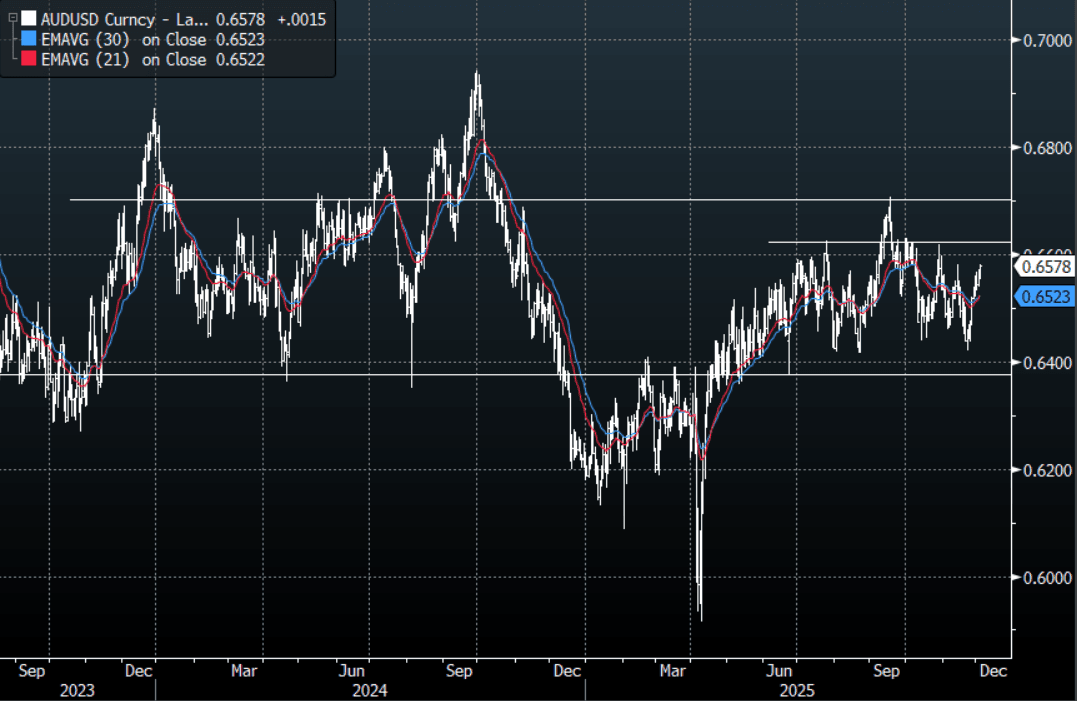

AUD: AUD/USD - GDP Data Not So Bad Sees AUD Bounce Back, Testing 0.6580

The AUD/USD has had a range today of 0.6553 - 0.6578 in the Asia- Pac session, it is currently trading around 0.6575, +0.20%. The AUD/USD had a brief look lower on the immediate GDP print back quickly recovered once the details showed underlying strength. The AUD has not backed off in all the noise and is pressing the pivot around 0.6580 within its wider 0.6350-0.6700 range. On the day, it feels like there is an air of inevitability around the AUD pushing above 0.6580 so I suspect dips back toward the 0.6535-0.6555 area could now be supported. A clear break above 0.6580 and the AUD could build some momentum looking to once again test the top end of its recent range, first target 0.6630 and then 0.6700.

- MNI AU - Strong Domestic Demand Growth To Keep RBA Cautious. Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details are a lot stronger than the headline with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

- MNI AU - RBA-dated OIS pricing is 1-7bps firmer for meetings beyond May today. Currently, pricing shows zero probability of a 25bp rate cut in December. More notable, the market has shifted to assign a 96% probability of a 25bp hike by December 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6475(AUD814m Dec 8), 0.6490(AUD710m Dec 4), 0.6500(AUD1.11b Dec 5) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 37 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

