PRECIOUS METALS: Dovish Fed Outlook Driving Prices Up, Silver Reaches Record

Silver has reached another record high during Wednesday’s APAC trading continuing to be driven by expectations of a Fed December rate cut, a dovish new Fed Chair in 2026 and a tight physical market. The rally has encouraged speculators into the market and it is now flashing overbought. The metal is up 0.6% to $58.84/oz after reaching $58.947, above resistance at $59.563. Attention is focussed on resistance at $60.00.

- Gold is also higher today rising 0.4% to $4221.1 off the intraday peak of $4228.85.

- Bloomberg is reporting a 200t inflow into silver ETFs on Tuesday to their highest since 2022.

- There is growing conjecture that President Trump will choose his National Economic Council Director Bessent as the next Fed Chair, as he is expected to be more dovish. This is adding support to non-yield bearing assets, such as precious metals.

- The US dollar is softer (BBDXY -0.1%) and yields slightly lower. Equities are mixed with the S&P e-mini up 0.2% and Nikkei +1.5% but Hang Seng down 1.0% and CSI flat. Oil prices are little changed with WTI at $58.66/bbl. Copper is 0.7% higher.

- Later US November ADP employment, delayed September trade prices/IP and November services ISM/PMI print. European November services/composite PMIs and euro area October PPI are out. The ECB President Lagarde speaks before the European parliament and ECB’s Lane and BoE’s Mann also make appearances.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NZD: Asia-Pac - NZD/USD Finds Support Towards 0.5700

The NZD/USD had a range of 0.5713 - 0.5727 in the Asia-Pac session, going into the London open trading around 0.5725, +0.05%. US yields retraced on Friday night but the USD continues to grind higher challenging levels last seen in July/August. The NZD found some demand back toward 0.5700 and consolidated in a tight range over month-end. While price remains below the 0.5800/50 area I suspect rallies continue to be faded looking for a potential move back towards the 0.5500/0.5600 area. NZD continues to stand out as a short against a resurgent USD but it is worth noting that because of the size of the market the market can very quickly become all positioned the same way, so I think the USD will need to build on its challenge higher for the NZD to test those lows.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5650(NZD1.1b Nov 5), 0.5675(NZD1b Nov 5), 0.5750(NZD604m Nov 5) - BBG

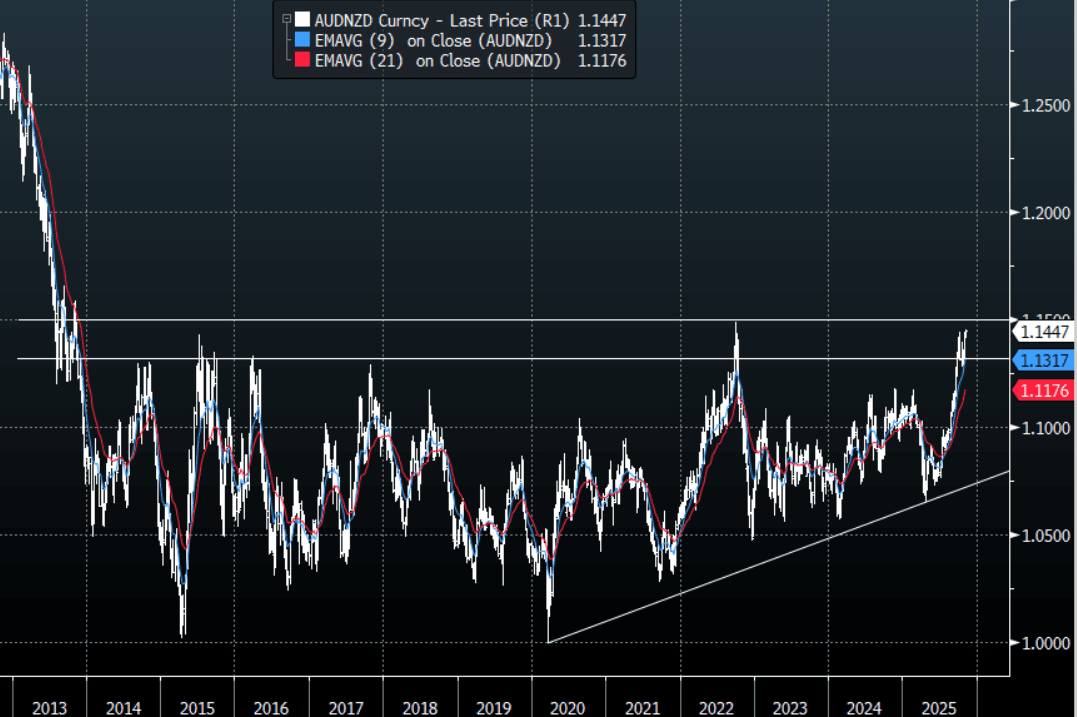

- AUD/NZD range for the session has been 1.1423 - 1.1453, currently trading around 1.1445. The Cross has bounced hard after finding solid demand back toward 1.1300. This 1.1400/1.1500 area remains tough resistance but the price action suggests the market wants to test it. Above 1.15/16 and the markets focus will start to turn toward 1.2000 and beyond.

Fig 1: AUD/NZD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

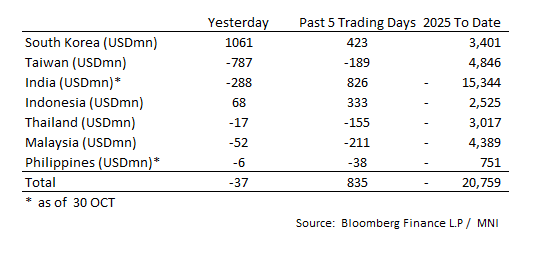

ASIA STOCKS: Korea Ends Month With Strong Inflows

- South Korea: Recorded inflows of +$1,061m Friday, bringing the 5-day total to +$423m. 2025 to date flows are +$3,401m. The 5-day average is +$85m, the 20-day average is +$225m and the 100-day average of +$137m.

- Taiwan: Had outflows of -$787m Friday, with total outflows of -$189 m over the past 5 days. YTD flows are positive at +$4,846m. The 5-day average is -$38m, the 20-day average of -$129m and the 100-day average of +$175m.

- India: Had outflows of -$288m as of the 30th, with total inflows of +$826m over the past 5 days. YTD flows are negative -$15,344m. The 5-day average is +$165m, the 20-day average of +$83m and the 100-day average of -$42m.

- Indonesia: Had inflows of +$68m Friday, with total inflows of +$333m over the prior five days. YTD flows are negative -$2,525m. The 5-day average is +$67m, the 20-day average +$45m and the 100-day average +$4m.

- Thailand: Recorded outflows of -$17m as of the 30th, with outflows totaling -$155m over the past 5 days. YTD flows are negative at -$3,017m. The 5-day average is -$31m, the 20-day average of -$9m and the 100-day average of -$9m.

- Malaysia: Recorded outflows of -$52m Friday, totaling -$211m over the past 5 days. YTD flows are negative at -$4,389m. The 5-day average is -$42m, the 20-day average of -$40m and the 100-day average of -$19m.

- Philippines: Recorded outflows of -$6m Friday, with net outflows of -$38m over the past 5 days. YTD flows are negative at -$751m. The 5-day average is -$8m, the 20-day average of -$3m the 100-day average of -$2m.

BONDS: NZGBS: Modest Bear-Steepener After A Subdued Session Of Trading

NZGBs closed showing a modest bear-steepener, with yields 1-3bps higher.

- The session was relatively subdued, with no cash US tsys trading due to the Japanese market being closed.

- The key event in NZ this week is the Q3 labour market and wages data released on Wednesday. Filled jobs for the quarter signal a stabilization, but employment is likely to have remained weak, with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ's August projections. Soft labour demand is likely to weigh on private wage growth, which is forecast to rise around 0.4% q/q after 0.6%.

- “The RBNZ said that the results of its 2025 bank stress tests showed that large banks are well placed to withstand and manage the impact of heightened geopolitical risks, according to a Monday statement.” - MTN

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for November, with a cumulative 30bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.