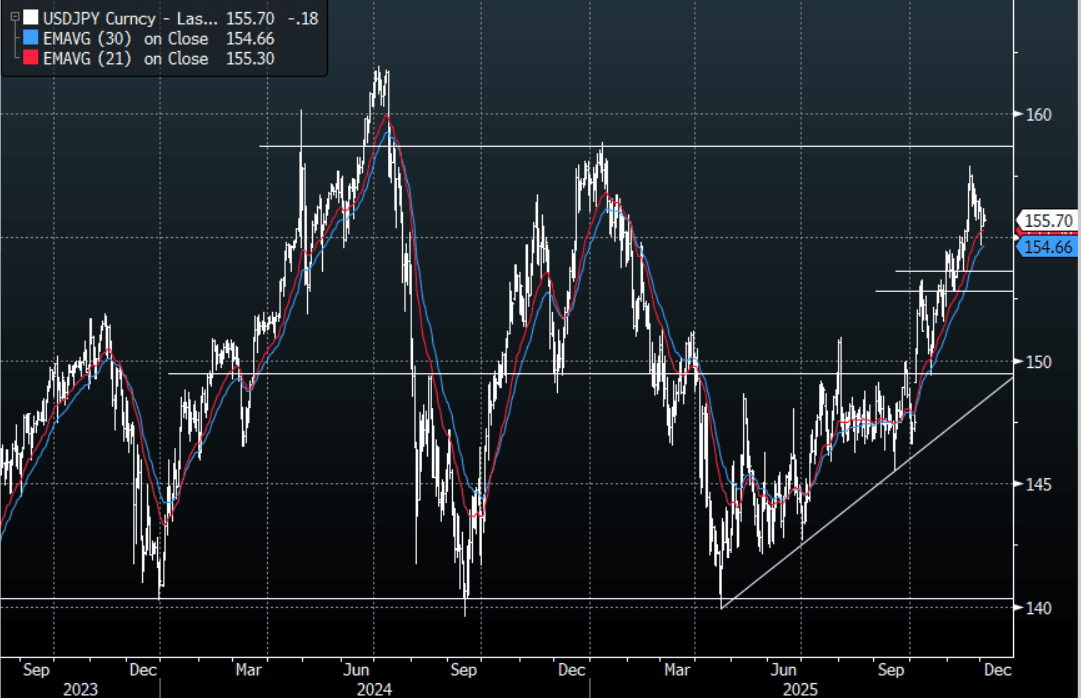

JPY: USD/JPY - Drifts Lower As The USD Trades Heavy

The USD/JPY range today has been 155.61 - 155.91 in the Asia-Pac session, it is currently trading around 155.70, -0.10%. The pair has drifted lower as the USD trades heavy across the board. The market is pricing in the fact that the Yen move looks like it could force the BOJ into action in December and a possible Hassett appointment brings more U.S. cuts into focus. This should keep the move that looked about to go parabolic a little more contained in the short-term but I suspect the market will still look for opportunities to express a long USD. Technically USD/JPY continues to look like it wants to test higher with the first big support back toward the 153-155 area which should see buyers reemerge. On the day I suspect we will continue to consolidate within a wider 155.00-156.50 range, with risk turning around its poor start to the week a short Yen might best be expressed in the crosses.

- (Dow Jones) - "Japanese government bond yields are higher as expectations for a near-term rate increase by the Bank of Japan continue. The BOJ's policy board is scheduled to meet on Dec. 18-19 for a final rate decision for the year. To gauge the economy's strength, investors will be focusing on economic indicators, including household spending data due Friday."

- MNI POLICY: Ueda Sharpens Dec Rate Hike, Risks Credibility. A hold at the Bank of Japan’s Dec. 18–19 meeting would be inconsistent with the bank’s recent market communications and would undermine its credibility, following Governor Kazuo Ueda’s comments on Monday that strongly indicated policymakers are set to raise the 0.5% rate this month, MNI understands.

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($1.27b). Upcoming Close Strikes : 153.00($1.2b Dec 4), 155.00($1.4b Dec 5), 156.00($1.14b Dec 8 ) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 88 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

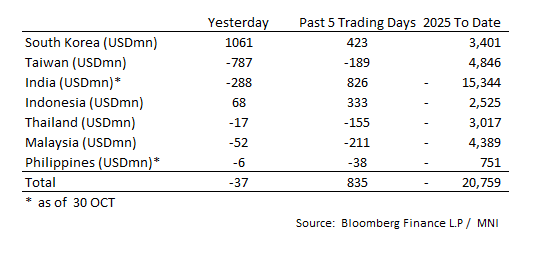

ASIA STOCKS: Korea Ends Month With Strong Inflows

- South Korea: Recorded inflows of +$1,061m Friday, bringing the 5-day total to +$423m. 2025 to date flows are +$3,401m. The 5-day average is +$85m, the 20-day average is +$225m and the 100-day average of +$137m.

- Taiwan: Had outflows of -$787m Friday, with total outflows of -$189 m over the past 5 days. YTD flows are positive at +$4,846m. The 5-day average is -$38m, the 20-day average of -$129m and the 100-day average of +$175m.

- India: Had outflows of -$288m as of the 30th, with total inflows of +$826m over the past 5 days. YTD flows are negative -$15,344m. The 5-day average is +$165m, the 20-day average of +$83m and the 100-day average of -$42m.

- Indonesia: Had inflows of +$68m Friday, with total inflows of +$333m over the prior five days. YTD flows are negative -$2,525m. The 5-day average is +$67m, the 20-day average +$45m and the 100-day average +$4m.

- Thailand: Recorded outflows of -$17m as of the 30th, with outflows totaling -$155m over the past 5 days. YTD flows are negative at -$3,017m. The 5-day average is -$31m, the 20-day average of -$9m and the 100-day average of -$9m.

- Malaysia: Recorded outflows of -$52m Friday, totaling -$211m over the past 5 days. YTD flows are negative at -$4,389m. The 5-day average is -$42m, the 20-day average of -$40m and the 100-day average of -$19m.

- Philippines: Recorded outflows of -$6m Friday, with net outflows of -$38m over the past 5 days. YTD flows are negative at -$751m. The 5-day average is -$8m, the 20-day average of -$3m the 100-day average of -$2m.

BONDS: NZGBS: Modest Bear-Steepener After A Subdued Session Of Trading

NZGBs closed showing a modest bear-steepener, with yields 1-3bps higher.

- The session was relatively subdued, with no cash US tsys trading due to the Japanese market being closed.

- The key event in NZ this week is the Q3 labour market and wages data released on Wednesday. Filled jobs for the quarter signal a stabilization, but employment is likely to have remained weak, with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ's August projections. Soft labour demand is likely to weigh on private wage growth, which is forecast to rise around 0.4% q/q after 0.6%.

- “The RBNZ said that the results of its 2025 bank stress tests showed that large banks are well placed to withstand and manage the impact of heightened geopolitical risks, according to a Monday statement.” - MTN

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for November, with a cumulative 30bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

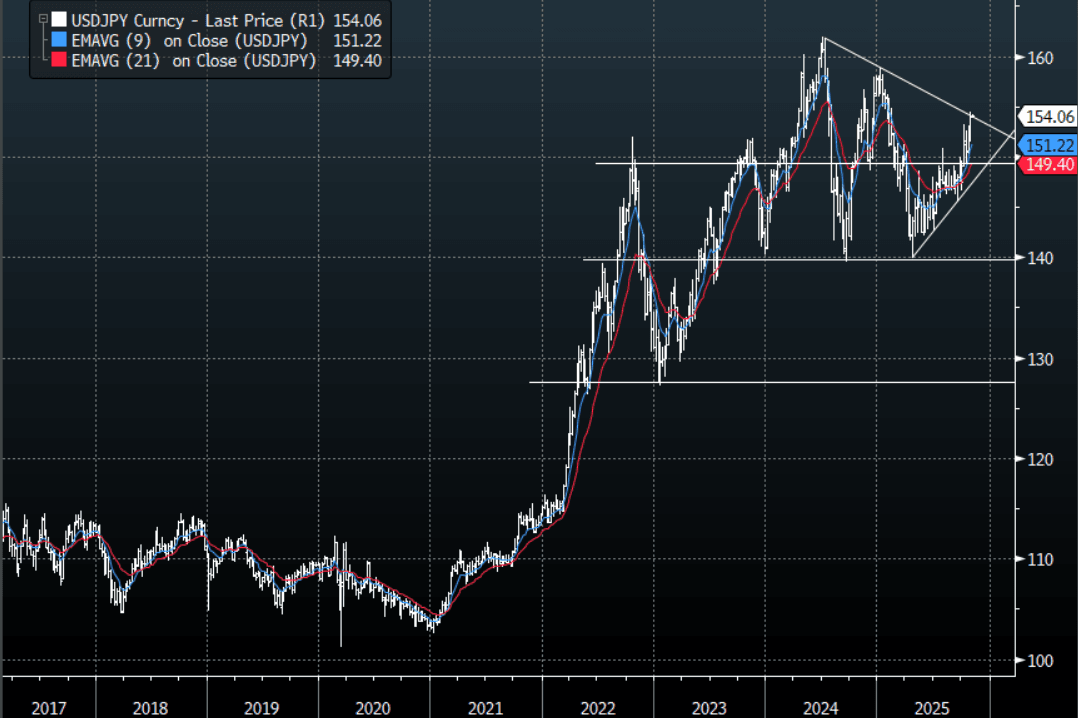

JPY: Asia-Pac - USD/JPY Consolidates Around 154.00

The USD/JPY range has been 154.00 - 154.25 in the Asia-Pac session, it is currently trading around 154.10, -0.05%. The pair remains well supported thanks to a combination of a hawkish FED and a BOJ that is still unsure about when it will raise rates. We are approaching some resistance back toward the 154/155 area and I would expect we might to do some work around here initially. I also suspect any sustained break back above 155 could see the move begin to accelerate and with that the potential for further intervention, though personally I think they will wait for levels closer to 160 to get involved. Look for dips to continue to be supported while above 149-150.

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.50($1.42b). Upcoming Close Strikes : 150.00($1.13b Nov 3) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P