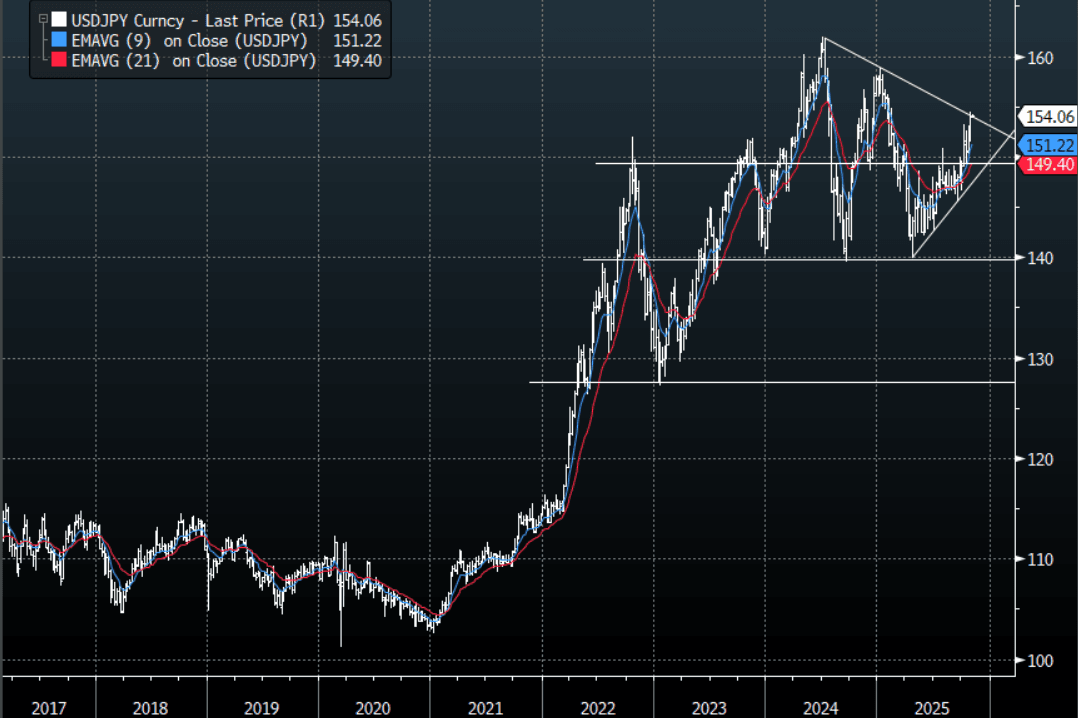

JPY: Asia-Pac - USD/JPY Consolidates Around 154.00

The USD/JPY range has been 154.00 - 154.25 in the Asia-Pac session, it is currently trading around 154.10, -0.05%. The pair remains well supported thanks to a combination of a hawkish FED and a BOJ that is still unsure about when it will raise rates. We are approaching some resistance back toward the 154/155 area and I would expect we might to do some work around here initially. I also suspect any sustained break back above 155 could see the move begin to accelerate and with that the potential for further intervention, though personally I think they will wait for levels closer to 160 to get involved. Look for dips to continue to be supported while above 149-150.

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.50($1.42b). Upcoming Close Strikes : 150.00($1.13b Nov 3) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia-Pac - AUD/USD Consolidates Around 0.6550 In A Quiet Session

The AUD/USD has had a range of 0.6539 - 0.6551 in the Asia- Pac session, it is currently trading around 0.6545, +0.03%. US yields retraced on Friday night but the USD continues to grind higher challenging levels last seen in July/August. The AUD/USD is back within its recent 0.6400-0.6650 range with the pivot being around 0.6500-0.6550 where I would expect some demand first up, RBA tomorrow but the market is not expecting them to move.

- Ex Alcohol & Tobacco, Q3 Consumer Spending Robust: September household spending was softer than expected rising 0.2% m/m to be up 5.1% y/y after a downwardly-revised 4.9% y/y. Q3 consumption volumes rose 0.2% q/q, the lowest rate since Q3 2024 but the fifth consecutive quarterly rise. Growth continued to recover rising 2.7% y/y, the highest since Q1 2024 but pressured by contracting alcohol & tobacco expenditure. The data point to a continued gradual recovery in private consumption. While the RBA is widely expected to be on hold this week, its consumption forecasts will be monitored for upward revisions.

- Bloomberg is reporting that “Pimco is betting on a rebound in Australian government bonds on expectations the RBA will resume easing next year, favoring the five- to 10-year part of the yield curve.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD 338m). Upcoming Close Strikes : 0.6625(AUD944m Nov 4), 0.6300(AUD600m Nov 4) - BBG

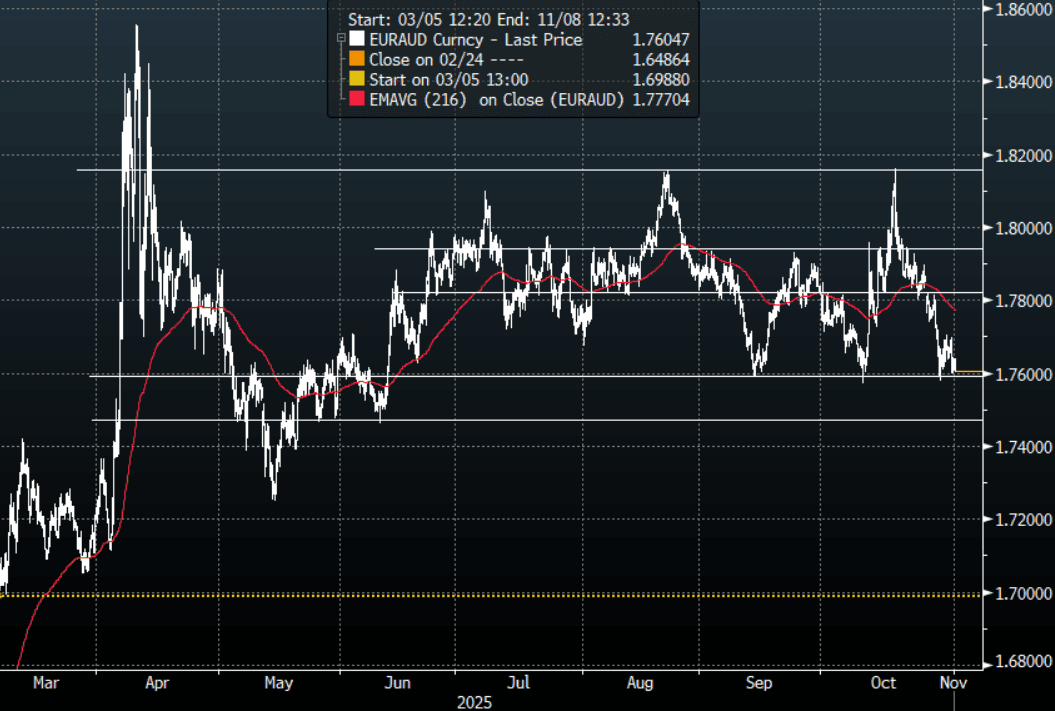

- EUR/AUD - Asia-Pac range 1.7602 - 1.7638, Asia is currently trading around 1.7605. The pair topped out again around 1.7700 and is once again testing the support in the 1.75-1.76 area. I suspect rallies toward 1.7700/1.7800 would now be faded but a break under the 1.7500 area is needed to signal a potential deeper pullback toward the 1.7000 area.

Fig 1: EUR/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

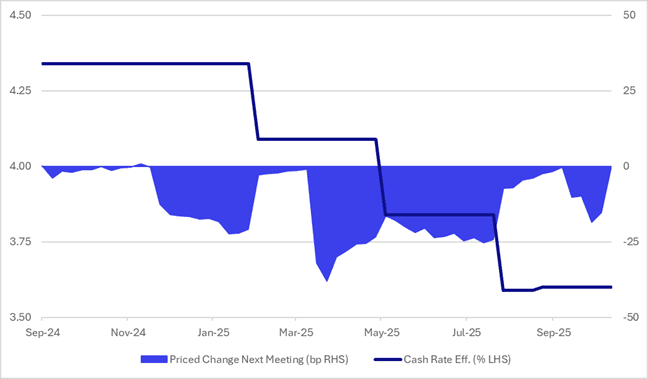

STIR: Market Gives A RBA Cut Tomorrow No Chance

Going into tomorrow’s RBA policy decision, RBA-dated OIS pricing implies almost no chance of an easing, with just a 2% probability assigned.

- In the wake of the surprise rise in the September unemployment rate to 4.5% in mid-October, markets had briefly priced as much as an 80% probability of a 25bp rate cut in November.

- However, that confidence faded in the lead-up to last week’s Q3 CPI release.

- Compared with previous episodes in this easing cycle, markets appeared noticeably less certain about a November 4 cut ahead of the CPI release.

- That caution proved justified, with the Q3 CPI printing well above expectations.

- As it currently stands, the OIS market has only an 80% chance of a 25bp cut by mid-2026.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI