AUSSIE BONDS: Q3 Domestic Demand Drives Yields Higher, Hike Priced By Dec-26

ACGBs (YM -6.5 & XM -3.0) have bear-flattened after today’s Q3 GDP data. The market initially rallied on the data headlines but quickly reversed after details revealed underlying strength.

- Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details were a lot stronger than the headline, with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022.

- Cash US tsys are ~1bp richer in today’s Asia-Pac session.

- Cash ACGBs are 3-6bps cheaper with the AU-US 10-year yield differential at +56bps, the widest since mid-2022.

- The latest round of ACGB Dec-35 supply saw the weighted average yield print 0.30bp through prevailing mids. However, today’s cover ratio slumped to 2.3550x from 3.4875x.

- The bills strip has sharply steepened, with pricing -1 to -10.

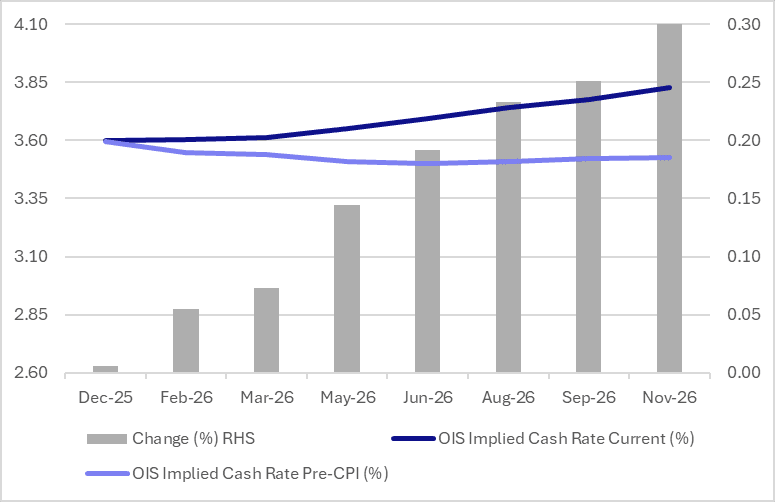

- RBA-dated OIS pricing is 1-7bps firmer for meetings beyond May today. Pricing shows zero probability of a 25bp rate cut in December. More notably, the market has shifted to assign a 96% probability of a 25bp hike by December 2026.

- Tomorrow, the local calendar will see Trade Balance and Household Spending data.

- The AOFM plans to sell A$1000mn of the 2.75% 21 November 2028 bond on Friday.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: Asia-Pac - USD/JPY Consolidates Around 154.00

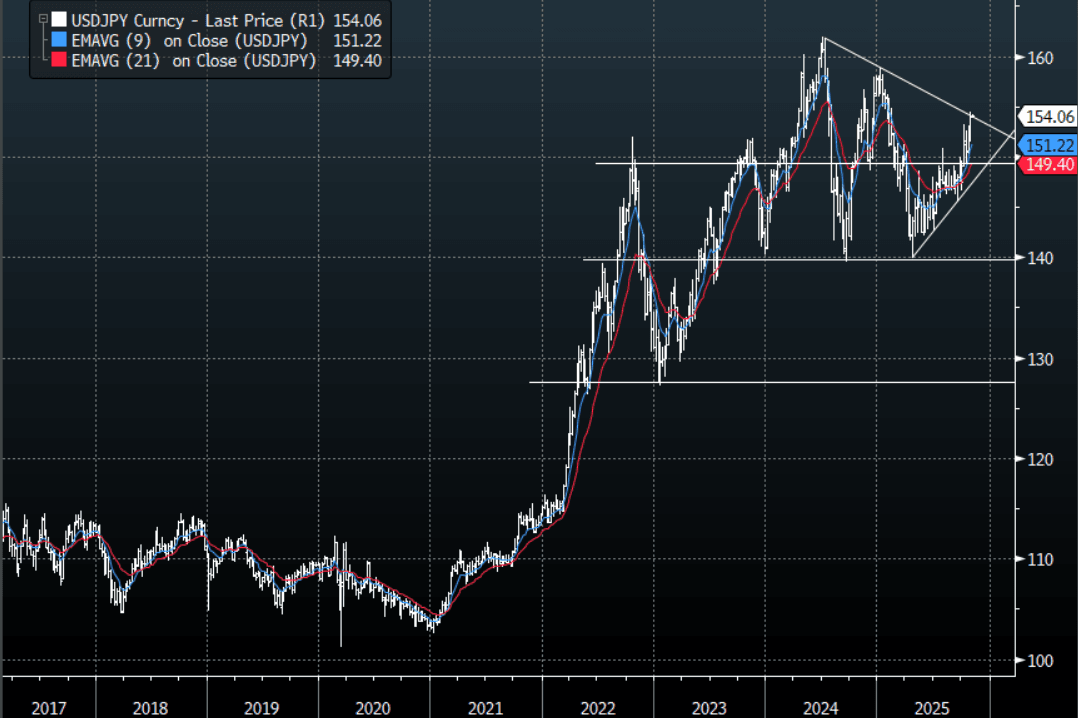

The USD/JPY range has been 154.00 - 154.25 in the Asia-Pac session, it is currently trading around 154.10, -0.05%. The pair remains well supported thanks to a combination of a hawkish FED and a BOJ that is still unsure about when it will raise rates. We are approaching some resistance back toward the 154/155 area and I would expect we might to do some work around here initially. I also suspect any sustained break back above 155 could see the move begin to accelerate and with that the potential for further intervention, though personally I think they will wait for levels closer to 160 to get involved. Look for dips to continue to be supported while above 149-150.

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.50($1.42b). Upcoming Close Strikes : 150.00($1.13b Nov 3) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia-Pac - AUD/USD Consolidates Around 0.6550 In A Quiet Session

The AUD/USD has had a range of 0.6539 - 0.6551 in the Asia- Pac session, it is currently trading around 0.6545, +0.03%. US yields retraced on Friday night but the USD continues to grind higher challenging levels last seen in July/August. The AUD/USD is back within its recent 0.6400-0.6650 range with the pivot being around 0.6500-0.6550 where I would expect some demand first up, RBA tomorrow but the market is not expecting them to move.

- Ex Alcohol & Tobacco, Q3 Consumer Spending Robust: September household spending was softer than expected rising 0.2% m/m to be up 5.1% y/y after a downwardly-revised 4.9% y/y. Q3 consumption volumes rose 0.2% q/q, the lowest rate since Q3 2024 but the fifth consecutive quarterly rise. Growth continued to recover rising 2.7% y/y, the highest since Q1 2024 but pressured by contracting alcohol & tobacco expenditure. The data point to a continued gradual recovery in private consumption. While the RBA is widely expected to be on hold this week, its consumption forecasts will be monitored for upward revisions.

- Bloomberg is reporting that “Pimco is betting on a rebound in Australian government bonds on expectations the RBA will resume easing next year, favoring the five- to 10-year part of the yield curve.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD 338m). Upcoming Close Strikes : 0.6625(AUD944m Nov 4), 0.6300(AUD600m Nov 4) - BBG

