BONDS: NZGBS: Partial Unwind Of Post-RBNZ Sell-Off

NZGBs closed showing a bull-flattener, with benchmark yields 4-7bps lower. Nevertheless, yields remain 12-25bps higher than last week’s pre-RBNZ levels.

- On a relative basis versus its $-bloc counterparts, NZGBs also had a good day, with the NZ-US and NZ-AU 10-year yield differentials 6bps and 10bps lower, respectively.

- NZ commodity export prices fell 1.6% m/m in November versus -0.3% in October.

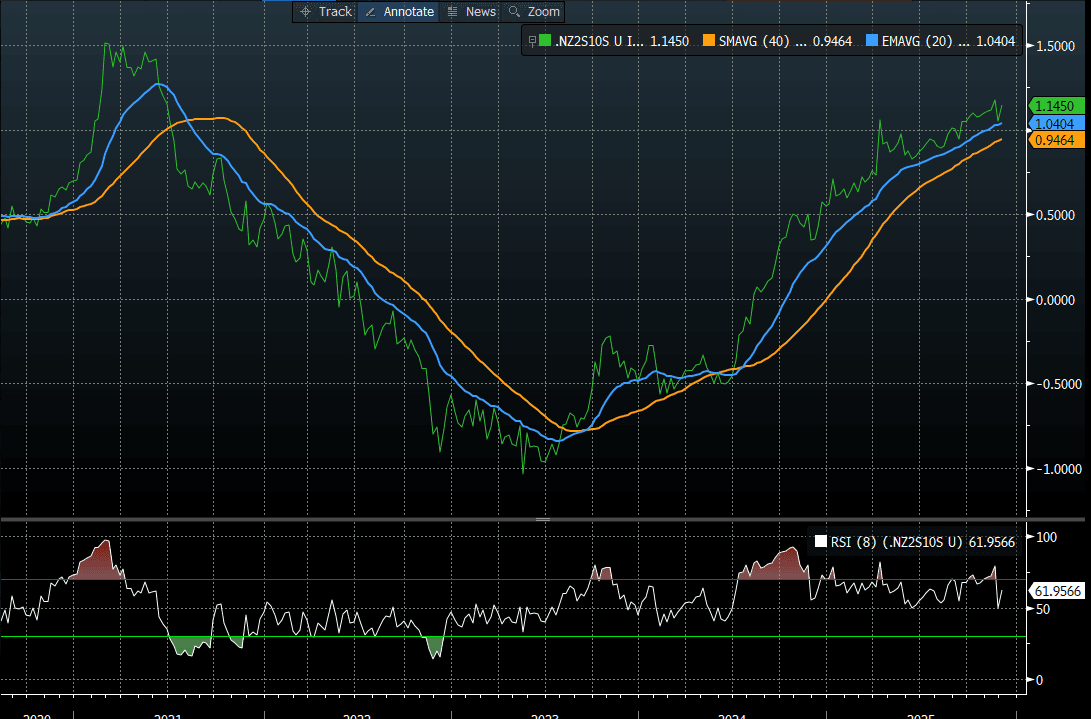

- Swap rates closed 2-7bps lower, with the 2s10s curve flatter. Nonetheless, the curve remains within striking distance of the 2021 peak (see chart).

- RBNZ-dated OIS pricing closed slightly softer across meetings. 2bps of easing is priced for February, while November 2026 assigns 31bps of tightening.

- Tomorrow, the local calendar will see Cotality Home Values and Volume of All Buildings data alongside NZ Government 4-Month Financial Statements.

- The NZ Treasury also plans to sell NZ$150mn of the 4.50% May-30 bond, NZ$225mn of the 4.50% May-35 bond and NZ$75mn of the 2.75% May-51 bond.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Market Gives A RBA Cut Tomorrow No Chance

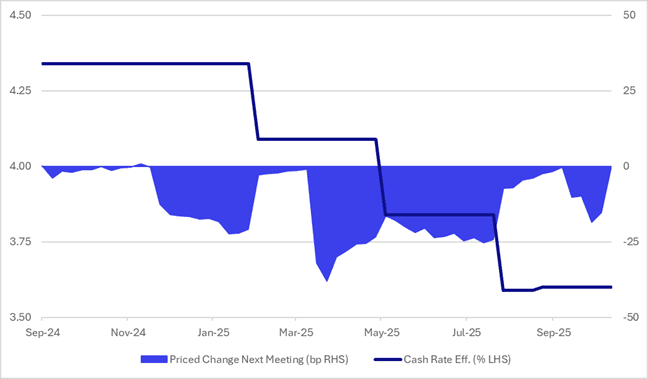

Going into tomorrow’s RBA policy decision, RBA-dated OIS pricing implies almost no chance of an easing, with just a 2% probability assigned.

- In the wake of the surprise rise in the September unemployment rate to 4.5% in mid-October, markets had briefly priced as much as an 80% probability of a 25bp rate cut in November.

- However, that confidence faded in the lead-up to last week’s Q3 CPI release.

- Compared with previous episodes in this easing cycle, markets appeared noticeably less certain about a November 4 cut ahead of the CPI release.

- That caution proved justified, with the Q3 CPI printing well above expectations.

- As it currently stands, the OIS market has only an 80% chance of a 25bp cut by mid-2026.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI

CHINA: Bond Futures Mixed on Liquidity Withdrawal

- In what looks like a decision to pause the bond rally, the liquidity withdrawal via the OMO sees bond futures mixed in morning trade.

- The 10-yr is flat at 108.67, maintaining its position above all major moving averages and near to oversold on a 14-day relative strength index.

- The 2-Yr is down -0.03 at 102.51 and remains above all major moving averages, having bounced from being oversold.

- The CGB 10-yr has ground lower in yield to be at 1.794%

CHINA PRESS: Changes To Gold VAT Could Increase China's Pricing Power

Changes to value-added tax (VAT) rules for gold trading on major exchanges could strengthen China’s international influence in gold pricing, according to Song Xiangqing, vice president at the China Business Economics Association. The Ministry of Finance recently announced that transactions without physical delivery will be exempt from VAT and for trades involving physical delivery, VAT treatment will vary based on the intended use of the gold, with non-investment use either being exempt from the tax or allowing buyers to apply a 6% input tax deduction rate. An expert noted the move could attract large institutional players to concentrate more trades on the major exchanges, thereby enhancing market liquidity and price-setting influence.