MNI EUROPEAN OPEN: China to Boost Consumption

EXECUTIVE SUMMARY

- China Targets Investment To Boost Consumption - MNI Policy

- Putin Hosts US Negotiators at Kremlin - BBC

- BOE Warns of AI Tech Bubble - TIMES

- China Property Developer's Woes to have little impact on banking sector - YICAI

- Australia Q3 GDP Softer Than Expected, But Domestic Demand Very Strong - MNI

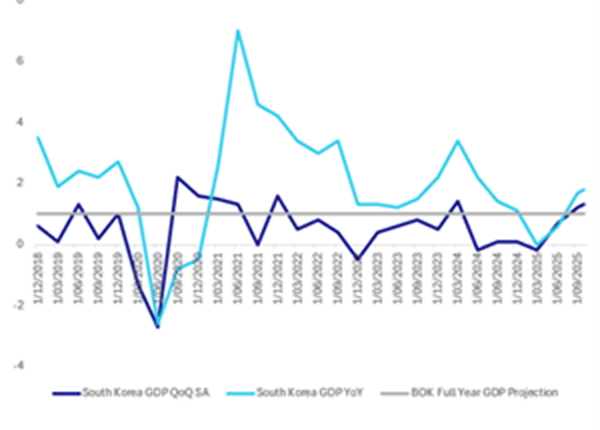

Fig 1: South Korea GDP QoQ, YoY vs Full Year Forecast

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

FINANCE (TIMES): “The threat posed by a potential AI bubble is being deepened by the use of debt to help underpin $5 trillion of investment in the technology over the next five years, the Bank of England has warned.”

CHINA (BBC): “No 10 highlighted the security advantage of consolidating the seven Chinese sites currently dotted around the capital, as the date for a decision on whether to grant planning permission was pushed back for a third time - into the new year.”

EU

EU (POLITICO): “The European Commission is offering a legal fix to allay Belgium’s fears of a nightmare scenario that could unfold if €140 billion in Russian assets frozen in Brussels are used as a loan to Ukraine.”

RUSSIA (BBC): “Russia's Vladimir Putin hosted US negotiators at the Kremlin on Tuesday for five hours of talks aimed at ending the war in Ukraine. Putin's aide Yuri Ushakov said the discussions - held behind closed doors with US envoy Steve Witkoff and President Donald Trump's son-in-law Jared Kushner - were "constructive" but "a lot of work lies ahead".”

UKRAINE (POLITICO): “On a visit to Ireland, the Ukrainian president says U.S. diplomacy in Moscow needs to include binding security commitments that make a renewed Russian assault impossible.”

ENERGY (BBG): “The European Union has reached a deal to phase out Russian natural gas by 2027 to end dependency on Russian gas and strengthen the EU's energy security.”

BUSINESS (POLITICO): “Lobbyists for some of the world's largest drug companies are parading a new pricing deal in the U.K. as a model the rest of Europe should emulate if it wants to keep drugmakers from bailing for America.”

EU (POLITICO): “EU legislators struck a deal on the first bloc-wide law to combat corruption after several concessions were made to give countries more leeway in its enforcement.”

US

FED (BBG/WSJ): “The Trump administration canceled a slate of interviews with finalists to be the next chair of the Federal Reserve, with no reason given for the decision.”

BRAZIL (BBG): “President Donald Trump spoke with Brazilian President Luiz Inacio Lula da Silva about sanctions the US imposed on Brazilian officials. Trump said the call was "very productive" and that they discussed trade, sanctions, and "how our Countries could work together to stop Organized Crime".”

POLITICS (BBG): “Republicans averted an upset in a Tennessee-based US House race Tuesday, a relief to President Donald Trump and his congressional allies. Matt Van Epps, the Trump-backed Republican candidate, was projected to win by the AP, NBC News and Decision Desk HQ, an election analysis website. Yet even in victory, voters in a district Trump won overwhelmingly just over a year ago swung away from Republicans.”

VENEZUELA (BBG): “Secretary of State Marco Rubio cast doubt on the possibility that the US could negotiate a deal with Nicolas Maduro to get him to stop drug traffickers, saying the Venezuelan leader has repeatedly broken commitments over the years.”

FINANCE (BBC): “Tech billionaire Michael Dell and his wife, Susan, have announced plans to donate $250 to 25 million children across the US. The $6.25bn (£4.72bn) gift will bolster Trump-branded investment accounts.”

OTHER

AUSTRALIA (MNI): “Australia’s Q3 GDP rose 0.4% q/q, 30 basis points below expectations, and 2.1% y/y, 10bp below forecasts, National Accounts data released on Wednesday showed.”

AUSTRALIA (MNI): “China is likely to meet its 5% GDP growth target this year and has successfully found alternative markets for its goods, mitigating the impact of U.S. trade restrictions, supporting iron ore prices and insulating the Australian economy, Michele Bullock, Governor of the Reserve Bank of Australia, said on Wednesday.”

SOUTH KOREA (BBG): “South Korean President Lee Jae Myung said regular joint military drills with the US could be reviewed in order to facilitate dialogue with North Korea.”

SOUTH KOREA ECONOMY (MNI): 3Q GDP Surprises to the Upside

MEXICO (MNI): “Mexican credit markets react with a delay to interest rate moves, and the effects of past monetary tightening will continue to filter through and allow policymakers to keep adjusting policy gradually, deputy governor of the Central Bank of Mexico Omar Mejia, who has just co-authored a study on the subject, told MNI.”

CHINA

MNI China Press Digest Wednesday 3: PBOC, Vanke, SOE Assets

MNI POLICY (MNI): Chinese officials will aim to raise the household consumption-to-GDP ratio by an average of one percentage point per year over the next five years from the current 39.9% towards the 50-70% range typical of developed economies, using a combination of consumption-related infrastructure spending, services subsidies and wage-growth support, MNI understands.

ECONOMY (BBG): “China’s services activity expanded at the weakest pace in five months, a private survey showed, adding more evidence of sluggish consumer demand that’s putting further pressure on a slowing economy.”

PBOC (SECURITIES DAILY): “The People’s Bank of China (PBOC) injected a net CNY50 billion through open-market Treasury bond purchases in November, marking the second consecutive month of such operations, Securities Daily reported.”

PROPERTY (YICAI): “Property developer Vanke’s recent bond turmoil will have only a limited impact on the banking system, according to most research institutions, with market focus shifting from systemic risk to the differentiated effects on individual banks, Yicai reported.”

FISCAL (YICAI): “Many localities have intensified efforts to activate state-owned assets, resources and funds, amid a backdrop of sluggish fiscal revenue growth, worsening fiscal imbalances and rising debt pressures, Yicai reported.”

MNI: PBOC Net Drains CNY134 Bln via OMO Wednesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY79.3 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY134 billion after offsetting maturities of CNY213.3 billion today, according to Wind Information

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4143% at 09:33 am local time from the close of 1.4410% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Tuesday, compared with the close of 51 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.0754 Weds; +2.52% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0754 on Wednesday, compared with 7.0794 set on Tuesday. The fixing was estimated at 7.0665 by Bloomberg survey today.

MARKET DATA

AUSTRALIA Q3 GDP +0.4% Q/Q; EST. 0.7%; Q2 +0.7%

AUSTRALIA Q3 GDP +2.1% Y/Y; EST. 2.2%; Q2 +2.0%

NZ NOV. ANZ COMMODITY EXPORT PRICES -1.6% M/M; OCT. -0.3%

JAPAN S&P GLOBAL NOV. SERVICES PMI 53.2; PRE 53.1; OCT 53.1

JAPAN S&P GLOBAL NOV. COMPOSITE PMI 52.0; PRE. 52.0; OCT. 51.5

SOUTH KOREA NOV. FOREIGN EXCHANGE RESERVES $430.66B; OCT. $428.82B

S. KOREA Q3 GDP +1.8% Y/Y, REVISED FROM +1.7%; Q2 +0.6%

S. KOREA Q3 GDP +1.3% Q/Q, REVISED FROM +1.2% INCREASE; Q2 +0.7%

MARKETS

US TSYS: Yields Lower Across Curve; TYH6 Nears Key Tech Level

Bond futures are up modestly across all maturities today in a relatively low volume trading day in Asia. The 10-Yr is up +02 at 112-31 with topside resistance at 113 being the 20-day EMA. Downside resistance in the 50-day EMA is at 112-27, where it failed to trade below in recent falls.

Cash rallied across the curve with yields down across all maturities, with the front end outperforming.

- The 2-Yr is down -1.2bps to 3.50%

- The 5-Yr is down -1.2bps to 3.645%

- The 10-Yr is down -1bps to 4.079%

- The 30-Yr is down -0.9bps to 4.739%

Projected rate cut pricing rises vs. late Monday US time (*): Dec'25 at -24.6bp (-24.7bp), Jan'26 at -31.8bp (-30.6bp), Mar'26 at -39.7bp (-37.8bp), Apr'26 at -46.8bp (-44.1bp).

Wednesday Key Data Calendar: ADP Employment Change, Import/Export Price Index, Industrial Production MoM, S&P Global US Services PMI, ISM Services Index and New orders.

For new issuance, bills remain in focus with a US$75bn 6-week auction

JGBS: 30YY Leads Yields Higher Ahead Of Tomorrow's Supply, Rinban Op Fuels Sell

JGB futures are weaker, -24 compared to settlement levels.