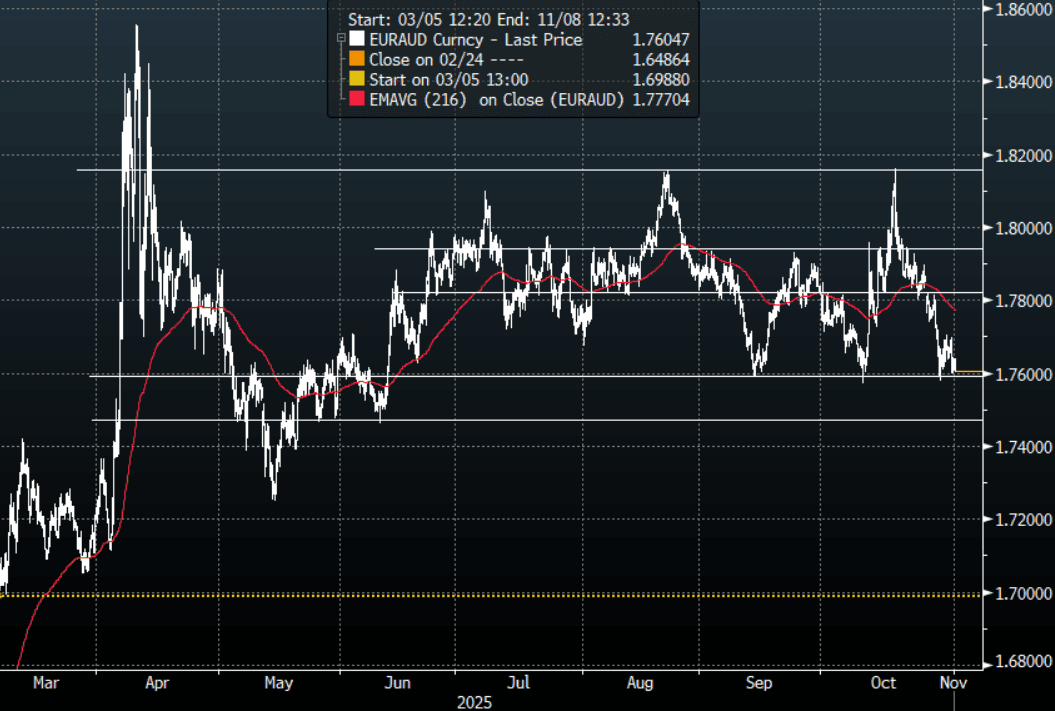

- EUR/AUD - Asia-Pac range 1.7602 - 1.7638, Asia is currently trading around 1.7605. The pair topped out again around 1.7700 and is once again testing the support in the 1.75-1.76 area. I suspect rallies toward 1.7700/1.7800 would now be faded but a break under the 1.7500 area is needed to signal a potential deeper pullback toward the 1.7000 area.

Fig 1: EUR/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

STIR: Market Gives A RBA Cut Tomorrow No Chance

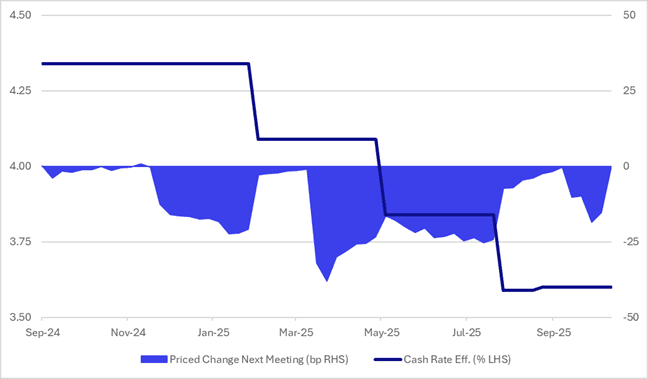

Going into tomorrow’s RBA policy decision, RBA-dated OIS pricing implies almost no chance of an easing, with just a 2% probability assigned.

- In the wake of the surprise rise in the September unemployment rate to 4.5% in mid-October, markets had briefly priced as much as an 80% probability of a 25bp rate cut in November.

- However, that confidence faded in the lead-up to last week’s Q3 CPI release.

- Compared with previous episodes in this easing cycle, markets appeared noticeably less certain about a November 4 cut ahead of the CPI release.

- That caution proved justified, with the Q3 CPI printing well above expectations.

- As it currently stands, the OIS market has only an 80% chance of a 25bp cut by mid-2026.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI