OIL: Crude Little Changed As Waits For US EIA Data Out Later

Oil prices are little changed today ahead of the US EIA fuel inventory and demand data later. The industry figures showed crude and product builds. The market is also monitoring US-Ukraine-Russia developments closely in case a peace deal is close which could see an easing of restrictions on Russia at a time of excess global oil supply. It doesn’t seem worried at this stage regarding Russia’s threat to strike vessels of countries supporting Ukraine.

- WTI is off its intraday low of $58.37/bbl to be steady at $58.66/bbl, while Brent is slightly higher at $62.49 after falling to $62.18.

- US Secretary of State Rubio said that talks are currently at the point of trying to work out what Ukraine can accept and to bridge the divide between it and Russia. Russia said that President Putin agreed with many points in the revised plan and the territory issue was discussed. The US is now going back to the Ukrainians.

- Venezuela, the world’s 17th largest oil exporter in 2023 (IEA), remains an issue with the US saying it will continue targeting drug running vessels and Rubio saying that negotiating a deal would be difficult as Venezuela’s Maduro has “broken every deal he’s ever made”.

- Bloomberg reported a US crude inventory build of 2.48mn barrels last week, according to people familiar with the API data. There were also product builds with gasoline up 3.1mn and distillate 2.88mn. The official EIA data is out Wednesday.

- Later US November ADP employment, delayed September trade prices/IP and November services ISM/PMI print. European November services/composite PMIs and euro area October PPI are out. ECB President Lagarde speaks before the European parliament and ECB’s Lane and BoE’s Mann also make appearances.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: KOSP Hits New Highs on Tech Rush

News that Nvidia has signed deals with Korean semi conductor companies like Samsung continue to underpin the rally in the KOSPI that is reaching new levels daily, and looking overbought on many valuation metrics. The rally now is the strongest in more than 20 years as Asia and particularly Korea position themselves in the global tech race. In China, gold related stocks were hit after a tax rebate on gold was ended by the government and could potentially increase costs. With Japan out, it was down to China to lead and despite the KOSPI's rally, China stocks were mixed on the day.

- The Hang Seng and CSI 300 were again going in opposite direction with the HSI up +0.58% and the CSI 300 down -0.45% whilst the Shanghai Comp was close to flat, whilst Shenzhen fell -0.61%

- The KOSPI hit 4,202 to be up +2.25% today to continue its run, now up over 70% YTD.

- The FTSE Malay KLCI has had a quiet period but is up today by +0.58% whilst the JCI in Indonesia is having its best start to a trading week in a fortnight with gains of +1.10%

- The NIFTY 50 posted new highs last week, before fading back and has started the week slowly flat at 25,727.

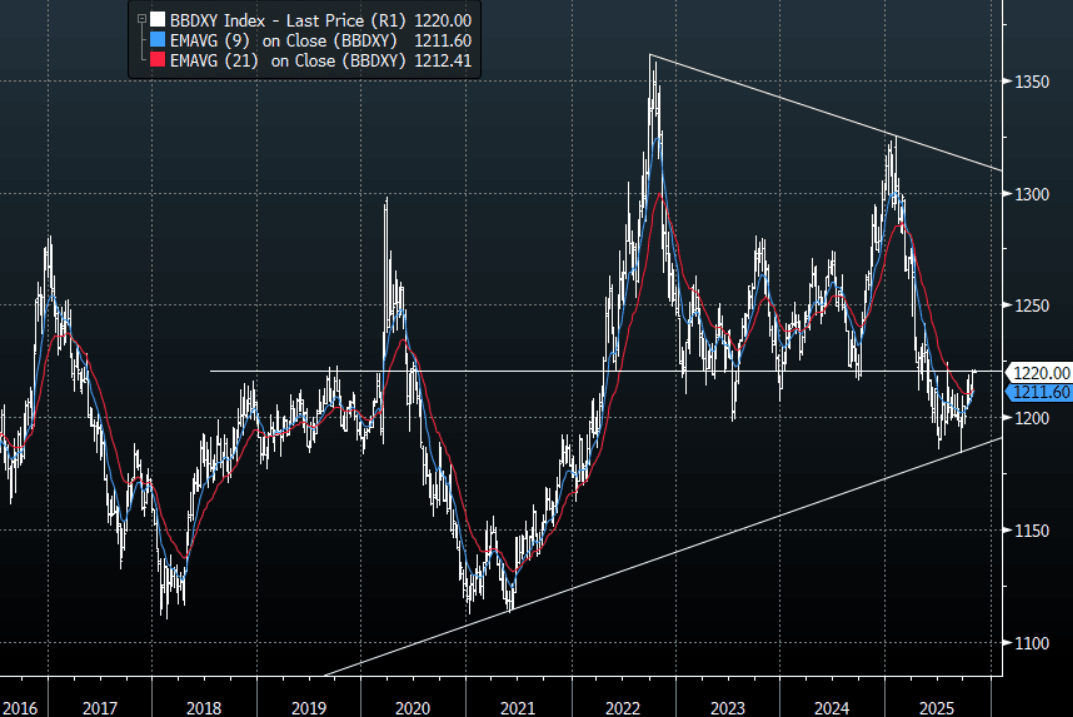

FOREX: Asia-Pac FX - BBDXY Moves Into Pivotal Resistance

The BBDXY has had a range of 1220.25 - 1221.11 in the Asia-Pac session; it is currently trading around 1220, -0.05%. The USD built on its gains from last week into the month-end. The 1220-30 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made on the Daily chart through October. A sustained move back above 1230 would potentially signal a medium term low is in place and a deeper pullback is on the cards.

- EUR/USD - Asian range 1.1522 - 1.1538, Asia is currently trading 1.1530. The pair has moved back toward its support just above 1.1500. A break under this support could signal a deeper correction, first target 1.1400 and then the 1.1100/1.1200 area.

- GBP/USD - Asian range 1.3130 - 1.3142, Asia is currently dealing around 1.3140. The pair looks to be building some downward momentum. This 1.3100/1.3150 area has proved to be supportive on more than 1 occasion this year so some work around this level could be expected. I continue to favor fading rallies though as GBP attempts to put in a medium term top.

- USD/CNH - Asian range 7.1178 - 7.1249, the USD/CNY fix printed at 7.0867, Asia is currently dealing around 7.1190. The support below 7.1000 looks to be pretty solid for now as USD/Asia moves in sympathy with a higher USD/JPY. The range of 7.08-7.16 looks set to continue for now.

- Cross asset : SPX +0.15%, Gold $4007, US 10-Year 4.0775%, BBDXY 1220, Crude Oil $61.18

- Data/Events : Italy HCOB Italy Manufacturing PMI/Budget Balance, Germany HCOB Germany Manufacturing PMI, EZ HCOB Eurozone Manufacturing PMI, France HCOB France Manufacturing PMI, Spain HCOB Spain Manufacturing PMI

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

RBA: MNI RBA Preview-November 2025: CPI Outlook Key To Rates

- Download Full Report Here

- The Q3 trimmed mean print at 3.0% y/y up from 2.7% and at the top of the 2-3% target band was a “material miss” for the RBA and meant that the Board is now highly likely to leave rates at 3.6% at its 4 November decision.

- The Board is likely to remain highly data dependent and cautious given inflation’s renewed shift higher and the emerging domestic recovery but easing labour market conditions.

- Updated staff forecasts will be released and the underlying inflation path is likely to be the focus to see how far out the return to the 2.5% band mid-point has been pushed out.

- The Board will need to see inflation resuming its trend lower towards 2.5% before it is likely to consider cutting rates again. Thus, rates are probably on hold in December and the Q4 CPI data on 28 January will be a key input into the 3 February decision.