- (Bloomberg) JGB contracts are extending losses in the afternoon session, with investors surprised at the depth of the selling of bonds back to the BOJ at its regular buying operations. Given this week’s 10-year auction was solid, the amount of bonds being offered is causing some level of shock, especially looking at the short duration,s which are most affected by BOJ rate hikes.

- (Dow Jones) "Japanese government bond yields are higher as expectations for a near-term rate increase by the Bank of Japan continue. The BOJ's policy board is scheduled to meet on Dec. 18-19 for a final rate decision for the year. To gauge the economy's strength, investors will be focusing on economic indicators, including household spending data due Friday."

- Cash US tsys are ~1bp richer in today’s Asia-Pac session.

- Cash JGBs are flat to 2bps cheaper across benchmarks, with the 30-year underperforming ahead of tomorrow’s supply. The benchmark 10-year yield is at 1.877% versus the cycle high of 1.886%, set before yesterday's strong 10-year auction.

- Swap rates are flat to 1bp higher.

- Tomorrow, the local calendar will see weekly International Investment Flow data alongside 30-year supply.

Source: Bloomberg Finance LP

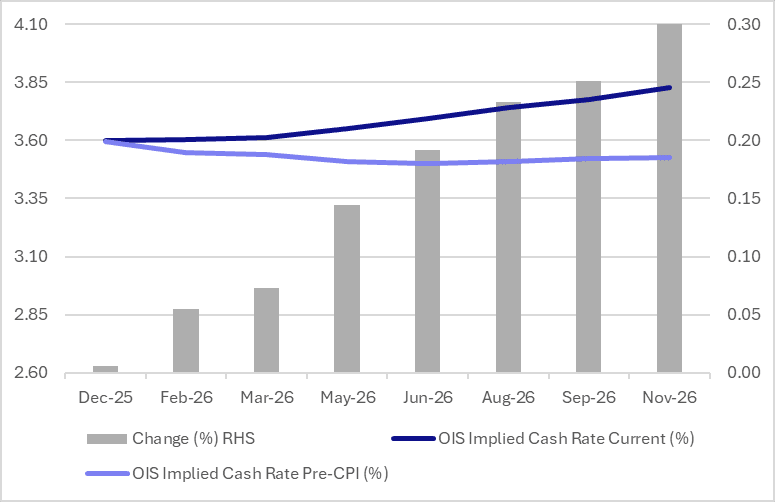

AUSSIE BONDS: Q3 Domestic Demand Drives Yields Higher, Hike Priced By Dec-26

ACGBs (YM -6.5 & XM -3.0) have bear-flattened after today’s Q3 GDP data. The market initially rallied on the data headlines but quickly reversed after details revealed underlying strength.

- Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details were a lot stronger than the headline, with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022.

- Cash US tsys are ~1bp richer in today’s Asia-Pac session.

- Cash ACGBs are 3-6bps cheaper with the AU-US 10-year yield differential at +56bps, the widest since mid-2022.

- The latest round of ACGB Dec-35 supply saw the weighted average yield print 0.30bp through prevailing mids. However, today’s cover ratio slumped to 2.3550x from 3.4875x.

- The bills strip has sharply steepened, with pricing -1 to -10.

- RBA-dated OIS pricing is 1-7bps firmer for meetings beyond May today. Pricing shows zero probability of a 25bp rate cut in December. More notably, the market has shifted to assign a 96% probability of a 25bp hike by December 2026.

- Tomorrow, the local calendar will see Trade Balance and Household Spending data.

- The AOFM plans to sell A$1000mn of the 2.75% 21 November 2028 bond on Friday.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

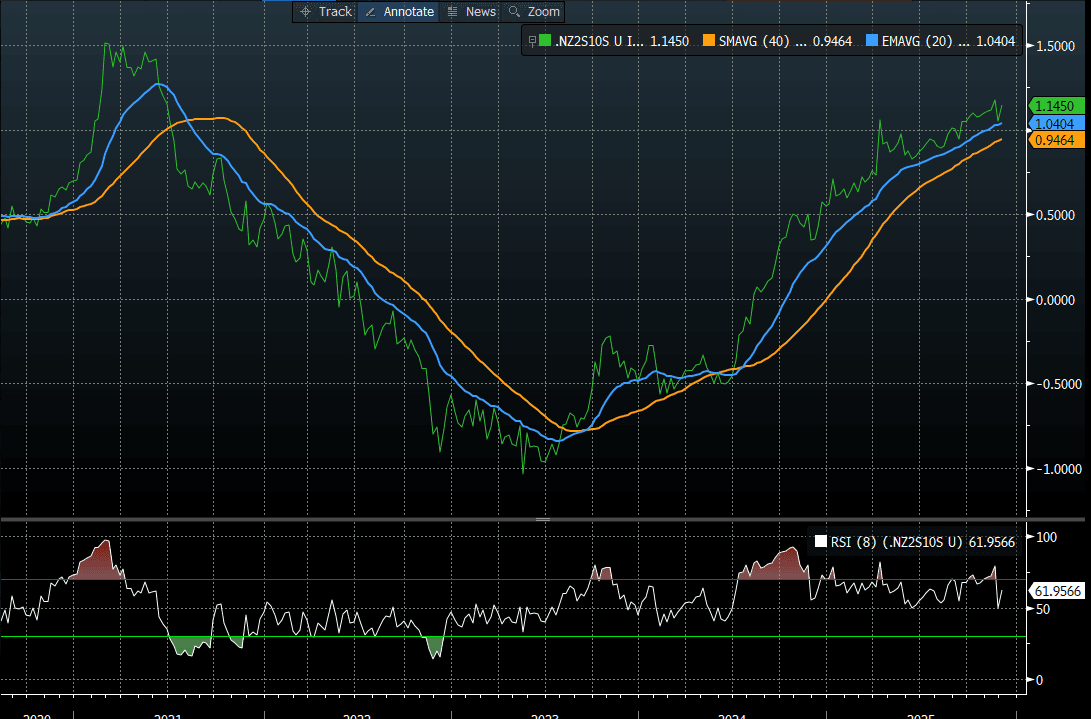

BONDS: NZGBS: Partial Unwind Of Post-RBNZ Sell-Off

NZGBs closed showing a bull-flattener, with benchmark yields 4-7bps lower. Nevertheless, yields remain 12-25bps higher than last week’s pre-RBNZ levels.

- On a relative basis versus its $-bloc counterparts, NZGBs also had a good day, with the NZ-US and NZ-AU 10-year yield differentials 6bps and 10bps lower, respectively.

- NZ commodity export prices fell 1.6% m/m in November versus -0.3% in October.

- Swap rates closed 2-7bps lower, with the 2s10s curve flatter. Nonetheless, the curve remains within striking distance of the 2021 peak (see chart).

- RBNZ-dated OIS pricing closed slightly softer across meetings. 2bps of easing is priced for February, while November 2026 assigns 31bps of tightening.

- Tomorrow, the local calendar will see Cotality Home Values and Volume of All Buildings data alongside NZ Government 4-Month Financial Statements.

- The NZ Treasury also plans to sell NZ$150mn of the 4.50% May-30 bond, NZ$225mn of the 4.50% May-35 bond and NZ$75mn of the 2.75% May-51 bond.

Bloomberg Finance LP

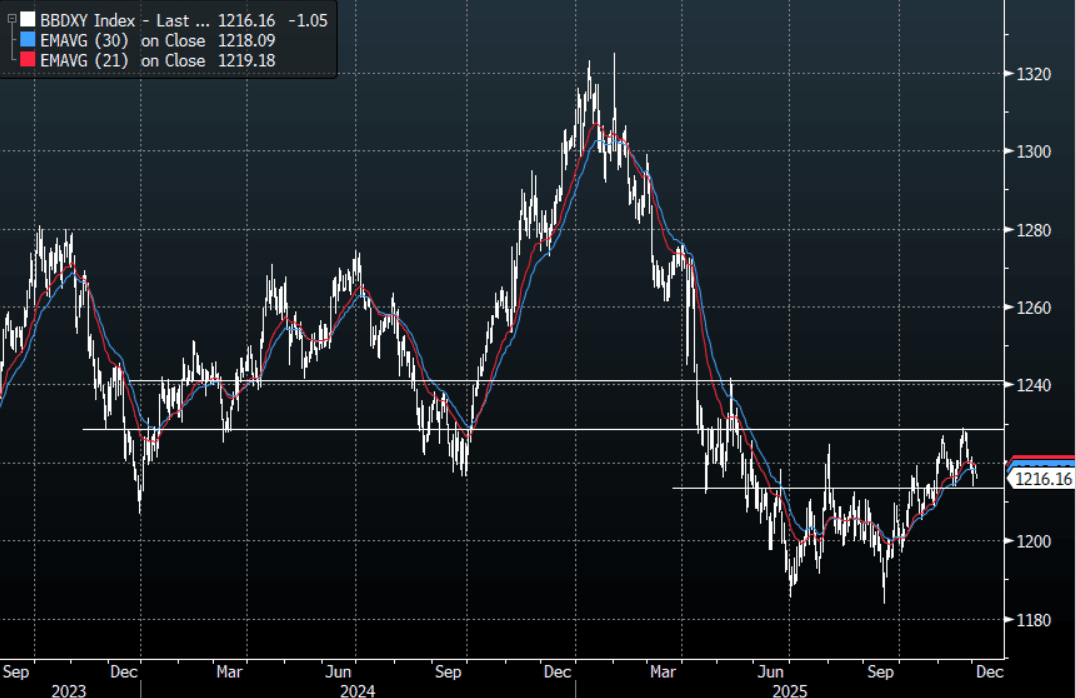

FOREX: USD - BBDXY Capped Toward 1220, Trades Heavy In Asia

The BBDXY has had a range today of 1216.02 - 1217.21 in the Asia-Pac session; it is currently trading around 1216, -0.10%. The USD has traded heavily all through the Asian session. The market seems confident Kevin Hassett will be announced as the new Fed Chair, this obviously adds headwinds to the USD from a rates perspective. The “sword of Damocles” hanging over the USD is also the Supreme Court's decision on the legality of Trump’s tariffs, this too could be announced toward the end of the year as the case has been expedited on national security reasons. On the day look for resistance again back towards the 1218-1221 area where sellers should remerge initially, a move back below 1214 which has been decent support recently could signal a deeper pullback towards 1205-1208 initially.

- EUR/USD - Asian range 1.1621 - 1.1638, Asia is currently trading 1.1640. The pair has consolidated above the 1.1600 area overnight. On the day as the market looks for more US cuts the USD should remain heavy. I suspect dips back toward 1.1600-20 could be supported initially looking to test the 1.1655-75 area later, a break of which could signal the beginning of some upward momentum again.

- GBP/USD - Asian range 1.3205 - 1.3232, Asia is currently dealing around 1.3230. The pair found decent demand sub 1.3200. I remain skewed toward shorts but I feel this move does signal the need to be patient. On the day GBP needs to hold above the 1.3180-1.3200 area which should continue to be supported, while above here look for the market to test the 1.3270-90 area initially, a break of which opens up a move toward 1.3350-70 where I suspect sellers could return.

- Cross asset : SPX +0.20%, Gold $4225, US 10-Year 4.076%, BBDXY 1216, Crude Oil $58.63

- Data/Events : France HCOB France Services PMI, Spain HCOB Spain Services PMI, EZ HCOB Eurozone Services PMI/ PPI, Italy HCOB Italy Services PMI, Germany HCOB Germany Services PMI

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

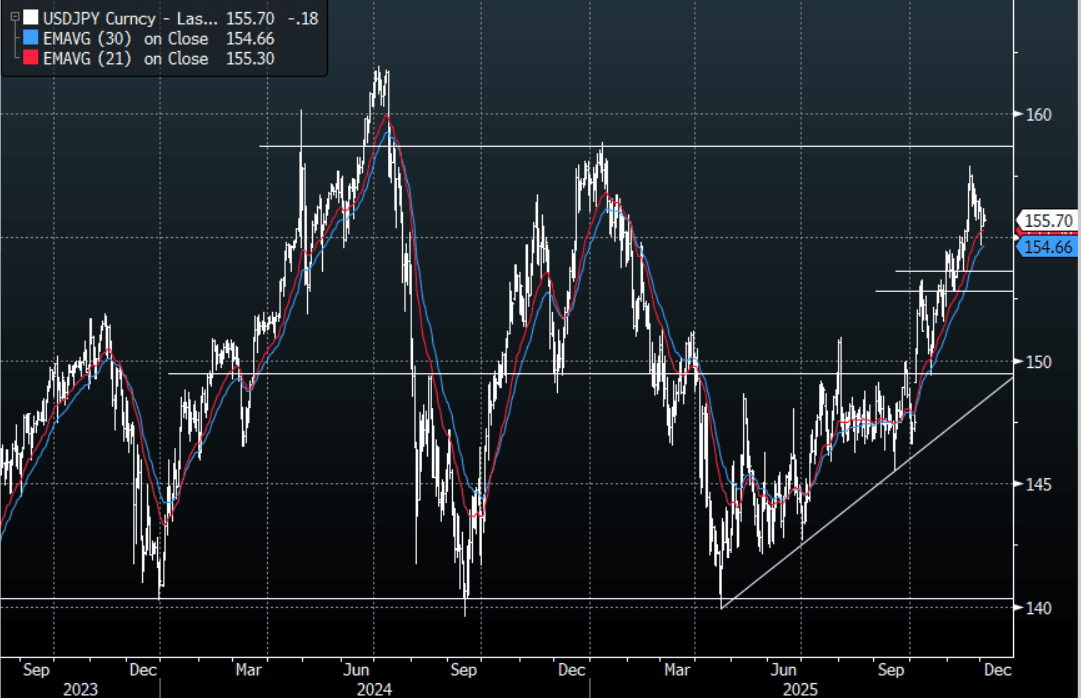

JPY: USD/JPY - Drifts Lower As The USD Trades Heavy

The USD/JPY range today has been 155.61 - 155.91 in the Asia-Pac session, it is currently trading around 155.70, -0.10%. The pair has drifted lower as the USD trades heavy across the board. The market is pricing in the fact that the Yen move looks like it could force the BOJ into action in December and a possible Hassett appointment brings more U.S. cuts into focus. This should keep the move that looked about to go parabolic a little more contained in the short-term but I suspect the market will still look for opportunities to express a long USD. Technically USD/JPY continues to look like it wants to test higher with the first big support back toward the 153-155 area which should see buyers reemerge. On the day I suspect we will continue to consolidate within a wider 155.00-156.50 range, with risk turning around its poor start to the week a short Yen might best be expressed in the crosses.

- (Dow Jones) - "Japanese government bond yields are higher as expectations for a near-term rate increase by the Bank of Japan continue. The BOJ's policy board is scheduled to meet on Dec. 18-19 for a final rate decision for the year. To gauge the economy's strength, investors will be focusing on economic indicators, including household spending data due Friday."

- MNI POLICY: Ueda Sharpens Dec Rate Hike, Risks Credibility. A hold at the Bank of Japan’s Dec. 18–19 meeting would be inconsistent with the bank’s recent market communications and would undermine its credibility, following Governor Kazuo Ueda’s comments on Monday that strongly indicated policymakers are set to raise the 0.5% rate this month, MNI understands.

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($1.27b). Upcoming Close Strikes : 153.00($1.2b Dec 4), 155.00($1.4b Dec 5), 156.00($1.14b Dec 8 ) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 88 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

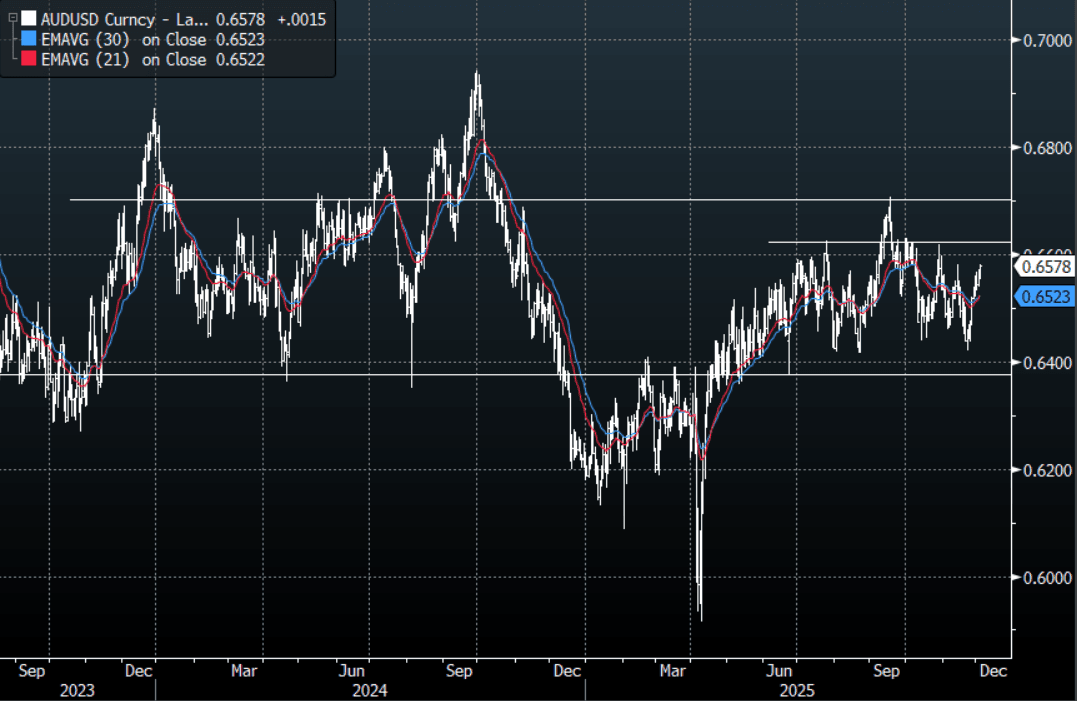

AUD/USD - GDP Data Not So Bad Sees AUD Bounce Back, Testing 0.6580

The AUD/USD has had a range today of 0.6553 - 0.6578 in the Asia- Pac session, it is currently trading around 0.6575, +0.20%. The AUD/USD had a brief look lower on the immediate GDP print back quickly recovered once the details showed underlying strength. The AUD has not backed off in all the noise and is pressing the pivot around 0.6580 within its wider 0.6350-0.6700 range. On the day, it feels like there is an air of inevitability around the AUD pushing above 0.6580 so I suspect dips back toward the 0.6535-0.6555 area could now be supported. A clear break above 0.6580 and the AUD could build some momentum looking to once again test the top end of its recent range, first target 0.6630 and then 0.6700.

- MNI AU - Strong Domestic Demand Growth To Keep RBA Cautious. Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details are a lot stronger than the headline with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

- MNI AU - RBA-dated OIS pricing is 1-7bps firmer for meetings beyond May today. Currently, pricing shows zero probability of a 25bp rate cut in December. More notable, the market has shifted to assign a 96% probability of a 25bp hike by December 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6475(AUD814m Dec 8), 0.6490(AUD710m Dec 4), 0.6500(AUD1.11b Dec 5) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 37 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

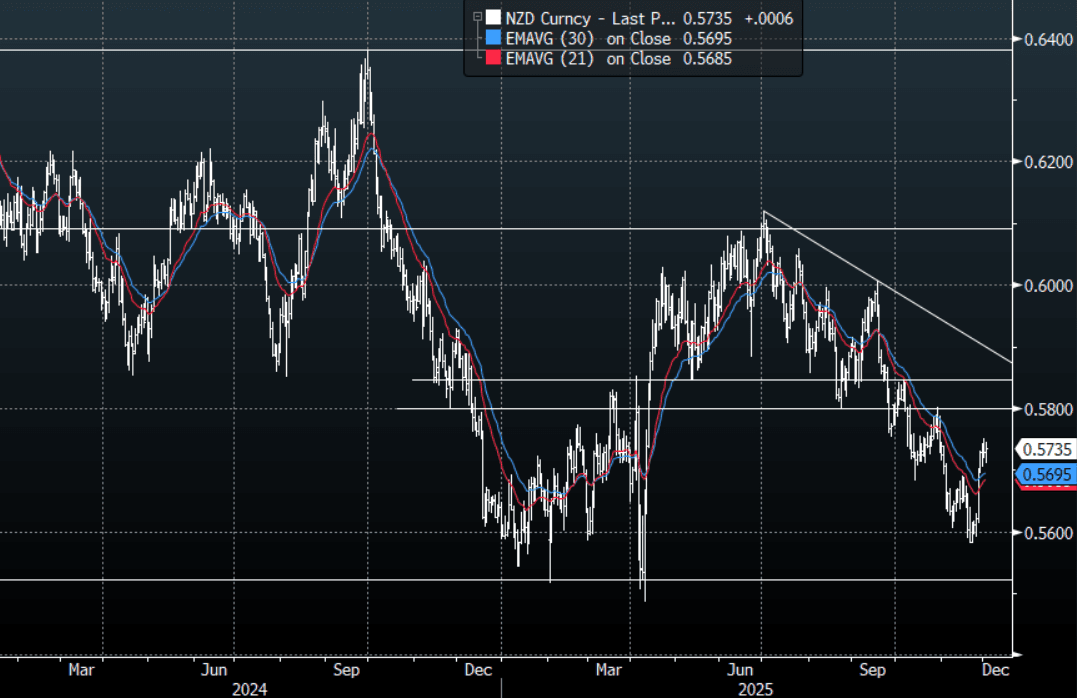

NZD/USD - Drifts Sideways Above 0.5700, Eyes 0.5760-70

The NZD/USD had a range overnight of 0.5725 - 0.5752, Asia is trading around 0.5735. The NZD continues to trade sideways consolidating just below the 0.5750 area, risk has managed to turn the poor start to the week around and Crypto has eventually seen buyers on the dip. Positioning could still be an issue in the short term. On the day it looks as though the NZD could remain well supported on dips, a sustained push back above 0.5760-70 should then potentially see the focus turn back toward the more important 0.5800-50 resistance. On the day support looks to be back toward the 0.5690-0.5710 area.

- Bloomberg: “Whole Milk Powder Average Price Falls to $3,364 a Ton from $3,452 at the previous auction, according to the GlobalDairyTrade website. GDT's weighted average price for all milk products was $3,507 a ton.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5575(NZD547m), 0.5730(NZD621m). Upcoming Close Strikes : 0.5670(NZD382m Dec 8), 0.5700(NZD332m Dec 5), 0.5730(NZD692m Dec 8 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 42 Points

- Data/Event: ANZ Commodity Price, Cotality Home Value

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Regional Bourses Mixed; China Lags Tech Rally Again

Whilst US indexes finished modestly up overnight, it wasn't enough to spur regional investor appetite with a mixed day across the region for major bourses. With most key AI tech stocks providing gains, tech heavy bourses were up again today with the NIKKEI and KOSPI leading. BITCOIN has recovered all of Monday's losses following news that China is cracking down on crypto speculators and that helped feed into better risk sentiment in general. China's major regional bourses are down and continue to lag the tech led boom elsewhere, with some market commentators suggesting that Chinese AI / tech names remain undervalued relatively to SK and JN names.

- The NIKKEI is up +1.5% to break above the 50,000 level to be 4.5% below the October high whilst the KOSPI was up again, by 1.2% today to break above the 4,000 level and close in on the early November high of 4,221

- China's major bourses are all lagging, with the Hang Seng the worst performer, down -0.95%. With Shanghai Comp and the CSI 300 doing little but trending weaker, it was down to Shenzhen to follow lower, dropping -0.35%

- The TAIEX is up +0.60% with TSMC up over 1% as US President Trump signs bill to deepen US-Taiwan ties .

- Having closed at a new high of 26,215 on November 27, the NIFTY 50 has fallen moderately each day since and is down -0.4% today at the open ahead of this week's RBI decision and the currency under pressure again.

- Jakarta and KL are moving in opposite directions with the JCI up +0.25% whilst the FTSE Malay KLCI is down -0.44% taking out some of its gains to start December.

OIL: Crude Little Changed As Waits For US EIA Data Out Later

Oil prices are little changed today ahead of the US EIA fuel inventory and demand data later. The industry figures showed crude and product builds. The market is also monitoring US-Ukraine-Russia developments closely in case a peace deal is close which could see an easing of restrictions on Russia at a time of excess global oil supply. It doesn’t seem worried at this stage regarding Russia’s threat to strike vessels of countries supporting Ukraine.

- WTI is off its intraday low of $58.37/bbl to be steady at $58.66/bbl, while Brent is slightly higher at $62.49 after falling to $62.18.

- US Secretary of State Rubio said that talks are currently at the point of trying to work out what Ukraine can accept and to bridge the divide between it and Russia. Russia said that President Putin agreed with many points in the revised plan and the territory issue was discussed. The US is now going back to the Ukrainians.

- Venezuela, the world’s 17th largest oil exporter in 2023 (IEA), remains an issue with the US saying it will continue targeting drug running vessels and Rubio saying that negotiating a deal would be difficult as Venezuela’s Maduro has “broken every deal he’s ever made”.

- Bloomberg reported a US crude inventory build of 2.48mn barrels last week, according to people familiar with the API data. There were also product builds with gasoline up 3.1mn and distillate 2.88mn. The official EIA data is out Wednesday.

- Later US November ADP employment, delayed September trade prices/IP and November services ISM/PMI print. European November services/composite PMIs and euro area October PPI are out. ECB President Lagarde speaks before the European parliament and ECB’s Lane and BoE’s Mann also make appearances.

PRECIOUS METALS: Dovish Fed Outlook Driving Prices Up, Silver Reaches Record

Silver has reached another record high during Wednesday’s APAC trading continuing to be driven by expectations of a Fed December rate cut, a dovish new Fed Chair in 2026 and a tight physical market. The rally has encouraged speculators into the market and it is now flashing overbought. The metal is up 0.6% to $58.84/oz after reaching $58.947, above resistance at $59.563. Attention is focused on resistance at $60.00.

- Gold is also higher today rising 0.4% to $4221.1 off the intraday peak of $4228.85.

- Bloomberg is reporting a 200t inflow into silver ETFs on Tuesday to their highest since 2022.

- There is growing conjecture that President Trump will choose his National Economic Council Director Bessent as the next Fed Chair, as he is expected to be more dovish. This is adding support to non-yield bearing assets, such as precious metals.

- The US dollar is softer (BBDXY -0.1%) and yields slightly lower. Equities are mixed with the S&P e-mini up 0.2% and Nikkei +1.5% but Hang Seng down 1.0% and CSI flat. Oil prices are little changed with WTI at $58.66/bbl. Copper is 0.7% higher.

- Later US November ADP employment, delayed September trade prices/IP and November services ISM/PMI print. European November services/composite PMIs and euro area October PPI are out. The ECB President Lagarde speaks before the European parliament and ECB’s Lane and BoE’s Mann also make appearances.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 03/12/2025 | 0700/0200 | * | Turkey CPI | |

| 03/12/2025 | 0730/0830 | *** | CPI | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 03/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 03/12/2025 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 03/12/2025 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/12/2025 | 1000/1100 | ** | EZ PPI | |

| 03/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/12/2025 | 1030/1130 | ECB Lane Keynote at Banca d'Italia Workshop on Exchange Rates | ||

| 03/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 03/12/2025 | 1315/0815 | *** | ADP Employment Report | |

| 03/12/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 03/12/2025 | 1330/1430 | ECB Lagarde Statement at ECON Hearing | ||

| 03/12/2025 | 1415/0915 | *** | Industrial Production | |

| 03/12/2025 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 03/12/2025 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 03/12/2025 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 03/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 03/12/2025 | 1530/1630 | ECB Lagarde Statement at ECON Hearing (as ESRB Chair) | ||

| 03/12/2025 | 1700/1700 | BOE Mann in Panel on Reserve Currencies | ||

| 04/12/2025 | 0030/1130 | ** | Trade Balance | |

| 04/12/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 04/12/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 04/12/2025 | 0800/0900 | ** | Unemployment | |

| 04/12/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/12/2025 | 0930/0930 | BOE Decision Maker Panel Data | ||

| 04/12/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/12/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 04/12/2025 | 1245/1245 | BOE Mann Panel at European and Global Issues Conference |