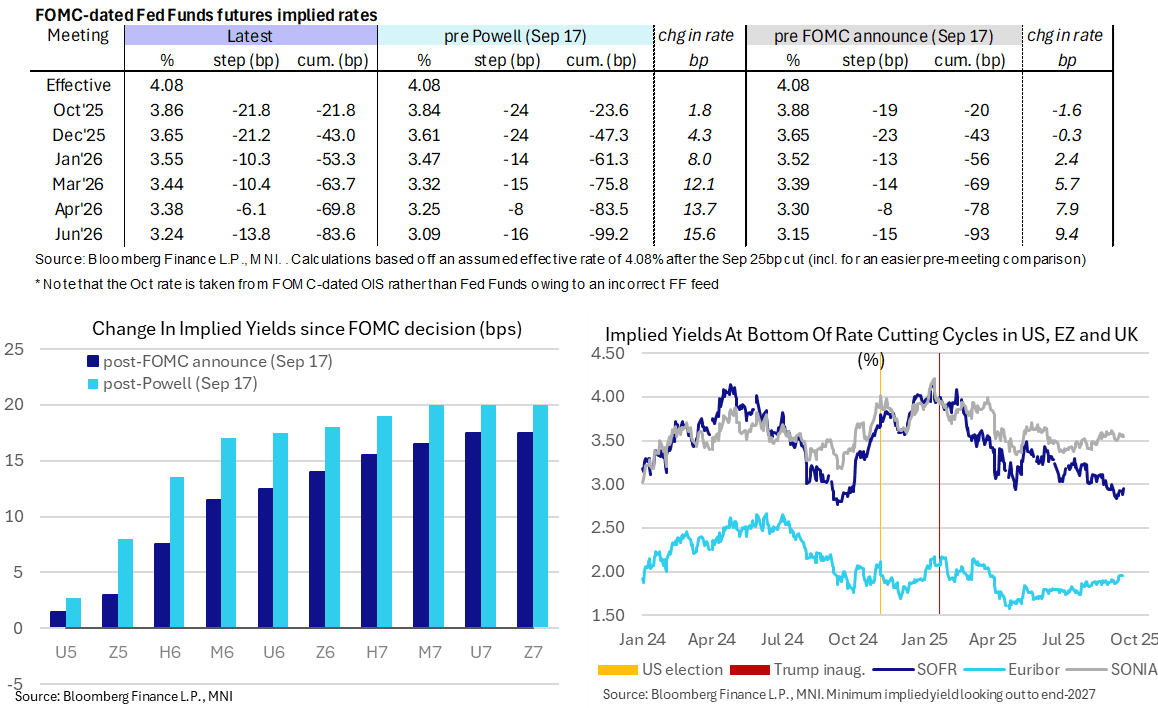

STIR: Fed Rates Little Changed

Oct-07 10:28

- Fed Funds implied rates are broadly 1bp higher on the day, with the mild increase coming in London hours rather than in response to typically hawkish comments from Schmid late yesterday (policy in right place, only sightly restrictive).

- Cumulative cuts from 4.08% effective: 22bp Oct, 43bp Dec, 53.5bp Jan, 64bp Mar, 70bp Apr and 83.5bp Jun.

- SOFR futures mild losses are led by the M6 (-0.01) and otherwise little changed at -0.005.

- The SOFR implied terminal yield at 3.085% (~100bp of cuts from current levels) is seen in the Z6 and H7 contracts, having ticked into the Z6 yesterday for the first time since mid-July.

- It remains off recent highs of 3.11/3.12% seen in late September (looking at closes).

LOOK AHEAD: Tuesday Data Calendar: Fed Speakers, 3Y Note Auction

Oct-07 10:26

Tuesday's Trade Balance & Import/Export data suspended due to the ongoing US Gov shutdown.

- US Data/Speaker Calendar (prior, estimate)

- ** Trade Balance (-$78.3B, -$61.0B)

- ** Imports/Exports MoM (5.9%, --)/(0.3%, --)

- 10/07 0855 Redbook Retail Sales

- 10/07 1000 Atlanta Fed Bostic moderated discussion Fisk University in Nashville

- 10/07 1005 Fed VC Bowman Delivers Welcoming Remarks bank research conf

- 10/07 1030 Fed Gov Miran Fireside Chat

- 10/07 1100 NY Fed Survey of Consumer Expectations (3.2%, --)

- 10/07 1130 MN Fed Kashkari Speaks at Star Tribune Summit

- 10/07 1130 US Tsy $90B 6W bill auction

- 10/07 1300 US Tsy $58B 3Y Note auction (91282CPC9)

- 10/07 1500 Consumer Credit ($16.01B, $14.00B)

- 10/07 1605 Fed Gov Miran Deutsche Bank Event

- Source: Bloomberg Finance L.P. / MNI

Trending Top

Jan-30 21:43

Jan-30 21:11